Basis in IRAs is a funny thing. It necessitates the Pro-Rata Rule, one of the least understood tax rules affecting financial planning. IRA basis creates all sorts of confusion, making traditional IRAs less user friendly.

Further, the value of basis in a traditional IRA is whittled away by inflation. Basis is generally the undistributed prior after-tax (or nondeductible) contributions in the IRA. Since basis might be distributed or converted years, perhaps decades, after the contribution, and is not increased for inflation, its value diminishes the longer it exists.

Thus, basis isolation techniques gain attention. The idea is to use the basis in an advantageous way to (1) harvest it prior to its value being eroded away by inflation and (2) move basis amounts into Roth IRAs relatively tax free.

Basis Isolation Techniques

The most basic basis isolation technique is a properly done Backdoor Roth IRA. IRA basis is created and quickly used to move money into Roth IRAs. The basis is fully used before inflation can erode its value.

The Backdoor Roth IRA is a simple tactic that, employed over many years, can be tremendously beneficial. It has very little downside risk and is relatively simple to implement.

Another basis isolation tactic is the qualified charitable distribution (“QCD”). This one is even easier than the Backdoor Roth IRA. QCDs do not take IRA basis when transferred to a charity. Thus, distributions the taxpayer receives and/or Roth conversions attract more of the available IRA basis to reduce the taxable amount. A small IRA basis benefit, but still helpful.

What about situations where someone has (1) significant basis in an IRA and (2) significant pretax amounts in an IRA? Now we have complexity, risk, and opportunity. The tactic I wrote about which could be useful in this situation is the Basis Isolation Backdoor Roth IRA.

The Basis Isolation Backdoor Roth IRA does the following:

- Cleans up IRA basis and uses it before inflation reduces its value.

- Creates a Roth IRA the owner can use for tax free withdrawals in retirement.

- Reduces future required minimum distributions (“RMDs”) by reducing the size of a traditional IRA.

I believe advisors and IRA owners need to proceed with caution when it comes to the Basis Isolation Backdoor Roth IRA. What initially looks incredibly attractive may turn out to be an unattractive planning technique.

Note that some 401(k) and other qualified plans do not accept roll-ins of IRAs. Some other plans only accept roll-ins of a certain type of IRA, a “conduit IRA.” A conduit IRA is an IRA comprised only of old 401(k)s, 403(b)s, governmental 457s, and other qualified plans and the growth thereon. Thus, plans requiring that the rolled-in IRA be a conduit IRA cannot be used to facilitate isolation of IRA basis created by old nondeductible traditional IRA annual contributions, since the growth on nondeductible traditional IRA contributions is not eligible to be moved over to such plans.

Basis Isolation Backdoor Roth IRA Examples

To analyze whether employing a sophisticated IRA basis isolation technique is advisable, I’m going to present two examples. These examples will illustrate when I favor and when I disfavor using the Basis Isolation Backdoor Roth IRA.

Example 1: Basis Isolation Backdoor Roth IRA into a Large Employer 401(k)

