If you have basis in an IRA, you will want to read this post. Basis in an IRA creates all sorts of confusion, but it also presents a great planning opportunity for many of those still working. I refer to this opportunity as the Basis Isolation Backdoor Roth IRA.

UPDATE March 10, 2026: I published an update to this post. Please read it (linked here) in conjunction with this post.

Where Does IRA Basis Come From?

Basis in a traditional IRA generally emerges from two sources. The first source is old nondeductible traditional IRA contributions that have not been Roth converted or withdrawn. Nondeductible traditional IRA contributions should be reported on a Form 8606 filed with one’s annual federal income tax return.

Many times this basis is simply exhausted annually by Backdoor Roth IRAs. Here’s a quick example:

Example 1: Becky contributed $6,500 to a traditional, nondeductible IRA on January 2, 2023. On February 1, 2023, when the traditional IRA was worth $6,504, she converted the entire traditional IRA balance to a Roth IRA. On December 31, 2023, she had $0 in all traditional IRAs, SEP IRAs, and SIMPLE IRAs. She successfully completed the Backdoor Roth IRA, which created $6,500 of IRA basis on January 2nd and exhausted all $6,500 of that basis on February 1st.

However, there are plenty of Americans who have existing and remaining IRA basis because they can’t do the Backdoor Roth IRA efficiently, or they never did the Backdoor Roth IRA.

To sum up, those doing annual tax-efficient Backdoor Roth IRAs tend not to have any IRA basis at year-end. But some Americans do have existing and remaining IRA basis.

The second source of IRA basis is from after-tax 401(k) contributions that have been transferred to a traditional IRA (see Natalie B. Choate’s treatise Life and Death Benefits for Retirement Planning (8th Ed. 2019), page 150).

There are Americans with existing IRA basis through transfers from a 401(k) (or other qualified plan) to a traditional IRA. However, going forward this should generally not occur. The IRS and Treasury issued Notice 2014-54, which provides that after-tax 401(k) contribution amounts can be rolled directly to a Roth IRA. From a planning perspective, after-tax 401(k) contributions (and other qualified plan after-tax contributions) should generally be directed into Roth IRAs if the plan participant prefers to exit the plan for IRAs (at retirement or a job change, for example).

Example 2: Chris is age 53. He leaves employment at Consolidated Industries, Inc. on November 1, 2023. At that time, he had a traditional 401(k) at Consolidated worth $500,000. During his time at Consolidated, Chris made $75,000 of after-tax contributions to the traditional 401(k) which remain in the traditional 401(k). Chris prefers to manage the money himself in an IRA or IRAs. Thus, he has two options:

Option One: Transfer the money (preferably through a direct trustee-to-trustee transfer) to a single traditional IRA. Chris now has $75,000 of traditional IRA basis.

Option Two: Transfer (preferably through direct trustee-to-trustee transfers) the after-tax money $75,000 to a Roth IRA and $425,000 to a traditional IRA. The $75,000 goes into the Roth IRA as a nontaxable conversion contribution (see also Notice 2014-54 Example 4). Chris receives no basis in his traditional IRA.

Which option is better for Chris? Clearly it is Option Two, which gives Chris tax-free growth on his $75,000. Further, Chris can withdraw the $75,000 from the Roth IRA tax and penalty free at any time while Chris would be subject to the hard bite of the Pro-Rata Rule if he used Option 1 and later withdrew $75,000 from the traditional IRA. Thus, while Chris is allowed to roll his $75K 401(k) basis into a traditional IRA, he would be much better served to roll the basis tax-free into a Roth IRA.

A Current Employer Qualified Plan That Accepts Rollovers

In order to have an IRA basis isolation opportunity, one must be currently employed by an employer with a qualified plan (often a 401(k)) that accepts IRA roll-ins. Many qualified plans accept IRA roll-ins but not all do.

Former employees generally are not able to contribute to 401(k)s and other qualified plans, so having a 401(k) plan at a former employer is generally not sufficient for this planning opportunity.

