Did you know that if you’re reading this before April 16, 2025 (before October 16, 2025 if you live in Los Angeles), it’s still possible to do a 2024 Backdoor Roth IRA?

Below I go through an example with a theoretical step plan to do two Backdoor Roth IRAs in 2025!

Everything below is academic information and opinion provided for your education and entertainment. It is not individualized tax, legal, or investment advice for you or anyone else.

2024 and 2025 Backdoor Roth IRA Example

Brad is 38. In early 2025, he learned about the Backdoor Roth IRA. He makes approximately $300,000 of adjusted gross income in each of 2024 and 2025, so he does not qualify for an annual Roth IRA contribution. Brad has no traditional IRAs, SEP IRAs, and/or SIMPLE IRAs.

Brad takes the following steps to implement two Backdoor Roth IRAs in 2025.

Step 1: Brad contributes $7,000 to a traditional IRA in February 2025. He codes the contribution as being for 2024. Brad invests it in a money market fund.

Step 2: In March 2025, Brad converted the entire traditional IRA balance, now $7,020, to a Roth IRA.

Step 3: In April 2025, Brad files his 2024 federal income tax return with a Form 8606 reporting the $7,000 2024 nondeductible traditional IRA contribution.

Step 7: Brad files a Form 8606 with his 2025 federal income tax return. It reports (1) the 2025 nondeductible traditional IRA contribution and (2) both Roth conversions.

It’s almost too easy 😉 . . .

Here is what Brad’s 2025 Form 8606 looks like (pardon the use of the 2024 version of the form, as I cannot currently access the 2025 version without a DeLeorean, a flux-capacitor, and 1.21 gigawatts of electricity).

What Has Brad Accomplished?

I believe this planning can be quite beneficial for Brad’s financial future. He just got $14,000 out of taxable accounts and into a tax free account for the rest of his life. Further, that $14,000 now enjoys a significant degree of creditor protection (note this does vary state to state).

Two years of a Backdoor Roth IRA don’t make that much of a difference. But what about 5 years? 10 years? 20 years? Now we are talking about significant numbers that can help Brad accomplish his financial goals.

Conclusion

In early 2025 it is not too late to do a Backdoor Roth IRA for 2024. I refer to this as the Split-Year Backdoor Roth IRA. It can be combined with a current year Backdoor Roth IRA.The taxpayer has to have the right profile, including no balances in traditional IRAs, SEP IRA, and/or SIMPLE IRAs.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

Late 2022 ushered in a new type of contribution to Solo 401(k)s: Roth employer contributions. Traditional employee and employer contributions have been available for all of the Solo 401(k)’s post-EGTRRA history. Roth employee contributions have been available since 2006, even if plan providers were slow to adopt them.

Should the availability of Roth employer contributions change planning for most solopreneurs? Not to my mind.

I have three concerns with making Roth employer contributions to Solo 401(k)s.

First Concern: Validity

Update March 13, 2026: Two federal judges agree with me. Two disagree with me. Thus, my view loses! The first concern discussed in this article, originally published in January 2025, is no longer a concern. I discussed a major development occurring after this article was originally published in this blog post.

Roth employer contributions were part of SECURE 2.0, which was part of the Omnibus bill passed in December 2022. That Omnibus bill has been subject to litigation. In Texas v. Garland (accessible here and here), Judge James W. Hendrix ruled for the State of Texas that the House of Representatives impermissibly used proxies to establish a quorum in order to pass the Omnibus, in violation of the Constitution’s Quorum Clause.

I encourage you to read the Texas v. Garland opinion. It is very convincing in my opinion.

While Texas v. Garland does not technically apply to SECURE 2.0, its reasoning does. Any taxpayer in the country facing harm under SECURE 2.0 (perhaps because they were denied the deduction for catch-up contributions under SECURE 2.0 Section 603) can pick it up and ask another federal judge to invalidate SECURE 2.0. That leaves SECURE 2.0 on shaky footing.

Short of litigation, there’s the question of what the new Administration will do with the Omnibus and SECURE 2.0. Texas v. Garland is litigation between the old Department of Justice and Ken Paxton, the Attorney General of Texas. Ken Paxton is much closer aligned politically with the Trump Administration. Will the Trump DoJ continue to litigate against Ken Paxton? The Trump Administration may simply refuse to uphold the Omnibus, including SECURE 2.0.

My hope is that if that happens taxpayers who have relied on SECURE 2.0 will be held harmless. For example, amounts in Roth 401(k)s (including Solo 401(k)s) attributable to employer contributions should be deemed to be amounts validly within the Roth 401(k) plan, so past reliance does not cause future harms (such as failed plan qualification). That said, my hope, a reasonable hope, is just a hope.

Regardless of one’s views on the Quorum Clause litigation, there’s at least some doubt as to SECURE 2.0’s validity, including the validity of Roth employer contributions to Solo 401(k)s. That makes planning into them difficult, in my opinion.

Second Concern: Section 199A Problem

Ben Henry-Moreland of Kitces.com wrote a thoughtful article on Roth employer contributions to Solo 401(k)s potentially reducing a solopreneur’s Section 199A qualified business income deduction.

I both agree and disagree with Mr. Henry-Moreland. I agree in a general sense that recent IRS guidance has muddied the waters when it comes to tax return reporting of Roth employer contributions to Solo 401(k)s. I disagree with his conclusion that this guidance results in non-deductible Roth employer contributions to Solo 401(k)s reducing the Section 199A qualified business income deduction.

The concern is Roth employer contributions might reduce the amount of qualified business income that then determines the Section 199A QBI deduction. Mr. Henry-Moreland is concerned about this because of Notice 2024-2 Q&A L9 (page 76 of this file). It tells plans how to report Roth 401(k) employer contributions in general. The question is “what reporting obligations apply to [Roth employer] contributions?”

Before I state the concerning answer, one must remember the context. This particular Q&A is about reporting, not about taxation. In theory, Roth employer contributions (taxable to the employee) should be simply added to W-2 income for most employees. But that creates a huge headache from a large employer systems perspective. That’s W-2 income that is income tax taxable but not payroll tax taxable. Ugh!

To avoid the payroll systems issue (which is mostly a large employer issue rather than a Solo 401(k) issue), the Notice provides that Roth employer contributions are reported “as if: (1) the contribution had been the only contribution made to an individual’s account under the plan, and (2) the contribution, upon allocation to that account, had been directly rolled over to a designated Roth account in the plan as an in-plan Roth rollover.” (emphases added). The Notice goes on to state that because of this treatment the Roth employer contribution is reported to the employee as taxable on a Form 1099-R.

Mr. Henry-Moreland is concerned that as applied to a Schedule C solopreneur, this is reported by deducting the contribution from net self-employment income (presumably on Schedule 1, Line 16) and then taxing the amount on Form 1040 Lines 5a and 5b. This reduction of net self-employment income would result in a reduction in the Section 199A QBI deduction.

While I hear Mr. Henry-Moreland’s concern, I disagree with it for several reasons. First, the Q&A in question applies to reporting by plans. It does not appear to apply to (1) determining taxable income or other tax relevant amounts and (2) tax return reporting by individuals. It is telling that the answer is silent as to any forms filed by individuals while it goes into depth as to how the Form 1099-R is to be filed.

Second, the words “as if” in the Notice’s answer are illuminating. The reporting is done “as if” X and Y happened for tax purposes. That means X and Y did not happen for tax purposes, which is good news from a Section 199A perspective. Third, the Notice does not purport to affect Section 199A in any way. Fourth, qualified business income is determined under Section 199A and Treas. Reg. Section 1.199A-3. Neither SECURE 2.0 Section 604 nor Notice 2024-2 mention Section 199A and qualified business income. Thus, I believe that Notice 2024-2 and Roth employer contributions to Solo 401(k)s do not reduce the qualified business income deduction.

The above views voiced, there may be some small risk that Roth employer contributions to Solo 401(k)s are not only nondeductible, they also reduce the qualified business income deduction. That’s a negative when assessing their desirability from a planning perspective.

How to Report Solo 401(k) Roth Employer Contributions on 2024 Tax Returns

What follows is my academic opinion, not advice for you or anyone else. To properly report Roth employer contributions to a Solo 401(k) made in 2024 for 2024 and arrive at the correct Section 199A QBI deduction, I believe the following is the best way to proceed:

(1) Report Schedule C income and deductions as normal. This should help generate the appropriate Section 199A QBI deduction.

(2) Report the amount of the Roth employer contribution to the Solo 401(k) in full in Box 5a of Form 1040.

(3) Assuming no other pension, annuity, 401(k), or other qualified plan distributions, report $0 for the taxable amount of pension and annuity distributions in Box 5b of Form 1040.