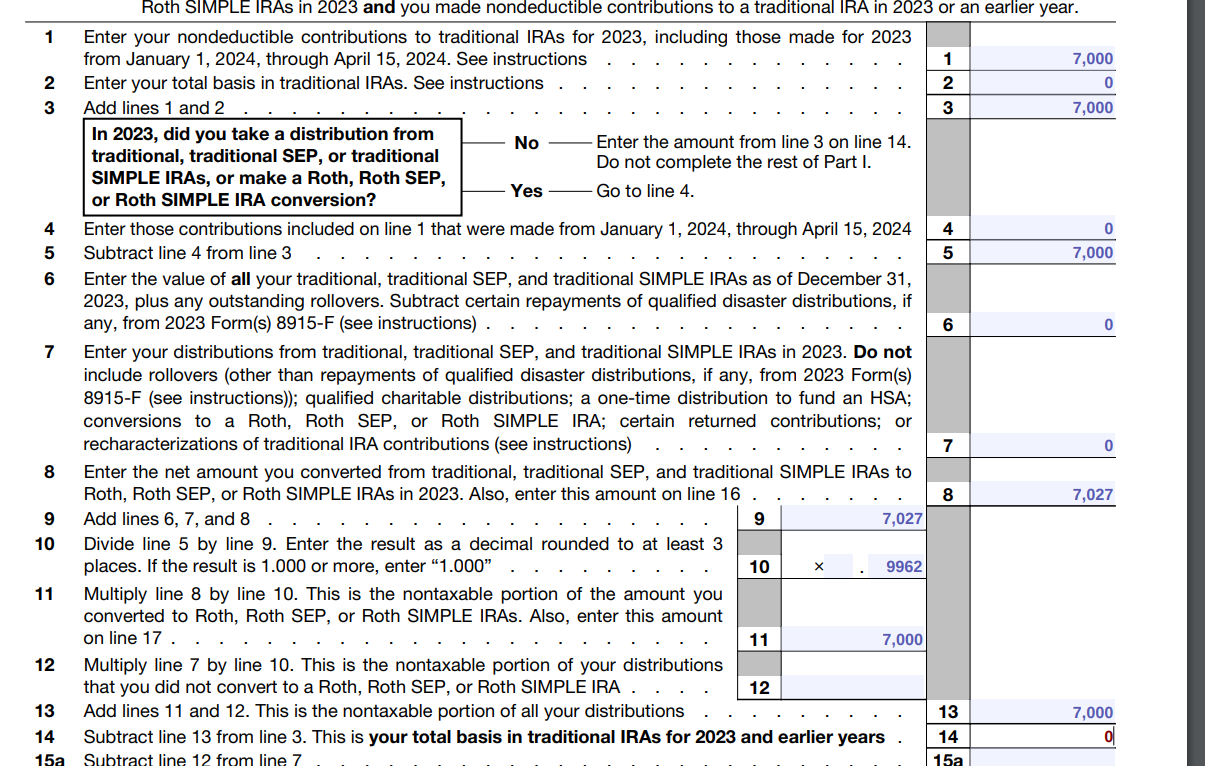

April, age 48 in 2026, works for Apple Inc. She is a participant in their 401(k) plan. In 2022 through 2026 her adjusted gross income was such that she qualified for neither a deductible annual contribution to a traditional IRA nor an annual contribution to a Roth IRA. In 2022 she contributed $6,000 to a traditional IRA. In 2023 she contributed $6,500 to a traditional IRA. In 2024 she contributed $7,000 to a traditional IRA.

All of these contributions were nondeductible. In 2025 April learned about the Backdoor Roth IRA and the Pro-Rata Rule. Thus, she did not make any contributions to a traditional IRA for 2025.

April is planning on retiring in five years. She has a sizable balance in her 401(k). Her taxable brokerage account is worth $100,000, and her traditional IRA is worth $100,000, consisting of (1) the three nondeductible contributions ($19,500 total), (2) a $20,000 401(k) rollover from a former employer plan and (3) investment growth on both 1 and 2. April has no Roth IRAs or health savings accounts.

Only for sake of this analysis, assume Apple’s 401(k) both accepts all IRA roll-ins (other than IRA basis) and offers satisfactory low-cost investment options.

April proceeds as follows:

Step 1: In May 2026, April contacts her IRA custodian and splits her $100,000 traditional IRA into two IRAs. The first is $19,700 invested in a money market account (her basis amount of $19,500 plus a small $200 round up). This IRA is the Leave Behind IRA. The second IRA (IRA 2) is worth $80,300 and can be invested in whatever April desires.

Step 2: April works with the Apple 401(k) plan and her IRA custodian to arrange a direct trustee-to-trustee transfer of IRA 2 from the traditional IRA to April’s Apple 401(k) account.