One should generally employ the Basis Isolation Backdoor Roth IRA if they have a 401(k) or other qualified plan at work they are satisfied with from both an investment choice standpoint and a fee standpoint. If one isn’t satisfied with their workplace retirement plan the Basis Isolation Backdoor Roth IRA may not be a good tactic to employ.

Comprehensive Basis Isolation Backdoor Roth IRA Case Study

Having addressed the two prerequisites to do a Basis Isolation Backdoor Roth IRA, let’s dive in with a comprehensive case study.

Imagine Ray has two (and only two) traditional IRAs. IRA 1 is a $100K traditional IRA rollover from an old 401(k). No basis came along in the rollover into IRA 1. IRA 2 is a traditional IRA worth $25K. It was established with three $6K nondeductible traditional IRA contributions for 2020 through 2022. He filed Forms 8606 reporting those contributions.

Ray’s current employer (Acme) has a great 401(k) that accepts roll-ins of traditional IRAs. What could Ray do to take advantage of his traditional IRA basis? He will need to isolate that basis, and that’s where the Basis Isolation Backdoor Roth IRA comes in.

Step 1

Ray transfers IRA 1 to the Acme 401(k), preferably through a direct trustee-to-trustee transfer.

Step 2

Ray invests about $18,010 of IRA 2 in a money market account and invests the remainder of IRA 2 in any investment of his choice (Mutual Fund A).*

By putting that $18,000 and a bit of change in a money market, Ray makes sure he “leaves behind” the IRA basis in the IRA! We will come back to why this “leave behind” asset is so critically important in the Step 3 discussion and analysis.

* As a practical matter, it may be easier to split IRA 2 into IRA 2 and IRA 3, with the $18,010 in IRA 2 and Mutual Fund A in IRA 3. Either path can work, but splitting into IRA 2 and IRA 3 may be the easier path. That split should be done internally at the IRA 2 institution without any check coming out of IRA 2 to the owner.

Step 3

Ray transfers the entire value of Mutual Fund A to the Acme 401(k), preferably through a direct trustee-to-trustee transfer.

The money market account is crucial. The Internal Revenue Code provides that IRA basis cannot be transferred to a 401(k) (see also Natalie B. Choate’s treatise Life and Death Benefits for Retirement Planning (8th Ed. 2019), page 158). By establishing that IRA 2 will have at least $18K that will not be moved into the 401(k), Ray ensures that he “leaves behind” at least his basis inside the IRA.

If the $18,010 was invested in an equity mutual fund (call it Mutual Fund B), there’s a risk that when Ray does Step 3 he will leave behind only Mutual Fund B, which could be less than his $18K basis if Mutual Fund B declines in value.

Example 3: Imagine Ray does Step 3 when Mutual Fund A is worth $10K and Mutual Fund B, originally worth $18K is now only worth $14K based on market declines. In such a case, $4K of basis would (theoretically) move into the Acme 401(k) with the $10K going from IRA 2 to the Acme 401(k). That would be a prohibited transfer of basis.

IRA Aggregation: Remember that for tax purposes, the IRS looks at all of Ray’s traditional IRAs (whether he has one or ten) as a single traditional IRA. We can’t say that basis attaches to IRA 2 only, so it is important that Ray leave at least $18K behind in an IRA so that after the transfers from his IRAs to qualified plans he can demonstrate that his basis was left behind in one or more of his traditional IRAs.

Step 4

Step 4: Ray converts the entire remaining balance in IRA 2 (likely to be $18,010 plus a bit of additional interest) to a Roth IRA. The only taxable amount is the small amount over $18,000.

Step 4 is reported on a Form 8606 (Parts 1 and 2).

Step 5

Ray ensures that as of December 31st of the year Step 4 occurs, Ray has $0 balances in all traditional IRAs, SEP IRAs, and SIMPLE IRAs.

The Benefits of the Basis Isolation Backdoor Roth IRA

Ray has moved approximately $107K from traditional IRAs to the Acme 401(k). That is entirely tax free and does not change the future tax treatment of that money. Perfectly fine, but by itself this doesn’t improve Ray’s tax position.

