Few things seem to generate more confusion than the Pro-Rata Rule.

It’s time for the FI Tax Guy to tackle it head on!

The Rule

For all the confusion about the Pro-Rata Rule, it is actually a very simple rule. All the Pro-Rata Rule says is that IRA Basis is allocated between two things.

One thing is IRA distributions and Roth conversions occurring during the year. The second thing is balances in traditional IRAs, SEP IRAs, and SIMPLE IRAs as of December 31st of the year.

If you understand the three bolded concepts, none of which are rocket science, you can easily master the Pro-Rata Rule.

The Pro-Rata Rule means that taxpayers can’t “cherry pick” to say that all of a distribution or Roth conversion goes against existing basis if there are traditional/SEP/SIMPLE IRA balances at year-end. Rather, that IRA Basis is proportionately allocated, based on value, between the distributions and Roth conversions on one hand and year-end balances on the other.

IRA Basis

IRA Basis exists to ensure amounts that were never deducted on their way into a traditional retirement account are not taxed on the way out.

As I previously wrote, IRA Basis emerges from two sources. The first is nondeductible traditional IRA contributions. These are reported on Form 8606 filed with one’s annual federal income tax return.

IRA Basis is to the Backdoor Roth IRA what the flux capacitor is to time travel: it’s what makes it possible.

Nondeductible Traditional IRA Contributions

Here’s an example of how a nondeductible traditional IRA contribution creates IRA Basis:

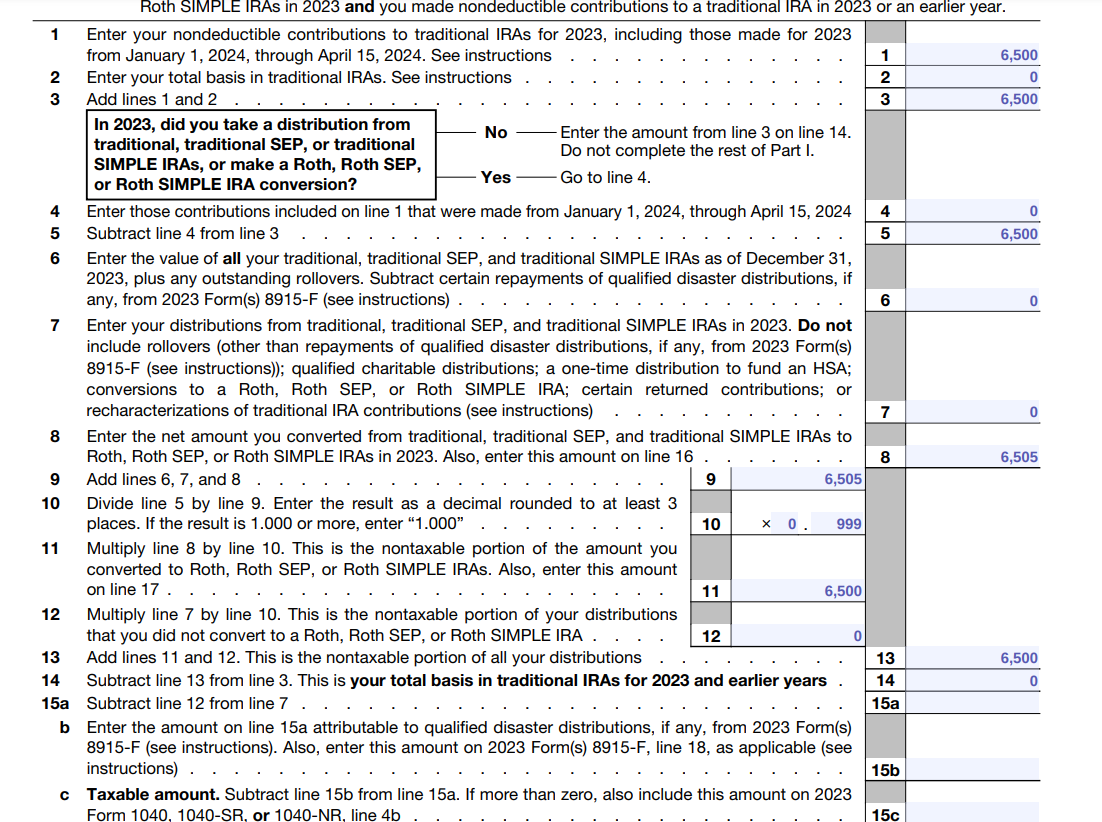

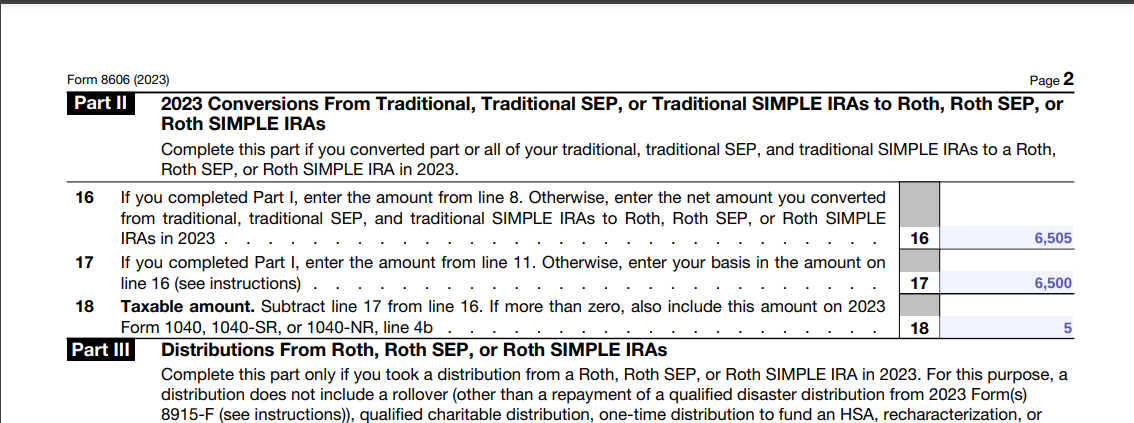

Example 1: Emmett contributed $6,500 to a nondeductible traditional IRA on January 2, 2023. At that time and on December 31, 2023, Emmett had no other balances in traditional IRAs, SEP IRAs, and SIMPLE IRAs. That $6,500 contribution creates $6,500 of IRA Basis. On February 1, 2023, Emmett converted the entirety of his traditional IRA, then $6,505, to a Roth IRA. Emmett did a successful Backdoor Roth IRA, and as a result, just $5 is taxed to him ($6,505 minus $6,500) since he recovers the $6,500 of basis created by the nondeductible traditional IRA contribution when determining the taxation of the Roth conversion.

Here is Part I of Emmett’s Form 8606 and here is Part II. Note that tax return software programs may not complete Part I but instead present it as a worksheet or statement.

{kind=link}

{kind=link}

In terms of the Pro-Rata Rule, 100% of Emmett’s $6,500 IRA Basis was allocated to his IRA distributions and Roth conversions during the year and 0% of Emmett’s $6,500 IRA Basis was allocated to his traditional/SEP/SIMPLE IRA balances on December 31st, since Emmett had no basis in traditional IRAs, SEP IRAs, and SIMPLE IRAs as of December 31st.

After-Tax Contributions to Workplace Retirement Plans

The second source of IRA Basis is after-tax contributions to workplace retirement plans. These are not deducted when made.

I’ve seen these occur in two contexts, though there are others. The first is after-tax 401(k) contributions, which oftentimes are done as part of a Mega Backdoor Roth IRA. Note that Mega Backdoor Roths exhaust the basis. The second context is a mandatory 401(a) plan. These are retirement plans sometimes offered by nonprofit organizations (educational institutions, hospitals, etc.). These plans sometimes require employees to make after-tax contributions to the retirement plan.

Transfers of after-tax basis in workplace plans to traditional IRAs create IRA Basis. However, in today’s environment, after-tax contributions not used up by Mega Backdoor Roths should not end up in traditional IRAs. Rather, they should end up in Roth IRAs under the rules available under Notice 2014-54. I discussed moving workplace after-tax contributions to Roth IRAs in this post.

IRA Distributions and Roth Conversions During the Year

This the second concept to understand: IRA distributions and Roth conversions during the year. These are reported to the IRS and taxpayers annually on a Form 1099-R.

The tax law treats all IRA distributions and Roth conversions as a single combined distribution for purposes of applying the Pro-Rata Rule.

This number is computed based on the relevant year. Unlike an IRA contribution, distributions or Roth conversions made after year-end cannot be designated as being for the current year.