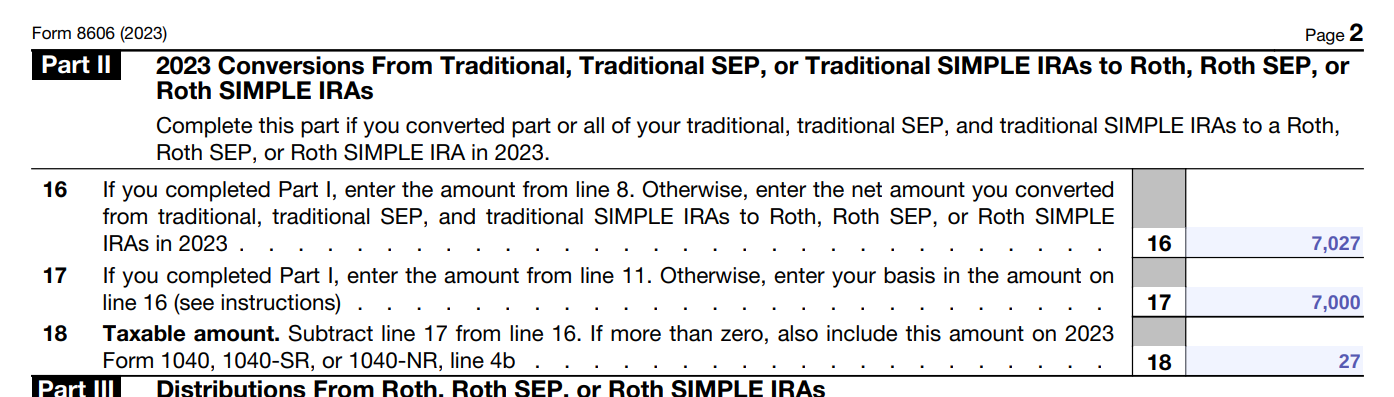

Step 3: After the completion of Step 2, April converts the entire Leave Behind IRA (now worth $19,900 due to interest accruing on the money market fund) to a Roth IRA. Due to IRA basis isolation, only $400 of the $19,900 is taxable to April on her 2026 federal income tax return.

Steps 1 through 3 are the Basis Isolation Backdoor Roth IRA.

Step 4: April executes the two steps of a 2026 Backdoor Roth IRA, getting another $7,500 (plus a small amount of interest) into her Roth IRA.

Step 5: April ensures that as of December 31, 2026, she has $0 balances in all traditional IRAs, traditional SEP IRAs, and traditional SIMPLE IRAs.

I’m drafting this at the end of the Winter Olympics. Recall that many of the figure skaters make the “heart sign” gesture after their skates. You can feel free to picture me making the heart sign gesture when thinking about April’s Basis Isolation Backdoor Roth IRA.

Why do I like this basis isolation play for April? Let me list the reasons.

Reason One: Helpful to April in early retirement. Recall that April intends to retire at age 53. Recall further that April has just $100,000 in a taxable brokerage account and no Roth IRA or HSA. Steps 1 through 4 create approximately $27,500 in Roth IRA basis that April can access in early retirement prior to age 59 ½ without tax or penalty. Further, the Basis Isolation Backdoor Roth IRA opens up the Backdoor Roth IRA for the last five years of her career, allowing her to create even more Roth IRA basis that can help fund early retirement advantageously from a Premium Tax Credit perspective and an income tax perspective.

Reason Two: Relatively modest IRA transfer. April moves approximately $80,000 of pretax IRA money. Any movement of pretax IRA money involves, however small, an element of risk. While $80,000 is not a tiny sum, it is also not a huge sum. It’s not the lion’s share of April’s wealth. Execution risk is mitigated in April’s case by the modesty of the sum moving into the Apple 401(k).

Reason Three: Using a large employer 401(k). Unless you work at Apple, you, like me, have little insight as to the contours and compliance record of Apple’s 401(k). Regardless, we would be absolutely shocked if we woke up tomorrow morning and read that the IRS and/or the Department of Labor challenged Apple’s 401(k) plan qualification.

Why? Disqualifying Apple’s 401(k) plan would create problems for thousands of voters. Congressmen from multiple Congressional districts, and perhaps even Senators, would strongly question the IRS and/or the Department of Labor about the issue. We know the motivations of the IRS and Department of Labor in this regard. They have every incentive to avoid significant headaches and work with Apple to get to a place where Apple’s 401(k) qualifies as a 401(k).

None of this is to cast aspersions at IRS and/or Department of Labor personnel. It’s simply acknowledging reality. How often do you look to stir up a hornet’s nest at your place of work?

As discussed above, I have absolutely no knowledge or opinion about the qualification of Apple’s 401(k) and/or the quality of the investments in it. I simply raise possibilities and discuss pivotal actors’ motivations to explore planning where one uses a workplace 401(k) to facilitate an IRA basis isolation transaction.

Helping fund early retirement. Relatively low risk of transferring pretax amounts. Parking assets in a stable, established, large employer 401(k) to achieve the objective.