My view is that the above will properly report that which must be reported to the IRS while also (i) avoiding any double counting and (ii) properly computing the Section 199A QBI deduction that the taxpayer is entitled to.

If anyone at the IRS or the Treasury Office of Tax Policy is reading this, it would very helpful for the government issuing guidance (1) clarifying that no, Roth employer contributions to Solo 401(k)s do not reduce the Section 199A qualified business income deduction and (2) illustrating the proper tax return reporting for Roth employer contributions to Solo 401(k)s.

Third Concern: Planning Desirability

For this section, let’s assume that I am wrong when it comes to the first concern and I am correct regarding the second concern. Making those two assumptions, Roth employer contributions to Solo 401(k)s are valid and do not reduce the Section 199A QBI deduction.

Great!

Does that mean we should plan into such contributions? I believe the answer is generally “No” for most solopreneurs.

Even with the “deduction-reduction problem” issue with traditional Solo 401(k) contributions, traditional Solo 401(k) contributions are often going to be better than Roth Solo 401(k) contributions.

Picture a solopreneur in the 24% marginal tax bracket. He or she can make employer contributions to a traditional Solo 401(k) and save 19.2 cents on the dollar (24% times 80% to account for the reduction to the Section 199A QBI deduction).

Okay, well, how is that money taxed in retirement? I’ve done blog posts and YouTube videos about this subject. Some of that money could be taxed at 0% because of the standard deduction (the Hidden Roth IRA), then against the 10% bracket and then against the 12% bracket. We can hardly say traditional contributions are always the “right answer,” but we can acknowledge that (1) retirees tend to be lightly taxed in retirement and (2) retirees greatly benefit from today’s tax environment, including large standard deductions and progressive tax brackets.

I question the planning value of Roth employer contributions. Say you disagree with me. You still have Roth employee contributions. Why not hedge your bets by making Roth employee contributions and deductible traditional employer contributions? Both of these types of contributions are well established under the law.

Conclusion

Roth employer contributions to Solo 401(k)s are on shaky legal ground and are not that desirable from a planning perspective. There’s even a chance they reduce the Section 199A QBI deduction. Based on those concerns, I believe Roth employer contributions to Solo 401(k)s are undesirable for most solopreneurs.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

Happy New Year! It’s Backdoor Roth IRA season, so let’s talk about the issue that refuses to go away . . . the timing of the two steps of the Backdoor Roth IRA.

Recall that the Backdoor Roth IRA is a two-step transaction. First, there is a nondeductible contribution to a traditional IRA. The second step is a relatively close-in-time conversion of the nondeductible traditional IRA contribution and any minor growth to a Roth IRA. Assuming the correct profile, this can move money into a Roth IRA for a year the person exceeds the Roth IRA contribution MAGI limits.

If there are two steps of the Backdoor Roth IRA, that begs a question: Just how long do I have to wait between the two steps, i.e., how long does the nondeductible traditional IRA contribution have to sit in the traditional IRA prior to the Roth conversion step? A minute? A day? A month? A year?

The Backdoor Roth IRA and the Step Transaction Doctrine

There has been a concern with the Backdoor Roth IRA: the step transaction doctrine, which can collapse steps into a single step. In theory, the two steps of the Backdoor Roth IRA can be viewed as a single step (a direct contribution to a Roth IRA), which creates an excess contribution(subject to a potential 6 percent penalty). Michael Kitces has written that he is concerned that, because the Roth conversion step might occur so soon after the nondeductible traditional IRA contribution, the step transaction doctrine can apply to the Backdoor Roth IRA. Kitces generally advocates waiting a year between the steps based on his step transaction doctrine concern. To my knowledge he has never changed his view on the issue.

Two late 2010’s developments moved the needle in the practitioner community towards Mr. Levine’s view. First, the IRS, in informal comments, indicated they were not too concerned with the Backdoor Roth IRA. Second, the legislative history to 2017’s Tax Cuts and Jobs Act indicated that Congressional staffers believed the Backdoor Roth IRA was valid. I believe this second development was overblown, as legislative history, to the extent relevant, is relevant to the legislation then being passed. It is not relevant, to my mind, to prior legislation (the Backdoor Roth IRA enabling legislation passed in 2006 – see Section 512). That said, both developments were informative, though certainly not binding.

Sean’s Take

I have never been too concerned with the Step Transaction Doctrine and the Backdoor Roth IRA. In 2019, I co-wrote a Tax Notes article (available behind a paywall) about the issue with Ben Willis, my former PwC colleague. We concluded that it is not appropriate to apply the step transaction doctrine to a taxpayer’s use of the explicit, taxpayer favorable IRA rules. I believe we made a good case that the step transaction should not apply to the Backdoor Roth IRA based on the contours of the doctrine.

The Backdoor Roth IRA and Section 408(d)(2)(B)

Since 2019, I have further developed my thinking. I now believe a little commented-on rule in the IRA statute is very instructive: Section 408(d)(2)(B).

Section 408(d)(2)(B) provides that all IRA distributions during the year are treated as a single distribution. As a result, the timing of IRA distributions is irrelevant. A January 1st distribution is treated the same as a March 29th distribution, which is treated the same as a December 31st distribution. Roth conversions are distributions from an IRA.

By grouping all IRA distributions into a single distribution, the Internal Revenue Code tells us the timing of IRA distributions, including Roth conversions, during the year is irrelevant.

It would be exceedingly odd to apply a judicial doctrine (the step transaction doctrine) to give that timing relevance when the Code strips away that relevance. Anyone arguing the step transaction doctrine applies to a Backdoor Roth IRA is saying that the step transaction doctrine should override the specific rule of Section 408(d)(2)(B) in determining the degree of relevance afforded to the timing of the Roth conversion step.

I strongly believe it is not appropriate to apply the step transaction doctrine when the Internal Revenue Code itself gives us a rule telling us the timing of the Roth conversion is irrelevant.

Backdoor Roth IRA Favored Timing

I have two beliefs. First, timing is irrelevant when doing the Backdoor Roth IRA. Second, my views are not guaranteed to yield a 9-0 Supreme Court decision 😉

Based on those two beliefs, I have a third. The most desirable Backdoor Roth IRA path is to wait until the end of a month passes and then do the Roth conversion step of the Backdoor Roth IRA. This is the old Ed Slott tactic and locks in an end-of-month statement showing some interest or dividends in the traditional IRA.

It could look something like this:

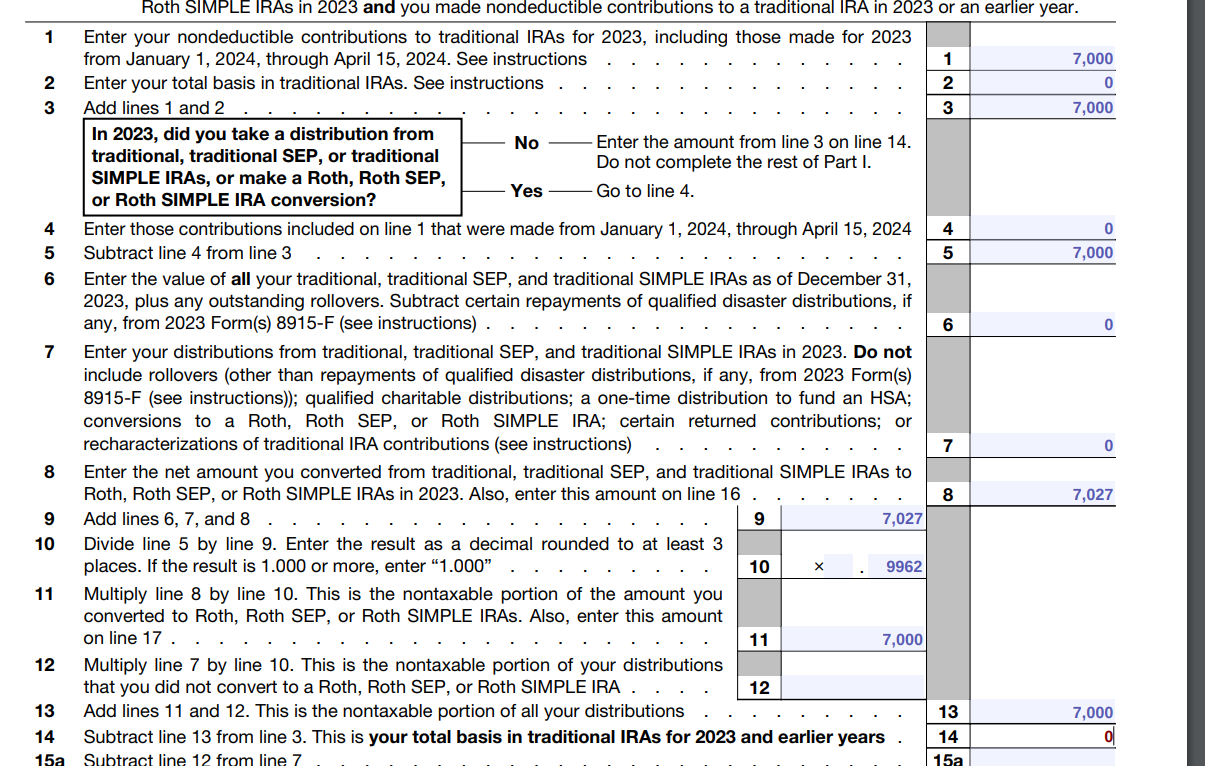

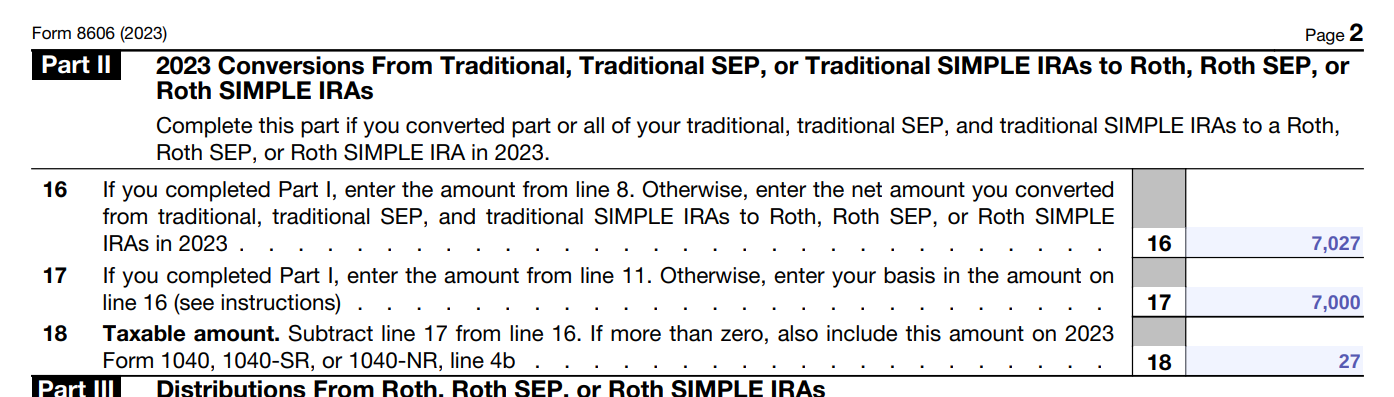

Roger contributes $7,000 to his traditional nondeductible IRA on January 2, 2025 for 2025 and invests it in a money market fund. On February 1, 2025, he converts the entire amount, now $7,027, to a Roth IRA. He has no other IRA transactions during the year and on December 31, 2025 he has $0 balances in any and all traditional IRAs, SEP IRAs, and SIMPLE IRAs.

Oh no, Roger created $27 of taxable income on his Backdoor Roth IRA. We’ve finally found something worse than IRMAA!

All kidding aside, here’s what Roger’s 2025 Form 8606 could look like (pardon the use of the 2023 form, the latest version available as of this writing): 8606 Page 18606 Page 2And, yes, Roger should convert the entire traditional IRA balance, not just the $7,000 originally contributed to the traditional IRA.

To my mind, this works as a good Backdoor Roth IRA. So now you say, But Sean, what about your first belief? I thought timing was irrelevant!

I respond, (A) see my second belief and (B) what’s the downside of my desired approach?

$27 of taxable income creates $10 of federal income tax if Roger is in the highest federal tax bracket, and Roger will have $27 more protected from future tax by the Roth IRA.

The Backdoor Roth IRA Should Not Exist

That the Backdoor Roth IRA exists is ridiculous. It is obnoxious that our tax laws are so complicated that one of the most prominent financial planners, Michael Kitces, could plausibly claim the step transaction doctrine adversely impacts the Backdoor Roth IRA.

Let’s end all of this and adopt a rule that notorious tax haven, Canada, has adopted: Eliminate the income limit on the ability to make an annual Roth IRA contribution! Canada’s Tax-Free Savings Account (their version of a Roth IRA) has absolutely no income limit on the ability to make a contribution. America should adopt that rule as a small part of what hopefully will be a dramatic simplification of American income tax laws in 2025.

Conclusion

I do not believe that the step transaction doctrine should apply to the Backdoor Roth IRA. I do not believe that the timing of the two steps is relevant for determining their ultimate federal income taxation. That said, I like waiting until the following month to do the Roth conversion step.

Of course, the entirety of this article is simply academic commentary. It is not tax, legal, or investment advice for you or anyone else.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

There are only three types of annual contributions to individual retirement accounts (“IRAs”). They are:

Traditional, nondeductible contributions

Traditional, deductible contributions

Roth contributions

This post discusses when a taxpayer can make one or more of these types of annual contributions.

Let’s dispense with what we are not talking about. This post has nothing to do with annual contributions to employer retirement plans (401(k)s and the like) and self-employed retirement plans. We’re only talking about IRAs. The Individual in “IRA” is the key – anyone can set up their own IRA. IRAs are not pegged to any particular job or self-employment.

The above list is the exhaustive list of the possible types of annual contributions you can make to an IRA. But there is plenty of confusion about when you are eligible to make each of the three types of annual contributions.

Two notes on this. First the limit is shared between traditional IRAs and Roth IRAs. In theory, someone under age 50 could contribute $4,000 to a traditional IRA and $3,000 to a Roth IRA. In practice, contributions are rarely divided between the traditional and the Roth, but it does occasionally happen.

Second, the limits have an additional limit: the contribution cannot exceed earned income. This means that those fully retired cannot contribute to an IRA unless they have a spouse who has earned income. A fully retired person (or a homemaker) can use their spouse’s earned income as their earned income and contribute to what is often referred to as a Spousal IRA.

Why Contribute to an IRA?

Why you would consider contributing to an IRA? The main reason is to build up tax-deferred wealth (traditional IRAs) and/or tax-free wealth (Roth IRAs) for your future, however you define it: financial independence, retirement, etc. A second potential benefit is the ability to deduct some annual contributions to traditional IRAs. A third benefit is some degree of creditor protection. States offer varying levels of creditor protection to traditional IRAs and Roth IRAs, while the federal government provides significant bankruptcy protection for traditional IRAs and Roth IRAs.

Traditional Nondeductible IRA Annual Contributions

There’s are only one requirement to contribute to a traditional, nondeductible IRA for a taxable year:

You and/or your spouse have earned income during that taxable year.

That’s it! As long as you satisfy that requirement, you can contribute to a traditional nondeductible IRA, no further questions asked.

Example: Teve Torbes is the publisher of a successful magazine. He is paid a salary of $1,000,000 in 2025 and is covered by the magazine’s 401(k) plan. Teve can make up to a $7,000 nondeductible contribution to a traditional IRA, and Teve’s wife can also make up to a $7,000 nondeductible contribution to a traditional IRA.

There is no tax deduction for contributing to a traditional nondeductible IRA. The amount of your nondeductible contribution creates “basis” in the traditional IRA. When you withdraw money from the traditional IRA in retirement, a ratable portion of the withdrawal is treated as a return of basis and thus not taxable (the “Pro-Rata Rule”).

Example: Ted makes a $6,000 nondeductible traditional IRA contribution for each of 10 years ($60,000 total). When he retires, the traditional IRA is worth $100,000, and he takes a $5,000 distribution from the traditional IRA. Ted is over 59 ½ when he makes the withdrawal. Of the $5,000 withdrawal, Ted will include $2,000 in his taxable income, because 60 percent ($3,000 — $60,000 basis divided by $100,000 fair market value times the $5,000 withdrawn) will be treated as a withdrawal of basis and thus tax free.

Traditional nondeductible IRA contributions generally give taxpayers a rather limited tax benefit. However, since 2010 traditional nondeductible IRA contributions have become an important tax planning tool because of the availability of the Backdoor Roth IRA.

Making a nondeductible IRA contribution requires the filing of a Form 8606 with your federal income tax return.

Traditional Deductible IRA Annual Contributions

In order to make a deductible contribution to a traditional IRA, three sets of qualification rules apply.

ONE: No Workplace Retirement Plan

Here are the qualification rules if neither you nor your spouse is covered by an employer retirement plan (401(k)s and the like and self-employment retirement plans):

You and/or your spouse have earned income during that taxable year.

That’s it! As long as you satisfy that requirement and you and your spouse are not covered by an employer retirement plan, you can make a deductible contribution to a traditional IRA, no further questions asked.