Before this planning, Ray had $18K of IRA basis that was of limited value due to the Pro-Rata Rule. Future taxable distributions or conversions from his traditional IRAs would have picked up only a small portion of that $18K, meaning that it would only protect small portions of future distributions and conversions from current taxation.

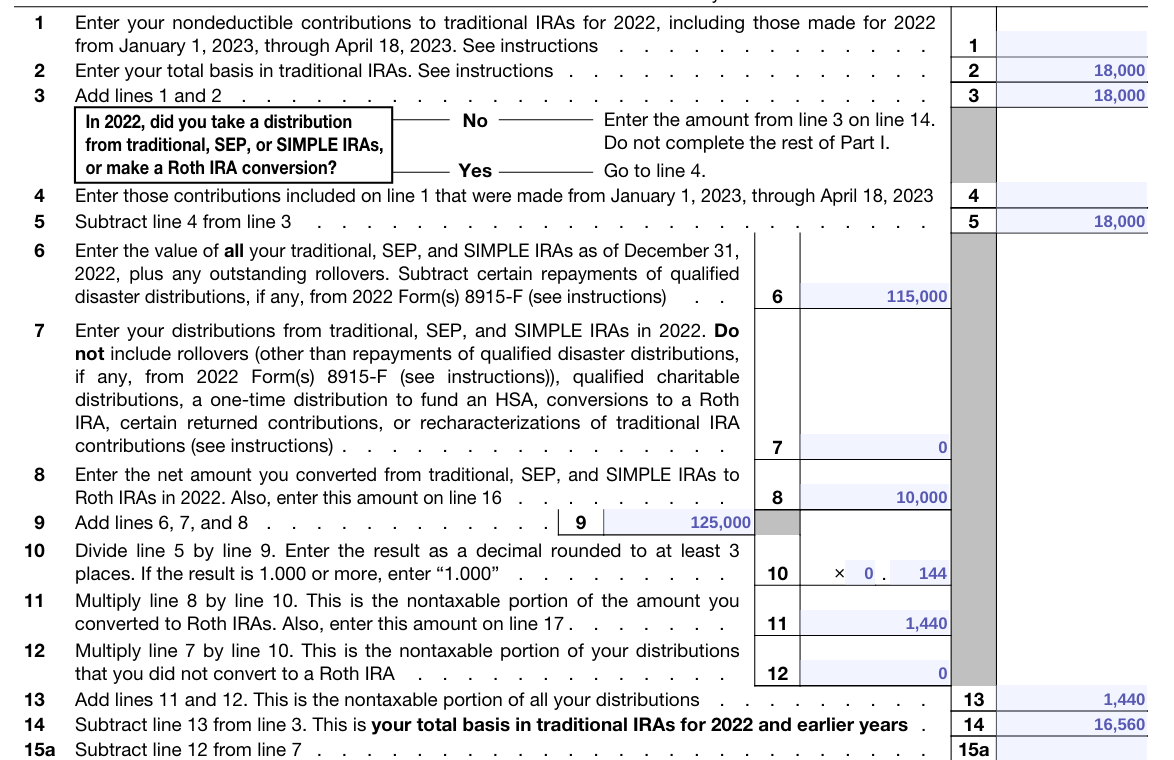

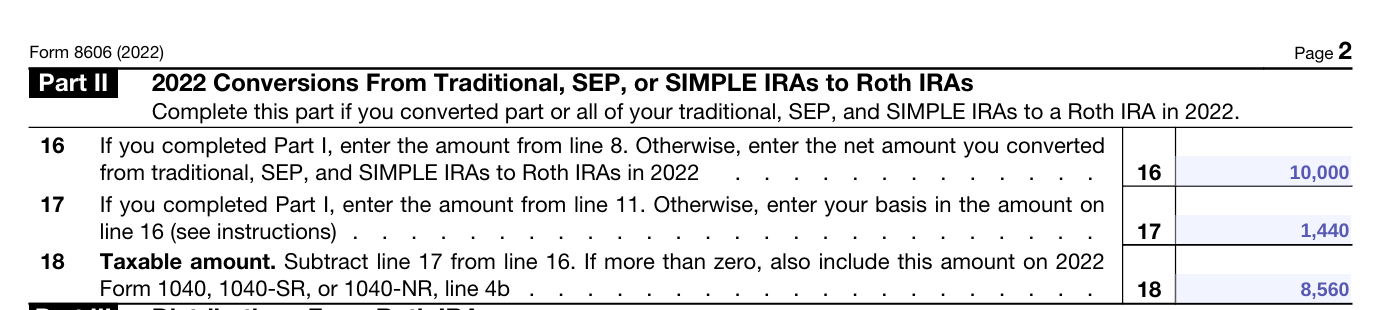

Example 4 The Pro-Rata Rule Bites Ray: If Ray had $18K of basis and $125K of total traditional IRAs and decided to do a $10K Roth conversion (without first doing the Basis Isolation Backdoor Roth IRA), approximately $1,440 of that Roth conversion would have been tax free and approximately $8,560 would have been taxable. See the mock Form 8606 Part I here and Form 8606 Part II here (though note that tax return software programs may use a separate statement instead of actually completing the form).

{kind=link}

{kind=link}

But with the Basis Isolation Backdoor Roth IRA Ray puts $18K plus into a Roth IRA and paid almost no tax to do so! Ray successfully isolated all $18,000 of basis to get it all into a Roth IRA without being adversely affected by the Pro-Rata Rule. Further, that $18,000 can now grow tax free for the rest of Ray’s life. Previously, inside a traditional IRA that $18,000 was growing tax-deferred, not tax free.

The Basis Isolation Backdoor Roth IRA improved Ray’s position by getting around the Pro-Rata Rule to get $18K plus into a Roth IRA for hardly any income tax. The only tax Ray pays is on the small amount the conversion amount in Step 4 exceeds $18,000.

The Basis Isolation Backdoor Roth IRA also opens another future tax planning opportunity. Going forward, Ray can do annual Backdoor Roth IRAs in a tax-efficient manner because he cleaned out his traditional IRAs into his workplace 401(k).

Practical Considerations

The Basis Isolation Backdoor Roth IRA is not a tactic to be affirmatively planned into. Rather, it is a clean up tactic. It makes the best of a situation where one has both basis and pretax amounts in traditional IRAs. The Backdoor Roth IRA is an affirmative planning technique, though it may require similar clean-up steps prior to implementation.