April’s Basis Isolation Backdoor Roth IRA is quite attractive, in my opinion.

Example 2: Basis Isolation Backdoor Roth IRA into a Solo 401(k)

Jack, age 66 in 2026, and his wife, Becky, also age 66 in 2026, retired two years ago. Jack made $80,000 of nondeductible traditional IRA contributions over the years. With rollovers of prior large employer 401(k)s, today Jack’s traditional IRA is worth $2 million. Jack is very happy with the financial institution holding the traditional IRA and the investments offered by that institution.

Jack and Becky currently live off taxable brokerage accounts, currently worth $1 million. Becky also has $500,000 in a traditional IRA with no basis. Neither Jack nor Becky has a Roth IRA or an HSA.

Jack is interested in isolating his $80,000 traditional IRA basis and getting it into a Roth IRA. He’s heard about the Solo 401(k) and is intrigued. He concocts an idea. He will drive for Lyft part time for three months. Doing so brings in $3,000 of revenue. After expenses and a deduction for half of his self-employment taxes, he has $2,000 of net profit.

Jack proceeds as follows:

Step 1: Jack takes the position that he has self-employment income in 2026 and thus opens a Solo 401(k). He makes a maximum $2,000 employee deferral contribution for 2026.

Step 2: In August 2026, Jack contacts his IRA custodian and splits his $2 million traditional IRA into two IRAs. The first is $80,200 invested in a money market account (his basis amount of $80,000 plus a small $200 round up). This IRA is the Leave Behind IRA. The second IRA (IRA 2) is worth $1,920,000 and can be invested in whatever Jack desires.

Step 3: Jack works with the Solo 401(k) plan custodian and his IRA custodian to arrange a direct trustee-to-trustee transfer of IRA 2 from the traditional IRA to Jack’s Solo 401(k) account.

Step 4: After the completion of Step 3, Jack converts the entire Leave Behind IRA (now worth $80,500 due to interest accruing on the money market fund) to a Roth IRA. Due to IRA basis isolation, Jack takes the position that only $500 of the $80,500 is taxable to him on his 2026 federal income tax return.

Steps 2 through 4 are the Basis Isolation Backdoor Roth IRA.

Step 5: Jack ensures that as of December 31, 2026, he has $0 balances in all traditional IRAs, traditional SEP IRAs, and traditional SIMPLE IRAs.

Jack’s Basis Isolation Backdoor Roth IRA makes me feel the way my New York Jets fandom has in recent years. For those unaware, the Jets currently have the longest streak of missing the playoffs in North American major sports.

Why do I disfavor this basis isolation play for Jack? Let me list the reasons.

Reason One: No help solving retirement funding issues. Jack and Becky’s retirement is well funded. Unlike April, they do not need to control income for Premium Tax Credit purposes. Jack and Becky are currently living off taxable accounts. As I have previously discussed, they may pay practically no federal income tax doing so.

Why are Jack and Becky moving a large account and doing sophisticated distribution planning when they already have years of paying hardly any federal income tax?

Reason Two: Large IRA transfer. Jack moves approximately $1.92M of pretax IRA money. Any movement of pretax IRA money involves, however small, an element of risk. $1.92 million is the lion’s share of Jack and Becky’s financial wealth. Execution risk on a $1.92 million transfer of assets already in a satisfactory location, a traditional IRA with a liked institution, is not something I favor successful retirees affirmatively planning into.

Reason Three: Using a Solo 401(k). Compare the IRS disqualifying Jack’s Solo 401(k) with disqualifying Apple’s Solo 401(k). No Congressman is reaching out to the IRS if they disqualify Jack’s Solo 401(k). Further, the success of Jack’s strategy depends on him successfully maintaining his Solo 401(k) in the future. Rocket science? No. But guaranteed? Also, no.

Is Jack’s Solo 401(k) Valid?

Contributions of Self-Employment Income

I strongly question whether Jack would have a valid Solo 401(k) in this fact pattern. Consider the Congressional intent behind Solo 401(k)s. Solo 401(k)s allow the self-employed to make significant contributions of self-employment income to retirement accounts. Solo 401(k)s solve for the problem of the self-employed not having access to large employer 401(k) plans.