Distributions and Roth conversions from qualified workplace retirement plans (such as 401(k)s) are not included in this number.

Rollovers and other transfers that end up back inside a retirement account are not included in this number.

Traditional IRA, SEP IRA, and SIMPLE IRA Balances on December 31st

Only one day matters! December 31st!

Financial institutions report to both the IRS and the taxpayer their year end traditional IRA, SEP IRA, and SIMPLE IRA balances on a Form 5498.

Amounts in qualified workplace retirement plans (such as 401(k)s) are not included in this number, though SEP IRAs and SIMPLE IRAs are included in this number.

As you can see on line 6 of the Form 8606, you must include “outstanding rollovers” in your December 31st balance. Without this rule, people could avoid the Pro-Rata Rule by taking a distribution from their IRA late in the year and refunding it (within 60 days) early the following year, essentially hiding the money from the December 31st balance amount.

Pro-Rata Rule FAQ

Do I Need To Be Worried About the Pro-Rata Rule?

Yes but only if (1) you take (or consider taking) a traditional IRA, SEP IRA, and/or SIMPLE IRA distribution or convert (or consider converting) an IRA to a Roth IRA and (2) you have IRA Basis.

If either or both do not apply to you, the Pro-Rata Rule has no relevance to your financial life.

Does the Pro-Rata Rule Apply for Purposes of Assessing the 10% Early Withdrawal Penalty?

Yes, but see the Roth conversion paragraph below.

The early withdrawal penalty does apply to regular withdrawals from traditional IRAs, SEP IRAs, and/or SIMPLE IRAs if the account owner is under age 59 ½. The amount of basis recovered under the Pro-Rata Rule is relevant, since only the taxable portion of the IRA distribution can be subject to the 10% early withdrawal penalty.

Note that exceptions to the 10% early withdrawal penalty can apply if one is under age 59 ½, including but not limited to 72(t) payments.

If the transaction is a Roth conversion, the 10% early withdrawal penalty does not apply, regardless of age, so it doesn’t matter how much of the Roth conversion is taxable. The 10% early withdrawal penalty simply never applies.

What Are the Exceptions to the Pro-Rata Rule?

The Pro-Rata Rule applies to nearly all movements of assets out of traditional IRA, SEP IRA, and SIMPLE IRAs. However, there are exceptions.

- Transfers from IRAs to qualified plans such as 401(k)s (I wrote about this rule in this post, see Steps 2 and 3 of the Case Study)

- Qualified charitable distributions (QCDs)

- Qualified HSA funding distributions (QHFDs)

If any of the above three apply, IRA Basis stays behind in the IRA and is not diminished by the transaction. The Pro-Rata Rule does not apply to these three transactions.

The Pro-Rata Rule also has no application to nontaxable rollover distributions of IRA assets (i.e., distributions that wind up back in IRAs).

I Have an Old Traditional 401(k) (No Basis) That I Rolled to a Separate Traditional IRA. That Doesn’t Count for Pro-Rata Rule Purposes, Correct?

Incorrect!

The Internal Revenue Code is quite clear: all traditional IRAs, SEP IRAs, and SIMPLE IRAs are aggregated and treated as a single traditional IRA for purposes of applying the Pro-Rata Rule. The rules don’t care about the origin of the IRA.

I Inherited a Traditional IRA from My Father and Inherited a Traditional IRA from My Aunt. They Both Had IRA Basis. Does That Basis Get Added to My Own IRA Basis?

No!

However, that basis goes with each inherited IRA. Each inherited IRA is hermetically sealed. So IRA Basis inherited from your father attaches only to the IRA inherited from your father. The IRA Basis inherited from your aunt only attaches to the IRA inherited from your aunt. Those two IRA Bases are not commingled. See Natalie B. Choate’s treatise Life and Death Benefits for Retirement Planning (8th Ed. 2019), page 151.

Isn’t the Pro-Rata Rule a Bad Rule That Should be Repealed?

Mostly no.

The Pro-Rata Rule reasonably sets forth how basis is recovered when withdrawing or converting money. Allowing taxpayers to “cherry pick” but having distributions or conversions access IRA Basis fully before accessing taxable amounts could make RMDs nontaxable to start off (effectively increasing the delay in taxation of deferred retirement accounts).

I believe the answer to eliminate Pro-Rata Rule confusion is to eliminate nondeductible contributions to retirement accounts, as I discussed in proposal number 5 of my retirement tax reform proposal.