Example: Teve Torbes is the publisher of a successful magazine. He and his wife are 45 years old. He is paid a salary of $1,000,000 in 2025. Neither he nor his wife is covered by an employer retirement plan. Teve can make up to a $7,000 deductible contribution to a traditional IRA, and Teve’s wife can also make up to a $7,000 deductible contribution to a traditional IRA.

TWO: You Are Covered by a Workplace Retirement Plan

Here are the deductible traditional IRA qualification rules if you are covered by an employer retirement plan:

You and/or your spouse have earned income during that taxable year.

Your modified adjusted gross income (“MAGI”) for 2025 is less than $89,000 (if single), $146,000 (if married filing joint, “MFJ”), or $10,000 (if married filing separate, “MFS”).

Note that in between $79,000 and $89,000 (single), $126,000 and $146,000 (MFJ) and $0 and $10,000 (MFS), your ability to make a deductible contribution to a traditional IRA phases out ratably. Here is an illustrative example.

Example: Mike is 30 years old, single, and is covered by a 401(k) plan at work. Mike has a MAGI of $84,000 in 2025, most of which is W-2 income. Based on a MAGI in the middle of the phaseout range, Mike is limited to a maximum $3,500 deductible contribution to a traditional IRA.

Assuming he makes a $3,500 deductible IRA contribution, Mike has $3,500 worth of IRA contributions left. He can either, or a combination of both (up to $3,500) (a) make a contribution to a nondeductible traditional IRA, since he meets the qualification requirement to contribute to a nondeductible traditional IRA or (b) make a contribution to a Roth IRA, since he meets the qualification requirements (discussed below) to contribute to a Roth IRA.

THREE: Only Your Spouse is Covered by a Workplace Retirement Plan

Here are the deductible traditional IRA qualification rules if you are not covered by an employer retirement plan but your spouse is covered by an employer retirement plan:

You and/or your spouse have earned income during that taxable year.

Your MAGI for 2025 is less than $246,000 (MFJ) or $10,000 (MFS).

Note that in between $236,000 and $246,000 (MFJ) and $0 and $10,000 (MFS), your ability to make a deductible contribution to a traditional IRA phases out ratably.

Roth IRA Annual Contributions

Here are the Roth IRA annual contribution qualification rules.

You and/or your spouse have earned income during that taxable year.

Your MAGI for 2025 is less than $165,000 (single), $246,000 (MFJ), or $10,000 (MFS).

Note that in between $150,000 and $165,000 (single), $236,000 and $246,000 (MFJ), and $0 and $10,000 (MFS), your ability to make a Roth IRA contribution phases out ratably.

Notice that whether you and/or your spouse are covered by an employer retirement plan (including a self-employment retirement plan) is irrelevant. You and your spouse can be covered by an employer retirement plan and you can still contribute to a Roth IRA (so long as you meet the other qualification requirements).

Here is an example illustrating your options in the Roth IRA MAGI phaseout range.

Example: Mike is 30 years old, single, and covered by a workplace retirement plan. Mike has a MAGI of $159,000 for 2025, most of which is W-2 income. Based on a MAGI 60 percent through the phaseout range, Mike is limited to a maximum $2,800 contribution to a Roth IRA.

Assuming he makes a $2,800 annual Roth IRA contribution, Mike has $4,200 worth of IRA contributions left. He can make up to $4,200 in annual contributions to a nondeductible traditional IRA, since he meets the qualification requirement to contribute to a nondeductible traditional IRA.

Deadlines

The deadline to make an IRA contribution for a particular year is April 15th of the year following the taxable year (thus, the deadline to make a 2025 IRA contribution is April 15, 2026). The deadline to make earned income for a taxable year is December 31st of that year.

Rollover Contributions

There’s a separate category of contributions to IRAs: rollover contributions. These can be from other accounts of the same type (traditional IRA to traditional IRA, Roth IRA to Roth IRA) or from a workplace retirement plan (for example, traditional 401(k) to traditional IRA, Roth 401(k) to Roth IRA).

Rollover contributions do not require having earned income and have no income limits and should be generally tax-free. For a myriad of reasons, it is usually best to effectuate rollovers as direct trustee-to-trustee transfers.

As a practical matter, it is often the case that IRAs serve at the retirement home for workplace retirement plans such as 401(k)s.

Further Reading

Deductible traditional IRA or Roth IRA? If you qualify for both, it can be difficult to determine which is better. I’ve written here about some of the factors to consider in determining whether a deductible traditional contribution or a Roth contribution is better for you.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

Before we explore new developments for 2025, 2024 was so chock full of Solo 401(k) developments that it deserves its own rundown. Then we will move onto 2025 Solo 401(k) changes.

Vanguard Out!

Vanguard transferred all of their Solo 401(k) accounts to Ascensus in 2024. Vanguard is now entirely out of the Solo 401(k) business.

The good news for those fond of Vanguard is that the Ascensus Solo 401(k) offers Vanguard mutual funds.

The transition was not entirely smooth. Notably, beneficiary designation forms did not transfer from Vanguard to Ascensus. The Ascensus Solo 401(k) contribution portal is quite different from Vanguard’s and is not intuitive, in my opinion. I did a YouTube video about making contributions to a Solo 401(k) at Ascensus.

I’m not in the business of making generic recommendations about which Solo 401(k) plan provider to use. In my book, I advocate strongly for considering a pre-approved plan (sometimes referred to as a prototype plan). Schwab, Fidelity, and Ascensus are now among the larger providers of pre-approved plans. While I will not provide any plan provider recommendation, I believe Ascensus, Fidelity, and Schwab are all reasonable options to consider.

Solo 401(k)s at Retirement

During 2024 I did a deep-dive on some Solo 401(k) history. The results of that research is a 27 page self-published article concluding that for Schedule C solopreneurs, a Solo 401(k) should survive the solopreneur’s retirement.

One of the implications of that finding is that Solo 401(k)s should qualify for the Rule of 55. However, one must always consult with their own individual plan, as the plan itself must have rules facilitating Rule of 55 distributions.

Doubts About SECURE 2.0

SECURE 2.0 made dozens of changes to retirement account rules. It made what I believe to be rather inconsequential changes to Solo 401(k) planning. Nevertheless, it did change some Solo 401(k) rules.

New Solo 401(k) Employee Contributions Limit for 2025

The IRS announced that for 2025, the employee deferral limit for all 401(k)s, including Solo 401(k)s, will be $23,500.

Solo 401(k) Catch-Up Contributions Limit for 2025

The IRS also announced that for 2025, the normal employee deferrals catch-up contribution limit remains $7,500. As a result, those aged 50 or older can contribute, in employee contributions, a maximum of the lesser of $31,000 ($23,500 plus $7,500) or earned income.

New Solo 401(k) All Additions Limit for 2025

The new all-additions limit for Solo 401(k)s is $70,000 (or earned income, whichever is less). For those aged 50 or older during 2025, the $70,000 number is $77,500 ($70,000 plus $7,500).

New Additional Catch-Up Contributions for Those Aged 60 Through 63

SECURE 2.0 increased the catch-up contribution for those aged 60 through 63 (see page 2087 of this file). In 2025, the catch-up contribution for these people is $11,250, not $7,500. As this is a SECURE 2.0 rule, I believe that Solo 401(k) users should (1) proceed with caution and (2) stay tuned.

Traditional Solo 401(k) Contributions More Attractive Than Ever

There’s been plenty of debate: traditional versus Roth. The way to resolve that is to compare today’s marginal tax rate with the tax rate on the income in retirement. Today’s rate is pretty knowable, but tomorrow’s rate isn’t.

That said, we do know that America has a history of standard deductions and graduated progressive tax rates. That, combined with Congress’s political incentives (retirees tend to vote), suggests that retirees will be relatively low taxed in retirement.

Social Security has been a fly in the ointment to that view. Up to 85 percent of Social Security income fills up the standard deduction and lower tax brackets with income. Doesn’t that mean that traditional retirement account withdrawals will be taxed against higher tax brackets?

Starting in 2025, that issue may go away. Eliminating income tax on Social Security was a major promise of the Trump campaign. Considering the GOP majorities in both houses of Congress, the tax on Social Security should be repealed. Stay tuned!

Removing Social Security from taxable income means significant amounts of traditional retirement account withdrawals should be tax free (offset by the standard deduction) or subject to the lower 10 percent and 12 income tax brackets. The possibility of even lighter taxation on traditional retirement account withdrawals makes traditional Solo 401(k) contributions more attractive than ever.