Jack’s use of a Solo 401(k) is hardly reflective of the intent behind the Solo 401(k). Jack accumulated years of retirement account contributions in a traditional IRA. He had no need for the Solo 401(k) to accumulate and maintain retirement savings. Further, about a tenth of a percent of the Solo 401(k) balance is funded by “self-employment income.” About 99.9 percent of the balance of Jack’s Solo 401(k) has nothing to do with self-employment.

These numbers indicate that Jack’s Solo 401(k) has little to do with contributions of self-employment income to save for retirement.

Is Jack Self-Employed?

As I discussed on page 24 of this article, one needs self-employment to have a Solo 401(k). I strongly question whether Jack’s Lyft driving qualifies as self-employment allowing him to open a Solo 401(k).

Consider making the case to respect Jack’s Lyft activities as “self-employment.” How is a retired person self-employed? What do Jack and Becky live off of? Accumulated retirement assets or Lyft income? That Jack and Becky live off their retirement savings and not off Jack’s Lyft income is instructive in determining whether that income comes from an activity sufficient to be considered a business to allow Jack to have a Solo 401(k).

IRA Basis Isolation and Solo 401(k) Stuffing

I’m not shy when I see the IRS in a weak position. In this article, I strongly argue the IRS has a very weak position if they attempt to enforce the literal terms of Notice 2022-6 governing 72(t) payment plans.

I’m also not shy in acknowledging situations where the IRS may have a strong position. When it comes to stuffing Solo 401(k)s for distribution motivated reasons, I believe the IRS has a strong position. I previously wrote about this when it comes to stuffing a Solo 401(k) for Rule of 55 planning. See pages 24 through 26 of this article.

I believe the IRS would have a high likelihood of success were they to challenge the validity of Jack’s Solo 401(k). Can you imagine taxing a $2 million traditional IRA through an attempted rollover into an invalid Solo 401(k) just to get $80,000 into a Roth IRA?

After considering Solo 401(k) stuffing in the contexts of both the Rule of 55 and the Basis Isolation Backdoor Roth IRA, I’ve come up with Mullaney’s Solo 401(k) Distribution Planning Principle:

Do not use a Solo 401(k) for distribution planning.

Solo 401(k)s can be distributed out of (as I argue in this article), but I disfavor using them to facilitate sophisticated distribution planning such as a Basis Isolation Backdoor Roth IRA.

Fortunately, Solo 401(k)s remain a great option for accumulation planning for the fully self-employed.

Tax Planning and New Businesses

I disfavor tax planning that necessitates the starting of a business to achieve retirement tax benefits.

Picture a financial planner, Jill, recommending to Jane, a self-employed lawyer, that she opens a Solo 401(k). Jill’s recommendation does not necessitate Jane starting a business. Jill simply is recommending a potentially advantageous tactic that Jane’s preexisting business opens the door to.

Contrast Jane’s preexisting business with Jack’s new “business” of Lyft driving. There are legitimate Lyft businesses operated by thousands of Americans. But in Jack’s case, his Lyft activity does not strike me as likely to be considered a trade or business sufficient to open a Solo 401(k).

Even if the Lyft activity is a sufficient trade or business, why do tax planning that requires changes in lived experience when the retiree is already financially successful?

Basis Isolation Backdoor Roth IRA Planning

Factors I view as favorable indicators that the Basis Isolation Backdoor Roth IRA may be a good planning tactic:

- Need for Roth basis in early retirement

- Relatively modest pretax amounts in traditional IRAs

- Possibility of opening up several years worth of Backdoor Roth IRAs

- Rolling pretax amounts into a large employer 401(k) with good investment selections

Factors I view as indicative that the Basis Isolation Backdoor Roth IRA should be disfavored:

- No compelling need for Roth basis in early retirement

- Significant pretax amounts in traditional IRAs

- No ability to do future Backdoor Roth IRAs

- Rolling pretax amounts into a Solo 401(k)

- The necessity to start a business to achieve a tax benefit in retirement

- Confusion surrounding the actual amount of IRA basis, since IRA basis cannot be rolled into a 401(k) or other workplace retirement plan

The above are my opinions. None of this should be read as advice for you or anyone else. Further, none of this should be read as to say any previously implemented planning in this regard is “wrong.” Rather, all this is intended to provide is my views as to what is desirable and what is not desirable from a planning perspective.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

Follow me on LinkedIn: @SeanWMullaney

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

{kind=link}

{kind=link}