Once there are no more after-tax contributions to retirement accounts, there’s no more IRA Basis. Once there’s no more IRA Basis, there’s no need for the Pro-Rata Rule.

Is the Pro-Rata Rule Applied Differently to Roth Conversions Than It Is to Regular IRA Distributions?

No difference whatsoever.

I will add one quick point: IRA distributions can be subject to the 10% early withdrawal penalty (as discussed above) while Roth conversions can never be subject to the 10% early withdrawal penalty, so as applied to regular IRA distributions the Pro-Rata Rule can be more impactful (since recovered basis avoids both ordinary income tax and the 10% early withdrawal penalty). But the application is the exact same.

Pro-Rata Rule Example

Since I’m writing this at year-end, I’ll borrow from some of my previous work in providing this example.

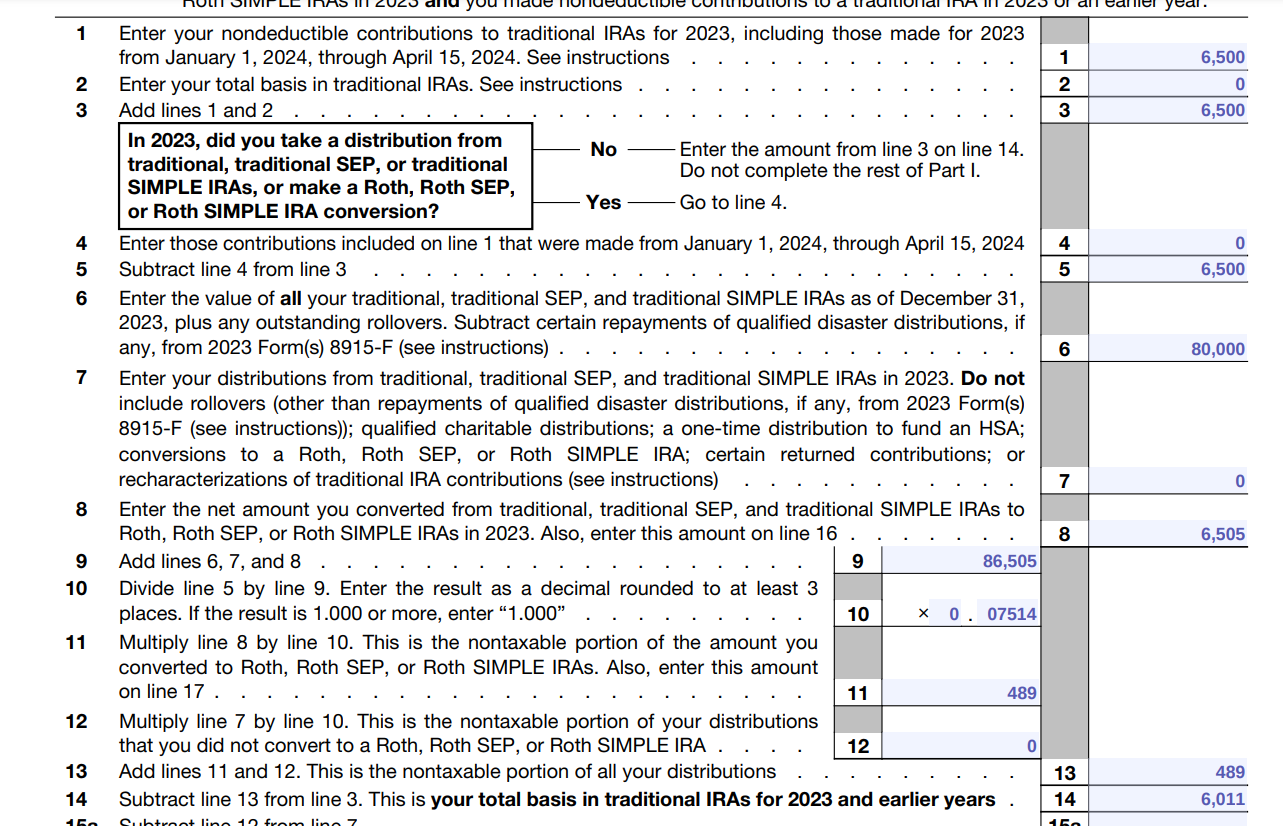

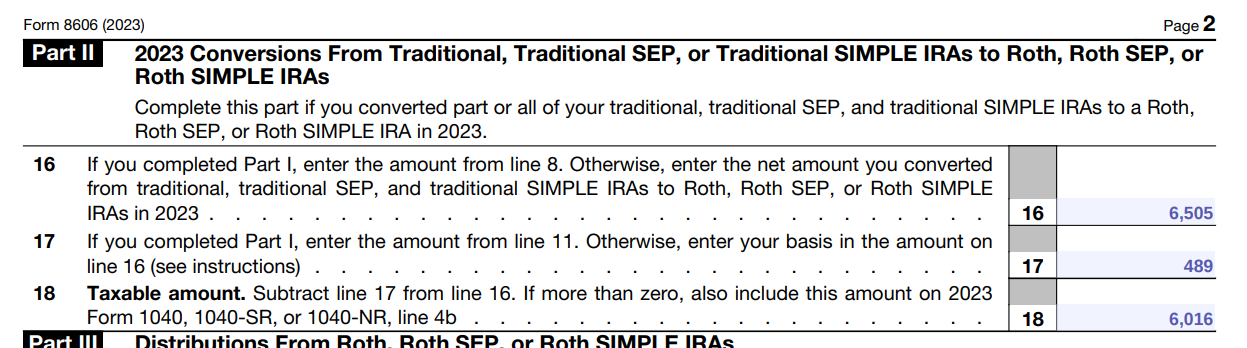

Example 2: Joe contributes $6,500 to a nondeductible traditional IRA on January 2, 2023. On February 1, 2023, when the traditional IRA is worth $6,505, Joe converts the entire balance to a Roth IRA. On December 31, 2023, Joe had $80,000 in an old traditional IRA (a rollover of an old 401(k)). That IRA has no basis.

The Pro-Rata Rule applies here to say “Okay, Joe has $6,500 in IRA Basis. How do we divide that up between (1) Joe’s $6,505 Roth conversion and (2) Joe’s $80,000 December 31st traditional IRA balance?”

The Pro-Rata Rule divides that amount proportionally based on the value of those two things. When we add $6,505 to $80,000 we get $86,505. The Roth conversion is 7.52% of the combined total ($6,505 divided by $86,505) and the December 31st IRA balance is 92.48% of the combined total ($80,000 divided by $86,505).

Thus, the Roth conversion attracts 7.52% of the IRA Basis ($489) and the December 31st IRA balance attracts 92.48% of that IRA Basis ($6,011). As a result, $6,016 of the Roth conversion is taxable ($6,500 minus $489) and Joe will go into 2024 with $6,011 of IRA Basis.