2025 Update to Solo 401(k): The Solopreneur’s Retirement Account

Solo 401(k): The Solopreneur’s Retirement Account explores the nooks and crannies of Solo 401(k)s. On page 16 of the paperback edition, I provide an example of the Solo 401(k) limits for 2022 if a solopreneur makes $100,000 of Schedule C income. Here is a revised version (in italics) of the example (with the footnote omitted) applying the new 2025 employee contribution limit:

Lionel, age 35, is self-employed. His self-employment income (as reported on the Schedule C he files with his tax return) is $100,000. Lionel works with a financial institution to establish his own Solo 401(k) plan and choose investments for the plan. Lionel can contribute $23,500 to his Solo 401(k) as an employee deferral (2025 limit) and can choose to contribute, as an employer contribution, anywhere from 0-20% of his self-employment income.

Lionel’s maximum potential tax-advantaged Solo 401(k) contribution for 2025 is $42,087! That is a $23,500 employee contribution and a $18,587 employer contribution. Note there’s no change in the computation of the employer contribution for 2025 in this example.

On page 18 I provide an example of the Solo 401(k) contribution limits factoring in catch-up contributions. Here’s the example revised for 2025:

If Lionel turned 50 during the year, his limits are as follows:

Employee contribution: lesser of self-employment income ($92,935) or $31,000: $31,000

Employer contribution: 20% of net self-employment income (20% X $92,935): $18,587

Overall contribution limit: lesser of net self-employment income ($92,935) or $77,500: $77,500

Amazon Reviews

If you have read Solo 401(k): The Solopreneur’s Retirement Account, you can help more solopreneurs find the book! How? By writing an honest, objective review of the book on Amazon.com. Reviews help other readers find the book!

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, legal, investment, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, legal, investment, and tax matters. Please also refer to the Disclaimer & Warning section found here.

It’s that time of year again. The air is cool and the Election is in the rear-view mirror. That can only mean one thing when it comes to personal finance: time to start thinking about year-end tax planning.

I’ll provide some commentary about year-end tax planning to consider, with headings corresponding to the timeframe required to execute.

As always, none of this is advice for your particular situation but rather it is educational information.

Urgent

By urgent, I mean those items that (i) need to happen before year-end and (ii) may not happen if taxpayers delay and try to accomplish them late in the year.

Donor Advised Fund Contributions

The donor advised fund is a great way to contribute to charity and accelerate a tax deduction. My favorite way to use the donor advised fund is to contribute appreciated stock directly to the donor advised fund. This gets the donor three tax benefits: 1) a potential upfront itemized tax deduction, 2) removing the unrealized capital gain from future income tax, and 3) removing the income produced by the assets inside the donor advised fund from the donor’s tax return.

In order to get the first benefit in 2024, the appreciated stock must be received by the donor advised fund prior to January 1, 2025. This deadline is no different than the normal charitable contribution deadline.

However, due to much year end interest in donor advised fund contributions and processing time, different financial institutions will have different deadlines on when transfers must be initiated in order to count for 2024. Donor advised fund planning should be attended to sooner rather than later.

Taxable Roth Conversions

For a Roth conversion to count as being for 2024, it must be done before January 1, 2025. That means New Year’s Eve is the deadline. However, taxable Roth conversions should be done well before New Year’s Eve because

It requires analysis to determine if a taxable Roth conversion is advantageous,

If advantageous, the proper amount to convert must be estimated, and

The financial institution needs time to execute the Roth conversion so it counts as having occurred in 2024.

Before the Election, many commentators said “you’ve gotta get your Roth conversions done before tax rates go up in 2026!” If this were X (the artist formerly known as Twitter), the assertion would likely be accompanied by a hair-on-fire GIF. 😉

I have disagreed with the assertion. As I have stated before, there’s nothing more permanent than a temporary tax cut! Now with a second Trump presidency and a Republican Congress, it is likely that the higher standard deduction and rate cuts of the Tax Cuts and Jobs Act will be extended.

Regardless of the particulars of 2025 tax changes, I recommend that you make your own personal taxable Roth conversion decisions based on your own personal situation and analysis of the landscape and not a fear of future tax hikes.

Adjust Withholding

This varies, but it is a good idea to look at how much tax you owed last year. If you are on pace to get 100% (110% if 2023 AGI is $150K or greater) or slightly more of that amount paid into Uncle Sam by the end of the year (take a look at your most recent pay stub), there’s likely no need for action. But what if you are likely to have much more or much less than 100%/110%? It may be that you want to reduce or increase your workplace withholdings for the rest of 2024. If you do, don’t forget to reassess your workplace withholdings for 2024 early in the year.

One great way to make up for underwithholding is through an IRA withdrawal mostly directed to the IRS and/or a state taxing agency. Just note that for those under age 59 ½, this tactic may require special planning.

These items can wait till close to year-end, though you don’t want to find yourself doing them on New Year’s Eve.

Tax Gain Harvesting

For those finding themselves in the 12% or lower federal marginal income tax bracket and with an asset in a taxable account with a built-in gain, tax gain harvesting prior to December 31, 2024 may be a good tax tactic to increase basis without incurring additional federal income tax. Remember, though, the gain itself increases one’s taxable income, making it harder to stay within the 12% or lower marginal income tax bracket.

I’m also quite fond of tax gain harvesting that reallocates one’s portfolio in a tax efficient manner.

Tax Loss Harvesting

The deadline for tax loss harvesting for 2024 is December 31, 2024. Just remember to navigate the wash sale rule.

RMDs from Your Own Retirement Account

The deadline to take any required minimum distributions from one’s own retirement account is December 31, 2024. Remember, the rules can get a bit confusing. Generally, IRAs can be aggregated for RMD purposes, but 401(k)s cannot.

RMDs from Inherited Accounts

The deadline to take any RMDs from inherited retirement accounts is December 31st. For some beneficiaries of retirement accounts inherited during 2020, 2021, 2022, and 2023, the IRS has waived 2024 RMDs. That said, all beneficiaries of inherited retirement accounts may want to consider affirmatively taking distributions (in addition to RMDs, if any) before the end of 2024 to put the income into a lower tax year, if 2024 happens to be a lower taxable income year vis-a-vis future tax years.

Can Wait Till Next Year

Traditional IRA and Roth IRA Contribution Deadline

The deadline for funding either or both a traditional IRA and a Roth IRA for 2024 is April 15, 2025.

Backdoor Roth IRA Deadline

There’s no law saying “the deadline for the Backdoor Roth IRA is DATE X.” However, the deadline to make a nondeductible traditional IRA contribution for the 2024 tax year is April 15, 2025. Those doing the Backdoor Roth IRA for 2024 and doing the Roth conversion step in 2025 may want to consider the unique tax filing when that happens (what I refer to as a “Split-Year Backdoor Roth IRA”).

HSA Funding Deadline

The deadline to fund an HSA for 2024 is April 15, 2025. Those who have not maximized their HSA through payroll deductions during the year may want to look into establishing payroll withholding for their HSA so as to take advantage of the payroll tax break available when HSAs are funded through payroll.

The deadline for those age 55 and older to fund a Baby HSA for 2024 is April 15, 2025.

2025 Tax Planning at the End of 2024

HDHP and HSA Open Enrollment

It’s open enrollment season. Now is a great time to assess whether a high deductible health plan (a HDHP) is a good medical insurance plan for you. One of the benefits of the HDHP is the health savings account (an HSA).

For those who already have a HDHP, now is a good time to review payroll withholding into the HSA. Many HSA owners will want to max this out through payroll deductions so as to qualify to reduce both income taxes and payroll taxes.

Self-Employment Tax Planning

Year-end is a great time for solopreneurs, particularly newer solopreneurs, to assess their business structure and retirement plans. Perhaps 2024 is the year to open a Solo 401(k). Often this type of analysis benefits from professional consultations.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, legal, investment, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, legal, investment, and tax matters. Please also refer to the Disclaimer & Warning section found here.

The 100%/110% safe harbor protects the late-in year lottery winner (among others). As long as he or she has withholding or estimated tax payments that meet 100% or 110% (as applicable) safe harbor, he or she can have millions or billions of dollars in income, meet the safe harbor requirements, avoid the underpayment penalty and pay most of the 2024 tax by April 15, 2025.

Estimated tax payments are great, but they require early in the year action not possible in the fourth quarter. To meet the safe harbor, generally one quarter of the total amount due under the safe harbor must be paid by April 15th, June 15th, September 15th, and the following January 15th. That’s great, but for those who didn’t make the first three payments going into the fourth quarter, estimated tax payments may not be all that helpful at this point.

Most states with an income tax have rules that mirror the federal income tax withholding rules, but some states have differences.

The Retiree’s Secret Weapon for Estimated Tax Payments

Retirees have a secret weapon for making income tax payments, particularly late in the year. IRAs!

People miss paying taxes during the year. It happens for a variety of reasons. If I were a retiree and I found myself underpaid for either (or both) federal and state income taxes purposes in the fourth quarter, the first place I would look to make an estimated tax payment would be a traditional IRA.

Why?