This planning is sophisticated and benefits from professional assistance. I recommend that most work with a professional if they are considering this sort of planning. Further, this planning does not occur every day. My experience suggests that most professionals are unfamiliar with this type of planning. Professionals will need to review resources such as this blog post and other sources and measure two or three times to dot I’s and cross T’s on this type of planning.

Of course, this blog post is not advice for the reader or any particular individual.

Additional IRA Basis and IRA Basis Isolation Resource

I went into detail on this planning in a June 2023 Measure Twice Planners presentation. While the presentation is mostly geared towards advisors, I hope I presented it in such a way that layman can also understand much of it and get value from it. The presentation and its slides, like this particular post, are for educational purposes only and are not intended as advice for any particular individual.

Conclusion

Existing basis in IRAs is a planning opportunity if the investor has a good workplace 401(k) or other qualified plan that accepts IRA roll-ins. That planning requires intention and diligence, and measuring two or three times, even if working with a professional.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

Follow me on X at @SeanMoneyandTax

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, legal, investment, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, legal, investment, and tax matters. Please also refer to the Disclaimer & Warning section found here.

Great solution, I wish I could take advantage of it. Any other solutions to clean this up? I have basis in an IRA, but it’s a tiny percentage of IRA total, so if I do Roth conversions, it’s going to become a paperwork nightmare over the years because of the pro-rata rule. Thanks again for your informative articles.