Here is Part I of Joe’s Form 8606 and here is Part II.

{kind=link}

{kind=link}

Watch me discuss how to compute the Pro-Rata Rule in Google Sheets.

More Pro-Rata Rule Posts

The Pro-Rata Rule has a significant impact on Backdoor Roth IRA planning. I cover that in these three posts:

Backdoor Roth IRAs for Beginners

What to Do if You Don’t Qualify for a Backdoor Roth IRA

The Backdoor Roth IRA and December 31st

Basis Isolation planning can be very impactful and help avoid taxation under the Pro-Rata Rule. I discussed that planning here.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

Follow me on Twitter: @SeanMoneyandTax

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

This is awesome Sean.

If Joe contributed after the end of the year (before filing his tax return) would the entire $6,500 be taxable?

It looks like line 10 is 0% if $6,500 goes on line 4.

Thanks!

Penny, thanks for reading and for the kind words. I appreciate them.

I reviewed the Form 8606, and in your counterfactual (converting $6,505 first in 2023 then later contributing $6,500 for 2023 in 2024) it appears you are correct. You don’t appear to get “basis credit” for a 2023 contribution made in 2024 until 2024. Before weighing in that I 100% agree with that outcome I’d want to review the law myself, but that appears to be the IRS conclusion and I have no reason to suspect they are incorrect.

Absolutely great website full of extremely useful information!

I have been putting considerable effort into understanding the pro-rata rule but continue to find it challenging to fully grasp. I would greatly appreciate your assistance in clarifying my specific situation.

I have an old 401(k) with only pre-tax contributions that I rolled over into a traditional IRA a few years ago, and I have not made any contributions to it since. Based on my understanding (which may be incorrect), I decided to roll over this IRA into my current 401(k) plan to eliminate having an IRA basis.