Because income tax withheld from a traditional IRA is deemed paid equally to the IRS throughout the year regardless of when the withholding occurs.

IRA owners can initiate a distribution from their traditional IRA and direct that most of it be directed to the IRS and/or the state taxing authority. That withholding is treated as if it is paid equally throughout the year regardless of whether it occurs on January 5th or December 21st.

That’s pretty good! A late in the year IRA distribution withheld to the IRS can meet either (or both) the 90% safe harbor and/or the 100%/110% safe harbor.

The downside is that it creates taxable income. In many cases, it turns out retirees are rather lightly taxed. As long as the retiree had a relatively low income tax burden either last year or this year, the taxable withdrawal won’t be a large number, because the applicable required safe harbor withholding will be modest. Thus, the tax hit on the mostly withheld distribution should be rather modest.

Another advantage of using a traditional IRA to pay income taxes is RMD mitigation. While I believe the concerns around RMDs are wildly overstated, RMD mitigation is a perfectly valid financial planning objective and a good outcome.

Using an IRA to Pay Income Taxes Under Age 59 ½

You may now be thinking “Sean, that’s a great idea for those over age 59 ½. But what if I’m under age 59 ½? Won’t I be subject to the 10% early withdrawal penalty on the amount I fork over to the IRS?”

That’s an excellent thought! Fortunately, the answer to your questions is “maybe.”

The IRS maintains a list of exceptions to the 10% early withdrawal penalty. Many will not be applicable to most retirees. But there are some options–let’s explore two of them: Inherited IRAs and 72(t) payment plans.

Inherited IRAs

Beneficiaries of inherited IRAs never pay the 10% early withdrawal penalty with respect to distributions from their “inherited IRAs.” Thus, the inherited IRA is a great place to look to pay taxes from late in the year.

The only downside is the distribution to the IRS or the state taxing authority is itself taxable to the beneficiary. However, the money in the inherited IRA has to come out eventually (usually under the 10 year rule at a minimum), so why not whittle the traditional IRA down by using it to pay income taxes and avoid an underpayment penalty?

72(t) Payment Plan to Pay Income Taxes

Could someone start a 72(t) payment plan to pay required income taxes? Absolutely, in my opinion. It might even be a good idea!

72(t) Payment to Pay Income Taxes Example

Homer and Marge both turned age 56 in the year 2024. They retired early in 2023 and thus had some W-2 income and some investment income in 2023. They had approximately $120K of adjusted gross income in 2023 and thus paid approximately $8,800 of federal income taxes in 2023 (see Form 1040 line 24 less most tax credits — see the comment below) and $2,000 of California income taxes in 2023.

In 2024 they have ordinary income below the standard deduction and taxable income below the top of the 12% federal income tax bracket. Thus, they owe no federal income tax and a very small amount of California income tax for 2024. They’ve made no estimated tax payments.

In August 2024 they decided to sell their Bay Area home worth $2M to move to a more rural part of California. The sale closed in October 2024 and they had a $500,000 basis in the home. Qualifying for the $500K exclusion, this triggers a $1M taxable long term capital gain to Homer and Marge in 2024. D’oh!

Very, very roughly, the capital gain creates approximately $175K of federal income tax, $30K of federal net investment income tax, and $100K of California income tax. Note also that the proceeds from the home sale are likely to cause some taxable income in December 2024, but let’s just use the above three tax numbers for illustrative purposes only.

One of their other assets is a $2M traditional IRA. They have no inherited retirement accounts but they do have some taxable brokerage accounts. To my mind, there are four main ways Homer and Marge can avoid an underpayment penalty.

Option 1: Q4 Estimated Tax Payments

Homer and Marge could make substantial fourth quarter estimated tax payments out of their taxable brokerage accounts by January 15, 2025. They would owe 90% their entire 2024 tax liability at that time and would need to use annualization on the Form 2210 to avoid an underpayment penalty.

Compared to the other three methods described below, this costs them 3 months of interest on about $275K. In today’s interest rate environment, that is about $2,700 of interest in an online FDIC insured savings account.

Option 2: IRA Regular Distribution

Homer and Marge could, no later than December 31st, trigger a distribution from one of their traditional IRAs, say for $11,100. They could direct the institution to send $8,880 (80%) to the IRS, $2,109 (19%) to the California Franchise Tax Board, and $111 (1%) to themselves (the intuition will likely require they take at least 1% of the distribution). This creates $11,100 more taxable income (taxed at a low federal rate due to income stacking).

The advantage is this qualifies for the safe harbor, meaning Homer and Marge don’t have to pay most of their 2024 income tax until April 15, 2024. The downside to this is it triggers a 10% early withdrawal penalty ($1,110) payable to the IRS and a 2.5% early withdrawal penalty ($278) payable to California.

Option 3: IRA Regular Distribution and Rollover

This option is the IRA Regular Distribution option plus refunding the $11,100 traditional IRA distribution to the traditional IRA from their taxable accounts within 60 days. This has all the same advantages as the IRA Regular Distribution option plus it reduces 2024 taxable income by $11,100 and avoids the early withdrawal penalties.

Gold, right? My view: I tend to disfavor this tactic. Why? Americans are limited to one 60 day rollover from an IRA to an IRA every 12 months. My personal opinion is that pre-age 59 ½ retirees are usually better served to keep that option on the table. You never know when a significant sum will pop out of a traditional IRA. It will be good to have the option to put that money back into the traditional IRA. If Homer and Marge do the $11,100 IRA Regular Distribution and Rollover, they are locked out from the ability to do a 60 day IRA to IRA rollover for the next 12 months.

Option 4: 72(t) Payment Plan

This option is simply the IRA Regular Distribution option as part of a 72(t) payment plan. The advantage of adding the 72(t) payment plan is avoiding the 10% early withdrawal penalty (federal) and the 2.5% early withdrawal penalty (California).

Here’s how it works. Before making the $11,100 IRA withdrawal, Homer and Marge do a 72(t) distribution calculation and have their financial institution set up a $172,116.10 72(t) IRA. Here is the 72(t) fixed amortization calculation:

Item

Amount

Source

Interest Rate

5.00%

Notice 2022-6

Single Life Expectancy Years at Age 56

30.6

IRS Single Life Table

Account Balance

$172,116.10

Annual Payment

$11,100.00

Homer and Marge then take the distribution from the 72(t) IRA prior to the end of 2024, directing 80% to the IRS and 19% to the Franchise Tax Board.

You say, but wait a minute, now they have $11,100 they have to take annually for each of the following four years. I say, well, okay, they have $2M in tax deferred accounts, why not take some of that without a penalty (perhaps as a form of the “Hidden Roth IRA”) and whittle down future RMDs a bit?

That said, Homer and Marge can drastically reduce the annual 72(t) payment if they want with a one-time change to the RMD method. Assuming the 72(t) balance on December 31, 2024 is $164,000, here’s what the 2025 taxable RMD from the 72(t) could look like:

Item

Amount

Source

Account Balance

$164,000

Single Life Expectancy Years at Age 57

41.6

Notice 2022-6 Uniform Life Table

2025 Payment

$3,942.31

One would hardly expect that $4,000 of taxable income would derail Homer and Marge’s tax planning in retirement. Further, they can direct most of that $4,000 to the IRS and Franchise Tax Board to help take care of 2025 tax liabilities, if any.

Conclusion

For those under age 59 ½, a 72(t) payment plan might be the answer to an underpayment of estimated taxes problem. It is a bit of an “out of the box” solution, but it has several advantages. It allows some taxpayers to delay paying significant amounts of tax until April 15th of the following year by qualifying the taxpayer for the 100% of prior year tax safe harbor. Second, it avoids the 10% early withdrawal penalty. Third, it avoids the once-every-twelve-months 60 day rollover rule. Lastly, a 72(t) payment plan is rather flexible and the required taxable distribution in future years can be significantly reduced by a one-time switch to the RMD method.

The above said, the first IRA I would look to if I was under age 59 ½ and looking to pay estimated taxes is an inherited IRA. Those are never subject to the early withdrawal penalty and can always be accessed in a flexible manner.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters.Please also refer to the Disclaimer & Warning section found here.

I’ve talked about what I refer to as a “72(t) IRA” both here on the blog and on my YouTube channel.

What I haven’t talked much about, until now, is a 72(t) payment plan coming out of a 401(k). Is it possible? Does it make sense?

Inspired by a comment on a recent video, I’m breaking down taking 72(t) payments from a 401(k) in this post. As you will see, when compared with the 72(t) IRA, the 72(t) 401(k) has significant disadvantages.

401(k) Plan Rules

Can you do a 72(t) out of your 401(k)? The answer is “maybe.” Qualified plans, including 401(k)s, have all sorts of unique rules. They vary plan to plan.

There’s no guarantee that you can access partial withdrawals from a 401(k) in accordance with a 72(t) payment plan after a separation from service.

By contrast, IRAs allow for easily accessible partial withdrawals regardless of age.

Must Separate From Service

There’s a tax rule to consider: one can only do a 72(t) payment plan from a 401(k) or other qualified plan after a separation from service from the employer.

From a planning perspective, this is not much of an issue. Few would want to do a 72(t) payment plan while still working, as taxable withdrawals from a 401(k) are not ideal if one still has significant W-2 income hitting their tax return.

72(t) Account Size

According to Notice 2022-6, the 72(t) account balance for the fixed amortization calculation must be determined in a reasonable manner. See Section 3.02(d). The Notice goes on to state that using a balance of the account from December 31st of the prior year through the date of the first 72(t) distribution is reasonable. One should document, usually with an account statement, the balance they are using to have in case the IRS ever examines the 72(t) payment.

Account size is one area where a 72(t) IRA is generally preferable to a 72(t) 401(k). As Natalie Choate observes in her classic Life and Death Planning for Retirement Benefits (8th Ed. 2019), an IRA can be sliced and diced into two or more IRAs, allowing one to take a 72(t) payment from a smaller IRA and remain flexible, in part through having a non-72(t) IRA as well. This flexibility is generally not possible with a 401(k) or other qualified plan. See Choate, page 595. That means without a transfer to an IRA first, the 401(k) account holder is generally stuck with an account size for the fixed amortization calculation, other than the bit of wiggle room given by Notice 2022-6 Section 3.02(d). Further, the entire account is subject to the locked 72(t) cage.

72(t) Locked Cage

A 72(t) 401(k) is entirely subject to the many restrictions on 72(t) retirement accounts. When one uses a 72(t) IRA, they often can have a 72(t) IRA and a non-72(t) IRA. This means less of their retirement account portfolio is subject to the 72(t) rules “locking the cage.” For example, the non-72(t) IRA can be used to accept other IRA roll-ins.

72(t) 401(k) Example

An example can illustrate the problems involved in using a 72(t) 401(k) instead of a 72(t) IRA.

Bob wants to retire early in 2024 at age 53. He has some rental real estate that will generate $40,000 of positive cash flow annually and needs $50,000 more annually from his retirement account to support his lifestyle. He has a $2,000,000 401(k) at his current employer. He sets up a 72(t) 401(k) instead of rolling out to a traditional IRA and establishing a non-72(t) IRA and a 72(t) IRA.

Solving for interest rate, we get an interest rate of -1.015124%.

Notice that in order to generate a $50K annual payment out of a $2M 401(k), Bob must use a negative interest rate. Bob can’t simply ask his 401(k) administrator to establish two separate 401(k) accounts for him and then use a positive interest rate for the 72(t) payment plan.

72(t) Negative Interest Rate

This raises an issue: can a taxpayer use a negative interest rate for a 72(t) payment plan under the fixed amortization method?I believe the answer is Yes. Notice 2022-6 Section 3.02(c) allows an interest rate “that is not more than the greater of (i) 5% or (ii) 120% of the federal mid-term rate (determined in accordance with section 1274(d) for either of the two months immediately preceding the month in which the distribution begins)” (emphasis added).

In my opinion, that wording in no way precludes using a negative interest rate for a 72(t) payment plan. Further, I see no compelling reason for the IRS to be concerned about using a negative interest rate. That said, there is at least some uncertainty around the issue.

The issue is entirely avoided if Bob rolled out to a traditional IRA and then split that traditional IRA into two IRAs. He could have a 72(t) IRA of about $804K generating an annual $50K payment (using a 5% interest rate) and a non-72(t) IRA of about $1.196M. From a planning perspective, it’s certainly my preference to avoid the issue by using the 72(t) IRA.

72(t) Structuring Alternative

As a structuring alternative that might be available to Bob (depending on the plan’s rules), Bob could roll the $804K out to a traditional IRA and use that as a 72(t) IRA. He could keep the balance inside his 401(k) and effectively use his 401(k) as what I refer to as the “non-72(t) IRA.” This sort of structuring was discussed on the Forget About Money podcast (timestamped here).

Unfortunately, using a 72(t) 401(k) boxed Bob into a bad corner. Say Bob is age 57 and the 72(t) 401(k) is still worth exactly $2M. He could use the age 57 factor from the Notice 2022-6 Uniform Life Table (41.6) and reduce his annual payment to $48,077. Not much of a reduction from his $50,000 required annual payment.

Had he used a 72(t) IRA/non-72(t) IRA structure instead, and the 72(t) IRA was worth $804K, he could reduce his $50,000 annual payment all the way down to $19,327.

For those looking for protection against significant tax in the event of an inheritance or other income producing event, the 72(t) IRA is preferable to the 72(t) 401(k).

What if Bob has a 72(t) 401(k)? I believe that establishing a second 72(t) payment from his 72(t) 401(k) would blow up his existing 72(t) payment plan. The second 72(t) payment would be an impermissible modification of the original 72(t) payment plan, triggering the 10 percent early withdrawal penalty and interest charges with respect to all prior distributions.

I am uncomfortable with any modification to a 72(t) retirement account unless it is specifically allowed by IRS guidance such as Notice 2022-6, and I see no evidence that a second 72(t) payment plan out of the same retirement account is permissible. Natalie Choate is also of the opinion that taking a second 72(t) payment from an existing 72(t) account is an impermissible modification of the first 72(t) payment plan. See Choate, page 594. See also IRS Q&A 9 (nonbinding), allowing a new 72(t) payment plan from the retirement account only after the taxpayer has blown up their original 72(t) payment plan.

That said, there is a single 2009 Tax Court case, Benz v. Commissioner, that gives the slightest glimmer of hope. In that case an additional distribution from a 72(t) IRA excepted from the 10% early withdrawal penalty as being for higher education expenses did not blow up an existing 72(t) payment plan, because the additional distribution itself qualified for a 10 percent early withdrawal penalty exception under Section 72(t)(2)(E).

It’s likely a stretch to apply Benz to a second 72(t) payment plan from the same retirement account. That said, I don’t believe it is an impossible outcome. But note that Benz is a single 15 year old court case binding neither on any federal district court nor on any federal appellate court. Further, the IRS never acquiesced to the decision in Benz, meaning they may still disagree with it. Even if the IRS now agrees with Benz they (and more importantly, a court) may not believe the logic of Benz goes so far as to allow a second 72(t) payment plan from the same retirement account.

Asset Protection

Depending on the circumstances and on the state, it can be true that IRAs offer materially less creditor protection than 401(k)s and other qualified plans. That could be a reason to use a 72(t) 401(k) instead of a 72(t) IRA.

I believe that, as a practical matter, sufficient personal liability umbrella insurance, which tends to be affordable, can adequately fill-in gaps between IRA and 401(k) creditor protection. Of course, everyone needs to do their own analysis, possibly in consultation with their lawyers and/or insurance professionals, as to the adequacy of their creditor protection arrangements.

72(t) Payment Plan Resources

72(t) payment plans are complex. Here are some resources from me and other content creators for your consideration:

The 72(t) 401(k) is a possibility if one’s 401(k) plan allows it. I usually strongly disfavor doing a 72(t) payment plan out of a 401(k) considering how rigid it is compared to the 72(t) IRA alternative. Further, as discussed above, 72(t) 401(k)s can create situations where the tax law has not, to my knowledge, definitely stated the governing rules. For these reasons, I generally favor using 72(t) IRAs in conjunction with non-72(t) IRAs instead of the more inflexible 72(t) 401(k).

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters.Please also refer to the Disclaimer & Warning section found here.

“Repay to Caesar what belongs to Caesar and to God what belongs to God.” – Matthew 22:21

What happens with our IRAs and other retirement accounts when we die? Early in our financial journeys, it is incredibly important to plan for our retirement accounts to take care of our loved ones, particularly spouses and younger children. Those concerns should be the primary drivers of the planning for our retirement accounts early on.

But what about later in our lives, when our financial futures are secured and our children are adults?

I believe it is time to be intentional about the destination of our tax deferred retirement accounts. It’s great to provide for adult children. But how much? And couldn’t retirement accounts help better the world? As discussed below, the Church IRA is a way to give wealth to adult children and to the Church.

The Origins of an Idea

In August 2023 the combination of a West Coast hurricane and the Podcast Movement conference resulted in my flying to Denver, Colorado on a Saturday to ensure I could attend the conference. As a result, I attended Sunday Mass far from home at St. Gianna Beretta Molla Church in Denver. At that Mass, the homilist, Deacon Steve Stemper, had an idea that spoke to me: treat the Church as one of your children in your estate plans.