However, I was unaware that dividend accruals would prevent me from fully rolling over the balance in a single transaction and I ran out of time. As a result, on December 31st, my IRA balance is $0.01.

Earlier this year, I executed a mega-backdoor Roth conversion by rolling over $41,000 from my current 401(k) into my Roth IRA. This amount was contributed a year earlier as after-tax contributions, with an immediate Roth in-plan conversion, making it part of my 401(k) Roth.

Could you help me understand how the pro-rata rule applies in this scenario? Thank you in advance for your time and expertise!

Seb, Merry Christmas and Happy New Year to you! Thank you for reading and commenting.

Unfortunately, I can’t address individual circumstances on the blog. I can say, in an academic sense, that end of year balances of less than $1 in a traditional IRA, by themselves, have no consequential impact on the taxation of IRA distributions, including but not limited to Roth conversions.

I appreciate your academic explanation, thank you for responding.

I came across this website as i was researching the topic and it’s been informative and easy to understand. Thanks so much.

But i do have a question on your example with Joe. Since he rolled over an old 401k to traditional ira of $80k that’s what triggered and caused the pro-rata rule. To avoid this in the future i read that he can roll it back to a qualified employer’s retirement account to avoid triggering the prorata rule. So let’s say the following year in 2024, he rolled back the $80k from a traditional ira to an employer 401k before year end. and let’s assuming the $80,000 is all pretax. If he rolls that over to a current employer’s 401k plan, then he will no longer have any balance in 2024 for the traditional IRA. As a result, he can do a full backdoor Roth IRA again correct? But my question now is what happens to the basis of $6011 that is carried forward to 2024? He no longer has a traditional IRA account since he would have rolled it back to an employer’s qualified retirement account. Also the fund of $6505 was fully converted to a Roth instead so what happens to the carryover basis?

I feel like I may have misunderstood something so Thanks for your clarification.

Ellen, thanks for commenting. You’re asking a great question and one that involves advanced planning concepts. Please understand my comments below are academic in nature — not advice for you or anyone else.

The answer is that if Joe wants to do a “roll in” from the traditional IRA to his 401(k) that is fine, so long as the 401(k) accepts IRA roll-ins. They are not required to do so. Assuming they do accept roll-ins, we now come upon a tax rule: IRA basis cannot be rolled into a 401(k) or there qualified plan. So Joe would need to leave $6,011 (I’d recommend a smidgen more to be safe) behind in the traditional IRA and only roll amounts above that basis amount to the 401(k). So that basis stays alive inside the traditional IRA.

This sets Joe up for what I refer to as the “Basis Isolation Backdoor Roth IRA.” Once he’s moved the amounts above $6,011 (and some change) to his 401(k), he can Roth convert the remainder of the traditional IRA to a Roth IRA and most of it will be a tax free recovery of basis. I did a blog post on this blog titled “The Basis Isolation Backdoor Roth IRA” you might be interested in reading for more information.

If we contribute less than the actual limit in Traditional IRA (e.g. $100 less than max allowed for that year) and if there’s $5 interest in Traditional IRA, then I assume it does not go in pro-rata? Since eventually we are converting $5 also to Roth.

Parag, thank you for commenting. I can’t provide any individual advice. But I can offer two academic insights. First, very small amounts tend to have immaterial tax effects. Second, you may want to review the “Roger” example in my Backdoor Roth IRA Timing blog post — you may find it insightful: https://fitaxguy.com/backdoor-roth-ira-timing/

You give an example of contributing to a traditional IRA in early January and converting via distribution in early February of the same year, say 2026. What about a contribution in December 2025 for the 2025 tax year, converted in February 2026, with a subsequent contribution in March 2026 for the 2026 tax year, converted in May 2026. Does this raise any issues given the two conversions in the same year? How does it affect the 8606 reporting? And does it matter if the same account is used for the after-tax traditional contribution? Of course, there may be other issues raised by these questions so feel free to expound.

Thanks for commenting.

Not to brag, but I’ve probably done more content about “Split-Year Backdoor Roth IRAs” than anyone on the planet. If you or anyone else can provide an example who has written or spoken more about this niche topic, please let me know. Some examples: https://fitaxguy.com/split-year-backdoor-roth-iras/ https://www.youtube.com/watch?v=OezHVXU57fE https://fitaxguy.com/the-backdoor-roth-ira-after-an-excess-contribution-to-a-roth-ira/