The Church IRA

As frequent readers of the blog know, I’m quite interested in tax-advantaged retirement accounts. The idea to treat the Church as one of your children in your estate strikes me as particularly well suited for traditional IRAs.

Let’s illustrate with an example:

Chuck and Joy are married and both are 85 years old. They have a $3M traditional IRA in Chuck’s name, and they have three adult sons: Abe, Barry, and Charlie, in their late 50s and early 60s.

Obviously, if Chuck dies, Joy needs support. Why not name Joy as the primary beneficiary of the traditional IRA? That leaves a remaining question: who should be the secondary beneficiaries?

Each of Abe, Barry, and Charlie could be a one-third secondary beneficiary. At the second death, they would get about $1M each. What if instead Chuck names each of Abe, Barry, and Charlie one-quarter secondary beneficiaries (about $750K each) and names his Catholic parish or diocese as a one-quarter secondary beneficiary (also about $750K)?

This is the beginning of what I refer to as the Church IRA.

How much different will Abe, Barry, and Charlie’s lived experience be by inheriting a $750K traditional IRA instead of a $1M traditional IRA?

Further, the “hit” to Abe, Barry, and Charlie is likely to be less than a 25% reduction. Why? Because of taxes!

Each of Abe, Barry, and Charlie will have 10 years to drain the inherited IRA. Odds are they will want to take more than 10% per year from the IRA to manage a potential “Year 10 Tax Time Bomb.” Say Abe is single and otherwise has annual income of $150,000.

If Abe takes 12.5% of the account in the first full year after death, he takes $125,000 if he inherits a $1M traditional IRA. Assuming he takes the standard deduction, Abe will be in the 35% marginal tax bracket.

If, instead, Abe inherits a $750K traditional IRA, he only takes $93,750 in the first year. With the other $150K of AGI, Abe will find himself in the 32% marginal tax bracket.

The $31,250 that the Church IRA costs Abe during the year would have been taxed at 32% and 35% federal income tax rates. This illustrates that reducing Abe’s inherited IRA by 25% is not likely to cost him 25% of the after-tax wealth since it is likely he would pay a significantly higher tax rate on those last dollars.

You could say Chuck and Joy “took” money from Abe, Barry, and Charlie by employing the Church IRA. The money they took from Abe, Barry, and Chuck and gave to the Church is the highest taxed money, making the Church IRA tax efficient.

The Church IRA and the Owner’s Needs

One of the advantages of the Church IRA is it need not risk the owners’ own retirement sufficiency. Joy has a legitimate interest in her own financial future. The initial Church IRA structure has the advantage of reducing Chuck and Joy’s ability to fund the remainder of their own lives in no way. The Church gets money only after they have both passed.

Church IRA Implementation

To my mind, the biggest question here is whether to create the Church IRA during our lives or at death. In Chuck and Joy’s case, assuming they want to, at a minimum, employ the Church IRA at death, there are three options:

PATH ONE: Keep everything in a single IRA during their lifetimes. Have the four equal secondary beneficiaries.

PATH TWO: Split the single IRA into four IRAs, each with its own 100% secondary beneficiary (Abe, Barry, Charlie, and the Church IRA)

PATH THREE: Split the single IRA into two IRAs (one worth $2.25M with Abe, Barry, and Charlie as the secondary beneficiaries and a second IRA worth $750K with the Catholic Church as the sole secondary beneficiary).

One of the advantages of the second and third paths is the Church IRA can serve additional purposes. One additional Church IRA purpose is that it be used during Chuck and Joy’s lifetimes to make their routine contributions to the Church (whether that be weekly or monthly). Those contributions can be made through qualified charitable distributions (“QCDs”).

QCDs are a great tax planning tactic during one’s own lifetime for the charitably inclined. They get money out of a traditional IRA tax-free and count against required minimum distributions (“RMDs”).

Regardless of the chosen path, the Church IRA can also be used during Chuck and Joy’s lifetime to help them fund their own living expenses.

We see that the Church IRA can be simply used at death through beneficiary designation forms. Or the Church IRA can also work during one’s own life to either or both (i) provide for routine lifetime Church donations (preferably through QCDs) and (ii) provide for the owner’s own living expenses.

Splitting IRAs

IRA owners can work with their financial institution to split an existing IRA into two or more IRAs. This can be done for any reason. Perhaps it’s simply for mental accounting to facilitate a Church IRA like the one in Paths Two and Three described above.

One does not need to split IRAs to facilitate the Church IRA (see Path One above). But there can be simplicity advantages to having each beneficiary have their own separate and distinct IRA they inherit separate from other siblings and/or the Church.

RMDs from Split IRAs

Here the tax rules are quite flexible. The tax rules treat all of one’s traditional IRAs as a single traditional IRA for RMD purposes. So Chuck and Joy would have tremendous flexibility in terms of which IRA or IRAs to take their overall RMD for the year from. They could take the RMD from the Church IRA or from one or more of the non-Church IRAs, or they can split it among their various IRAs however they want to.

Changing Beneficiaries at the First Death

In Chuck and Joy’s situation, there is an important additional consideration. What if Chuck dies first? Joy would inherit the traditional IRA. She would then need to work with the financial institution to appropriately roll the inherited IRA into an IRA into her own IRA.

From there, she should name primary beneficiaries in accord with her Church IRA intention. She has the three paths described above as possibilities for structuring her Church IRA.

Roth Versus Traditional

Absent incredibly rare circumstances, the Church IRA should be a traditional IRA. Roths are tax-free to individual beneficiaries. Traditional IRAs are taxable to individual beneficiaries. If your adult children are getting some and the Church is getting some, why not leave Roths to the adult children and some or all of the traditional IRAs to the Church?

The adult children pay income tax and the Church does not. Why waste the tax-free attribute of the Roth on a tax-free entity, the Church? The Church does not benefit from Roth treatment while the adult children do.

Perhaps the beneficiary designation forms split the Roth IRA only among the adult children and split the traditional IRA among the adult children and the Church, and leave a greater percentage of the traditional IRA to the Church.

Conclusion

The Church IRA can flexibly leave a share of one’s financial wealth to the Church or other 501(c)(3) charity. It can help us repay to God what is God’s while reducing what is owed to Caesar.

To determine whether the Church IRA is appropriate for us, we need to ask ourselves several questions. How much do my adult children need? Should I leave a significant amount to my Church or other charities? Are there tax-efficient ways to provide for both the Church and my adult children?

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

Some potential “early” retirees are thinking about the so-called “Rule of 55” and many of them have Roth 401(k)s.

How does the Roth 401(k) work with the Rule of 55? Is there a better option than the Rule of 55 for those looking to retire using in part or in whole a Roth 401(k) prior to turning age 59 ½?

We will explore both the Roth 401(k) and the Rule of 55, then we will discuss planning involving the potential combination of the Roth 401(k) and the Rule of 55. We will also discuss a planning alternative to combining the Roth 401(k) with the Rule of 55.

Roth 401(k)

The Roth 401(k) is a 401(k) that is taxed as a Roth. Employers offering a 401(k) are not required to offer a Roth 401(k) option, but many do.

Roth 401(k) Contributions

There are now three main potential sources of “Roth contributions” to a Roth 401(k).

Employee Deferrals: In 2024, these are limited to the lesser of earned income or $23,000 ($30,000 if age 50 or older). These are done through W-2 withholding into the Roth 401(k).

Mega Backdoor Roth: These are after-tax contributions by the employee (also through W-2 withholding) to the traditional 401(k) followed by a soon-in-time Roth conversion of the after-tax 401(k) amount to the Roth 401(k).

Employer Contributions: Employers contribute to 401(k)s. SECURE 2.0 allows for employers to contribute to Roth 401(k)s. Traditionally, employer contributions had always been to the traditional 401(k), but SECURE 2.0 established the possibility of Roth 401(k) employer contributions. Note that a February 2024 federal court decision has called SECURE 2.0 into question.

There’s a limit on the combination of 1 plus 2 plus 3. I refer to this limit as the “all additions limit” and some refer to it as the “415(c)” limit, as that’s where the limit lives in the Internal Revenue Code. For 2024, the all additions limit is $69,000. For those aged 50 or older, it is $76,500.

There’s a fourth potential source of Roth 401(k) funds: Taxable conversions from traditional 401(k)s. Taxable Roth conversions (traditional 401(k) to Roth 401(k)) have no limit. These are usually not done during one’s working years.

Roth 401(k) Withdrawals

If “done right” a Roth 401(k) withdrawal in retirement is fully tax and penalty free.

However, if a distribution from a Roth 401(k) occurs before either (or both) the account owner is 59 ½ years old or the owner has owned that particular Roth 401(k) for five years, the “earnings” portion of the distribution is subject to ordinary income tax and the potential 10 percent early withdrawal penalty.

Here’s a quick example illustrating that rule: