There’s a tax increase in the new SECURE Act 2.0 legislation. Unfortunately, it falls largely on those least equipped to shoulder it.

Catch-Up Contributions

Since enacted in 2001, “catch-up” contributions have been a great feature of 401(k) plans. Currently, they allow those age 50 or older to contribute an additional $6,500 annually to their 401(k) or similar plan. Those contributions can be traditional deductible contributions, Roth contributions, or a combination of both.

The idea is that by age 50, workers have much less time to make up for deficiencies in retirement savings. Thus, the law allows those workers to make catch-up contributions to have a better chance of financial success in retirement.

Other than age (must be at least 50 years old), there are no limits on the ability to make catch-up contributions. That could be viewed as a give-away to the rich. However, it is logical to keep retirement savings rules simple, especially those designed to help older workers behind in retirement savings.

Watch me discuss SECURE 2.0’s tax increase on catch-up contributions

Catch-Up Contributions for Those Behind in Retirement Savings

For those behind in retirement savings, deducting catch-up contributions usually makes the most sense. First, many in their 50s are in their highest earning years, and thus tax deductions are their most valuable. Second, those behind in retirement savings are not likely to be in a high tax bracket in retirement. With modest or low retirement income, they are likely to pay, at most, a 10% or 12% top federal income tax rate in retirement.

Here is an example of how that works:

Sarah, single and age 55, is behind in her retirement savings, so she maxes out her annual 401(k) contribution at $27,000 ($20,500 regular employee contribution and $6,500 catch-up contribution). Sarah currently earns $130,000 a year and lives in California. Since she deducts her catch-up contributions, she saves $2,165 a year in taxes ($6,500times 24% federal marginal tax rate and 9.3% California marginal tax rate).That $2,165 in income tax savings makes catching up on her retirement savings much more affordable for Sarah.

Sarah’s approach is quite logical. If things work out, Sarah can make up the deficit in her retirement savings. Doing so might push her up to the 12% marginal federal tax bracket and the 8% marginal California tax bracket in retirement.

For someone like Sarah who is behind in their retirement savings, the Roth option on catch-up contributions is a very bad deal!

SECURE 2.0 and Catch-Up Contributions

SECURE 2.0 disallows the tax deduction that people like Sarah rely on. It requires all catch-up contributions to be Roth contributions. For the affluent, this makes some sense. Why should someone with very substantial assets get a tax deduction when they already have a well-funded retirement?

Sadly, many Americans in their 50s and 60s do not have well-funded retirements. Removing the tax deduction for catch-up contributions increases their taxes. These are people who can least afford to shoulder a new tax. The goal should be to make it easier for those behind in retirement savings to catch-up. Taking away this tax deduction makes it more difficult to build up sufficient savings for retirement.

Fortunately, as of this writing SECURE 2.0 has only passed the House. It has not passed the Senate. Hopefully this provision will be reconsidered and will not ultimately become law.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

It appears some changes are likely coming to the tax-advantaged retirement savings landscape, as the House of Representatives passed (by a 414-5 vote) the Securing a Strong Retirement Act of 2022. It now goes the Senate where the Senate Finance Committee is likely to offer their own version of the bill. Commentators have referred to this bill as the SECURE Act 2.0 or SECURE 2.0.

This bill is not a paradigm shift in retirement saving and planning. Rather it makes many changes to the tax-advantaged retirement savings rules, most of which are small changes.

Here is a some brief points to consider:

My thinking about the bill

What expanding Roths (“Rothification”) means to the FI/FIRE community

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

The IRS and Treasury have recently issued two updates to the rules for payments which avoid the 10 percent early withdrawal penalty from retirement accounts. These payments are referred to as a series of substantially equal periodic payments, SEPP, or 72(t) payments. This post discusses the updated rules.

72(t) Payments

Tax advantaged retirement accounts are fantastic. Who doesn’t love 401(k)s, IRAs, Roth IRAs, and the like?

However, investing through a tax advantaged account can have drawbacks. One big drawback is that taxable amounts withdrawn from a tax advantaged retirement account prior to the account owner turning age 59 ½ are generally subject to a 10 percent early withdrawal penalty. My home state of California adds a 2.5 percent early withdrawal penalty.

There are some exceptions to this penalty. One of them is taking 72(t) payments. The idea is that if the taxpayer takes a “series of substantially equal periodic payments” they can avoid the penalty.

72(t) payments must be taken annually. Further, they must last for the longer of (a) 5 years or (b) the time until the taxpayer turns age 59 ½. This creates years of locked-in taxable income.

There are three methods that can be used to compute the amount of the annual 72(t) payments. These methods compute an annual distribution amount generally keyed off three numbers: the balance in the relevant retirement account, the interest rate, and the table factor provided by the IRS. The factor is greater the younger the account owner is. The greater the factor, the less the account owner can withdraw from a retirement account in a 72(t) payment.

New 72(t) Payment Interest Rates

In January 2022, the IRS and Treasury issued Notice 2022-6. Hat tip to Ed Zollars for the alert. This notice provides some new 72(t) rules. The biggest, and most welcome, change is a new rule for determining the interest rate.

Previously, the rule had been that 72(t) payments were keyed off 120 percent of the mid-term applicable federal rate (“AFR”). The IRS publishes this rate every month. In recent years, that has been somewhat problematic, as interest rates have been historically low. For example, in September 2020, the mid-term AFR was just 0.42 percent. This made relying on a 72(t) payment somewhat perilous. How much juice can be squeezed from a large retirement account if the interest rate is just 0.42 percent?

Here is what a $1M traditional IRA could produce, under the fixed amortization method, in terms of an annual payment for a 53 year old starting a 72(t) payment if the interest rate is just 0.42 percent:

120% of Sept 2020 MidTerm AFR

0.42%

Single Life Expectancy Years at Age 53

33.4

Account Balance

$1,000,000.00

Annual Payment

$32,151.93

Notice 2022-6 makes a very significant change. It now allows taxpayers to pick the greater of (i) up to 5 percent or (ii) up to 120 percent of mid-term AFR. That one change makes a 72(t) payment a much more attractive option, since periods of low interest rates do not as adversely affect the calculation.

Here is what a $1M traditional IRA could produce, under the fixed amortization method, in terms of an annual payment for a 53 year old starting a 72(t) payment if the interest rate is 5 percent:

5% Interest Rate

5.00%

Single Life Expectancy Years at Age 53

33.4

Account Balance

$1,000,000.00

Annual Payment

$62,189.80

The new rule provides a 5 percent interest rate floor for those using the fixed amortization method and the fixed annuitization method to compute a 72(t) payment. Using a 5 percent interest rate under the fixed amortization method is generally going to produce a greater payment amount than using the required minimum distribution method for 72(t) payments.

The interest rate change provides taxpayers with much more flexibility with 72(t) payments, and a greater ability to extract more money penalty free prior to age 59 ½. Taxpayers already have the ability to “right-size” the traditional IRA out of which to take a 72(t) payment to help the numbers work out. In recent years, what has been much less flexible has been the interest rate. Under these new rules, taxpayers always have the ability to select anywhere from just above 0% to 5% regardless of what 120 percent of mid-term AFR is.

Watch me discuss the update to 72(t) payment interest rates.

New Tables

A second new development is that the IRS and Treasury have issued new life expectancy tables for required minimum distributions (“RMDs”) and 72(t) payments. Most of the new tables are found at Treasury Regulation Section 1.401(a)(9)-9, though one new table is found at the end of Notice 2022-6.

These tables reflect increasing life expectancies. As a result, they reduce the amount of RMDs, as the factors used to compute RMDs are greater as life expectancy increases.

From a 72(t) payment perspective, this development is a minor taxpayer unfavorable development. Long life expectancies in the tables means the tables slightly reduce the amount of juice that can be squeezed out of any particular retirement account.

This said, the downside to 72(t) payments coming from increasing life expectancy on the tables is more than overcome by the ability to always use an interest rate of up to 5 percent. These two developments in total are a great net win for taxpayers looking to use 72(t) payments during retirement.

Use of 72(t) Payments

Traditionally, I have viewed 72(t) payments as a life raft rather than as a desirable planning tool for those retiring prior to their 59 ½th birthday. Particularly for those in the FI community, my view has been that it is better to spend down taxable assets and even dip into Roth basis rather than employ a 72(t) payment plan.

These developments shift my view a bit. Yes, I still view 72(t) payments as a life raft. Now it is an upgraded life raft with a small flatscreen TV and mini-fridge. 😉

As a practical matter, some will get to retirement prior to age 59 ½ with little in taxable and Roth accounts, and the vast majority of their financial wealth in traditional retirement accounts. Notice 2022-6 just made their situation much better and much more flexible. Getting to retirement at a time of very low interest rates does not necessarily hamstring their retirement plans given that they will always have at least a 5 percent interest rate to use in calculating their 72(t) payments.

72(t) Payments and Roth IRAs

As Roth accounts grow in value, there will be at least some thought of marrying Roth IRAs with 72(t) payments.

At least initially, Roth IRAs have no need for 72(t) payments. Those retired prior to age 59 ½ can withdraw previous Roth contributions and Roth conversions aged at least 5 years at any time tax and penalty free for any reason. So off the bat, no particular issue, as nonqualified distributions will start-off as being tax and penalty free.

Only after all Roth contributions have been withdrawn are Roth conversions withdrawn, and they are withdrawn first-in, first-out. Only after all Roth conversions are withdrawn does a taxpayer withdraw Roth earnings.

For most, the odds of withdrawing (i) Roth conversions that are less than five years old, and then (ii) Roth earnings prior to age 59 ½ are slim. But, there could some who love Roths so much they largely or entirely eschew traditional retirement account contributions. One could imagine an early retiree with only Roth IRAs.

Being “Roth only” prior to age 59 ½ could present problems if contributions and conversions at least 5 years old have been fully depleted. Taxpayers left with withdrawing conversions less than 5 years old or earnings in a nonqualified distribution might opt to establish a 72(t) payment plan for their Roth IRA. Such a 72(t) payment plan could avoid the 10 percent penalty on the withdrawn amounts attributable insufficiently aged conversions or Roth earnings. Note, however, that Roth earnings withdrawn in a nonqualified distribution are subject to ordinary income tax, regardless of whether they are part of a 72(t) payment plan.

See Treasury Regulation Section 1.408A-6 Q&A 5 providing that Roth IRA distributions can be subject to both the 72(t) early withdrawal penalty and the exceptions to the 72(t) penalty. The exceptions include a 72(t) payment plan.

Additional Resource

Ed Zollars has an excellent post on the updated IRS rules for 72(t) payments here.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters.Please also refer to the Disclaimer & Warning section found here.

Update as of December 20, 2021: I originally posted this article on Saturday morning, December 18th. On Sunday, developments occurred which called into question the use of a question mark in the article’s title.

Senator Joe Manchin appeared on Fox News Sunday and very publicly indicated he is a No on Build Back Better. He followed that with a written statement outlining his opposition to Build Back Better. The White House issued a statement in response to Senator Manchin.

A fair assessment indicates the parties are not at all close on this one. This is not a situation where Senator Manchin is bargaining to get A, B, and C into the bill and the White House is hoping to only have to give B and C. While anything is possible with tax legislation, it is quite difficult to argue that the Build Back Better program (which includes Backdoor Roth IRA repeal) has a realistic possibility of passage in this Congress in anything resembling its current form.

Update February 5, 2022: Watch my updated assessment of the lay of the land on 2022 Backdoor Roth IRAs.

Below is the original post posted on December 18, 2021.

There’s an early Christmas present for tax efficient investors. The proposal to end the Backdoor Roth IRA is on life support, and as of now (December 18, 2021) it appears that even if the proposal passes, it will not pass until 2022 at the earliest.

Latest Developments

The White House has now issued a written statement that the so-called Build Back Better program will not be signed into law this year. The proposal to repeal the Backdoor Roth IRA is one of many tax proposals contained within the overall Build Back Better legislative program. As this Deloitte write-up discusses, it is clear the Senate will not pass the legislation any time in the near-term. Thus, for the time being, the Backdoor Roth IRA is in the clear.

There is a reason the Build Back Better program will not be enacted during 2021: it’s not broadly popular. This is reflected in the current opposition of all 50 Senate Republicans and Democrat Senator Joe Manchin. Further, it is not at all clear that Democrat Senator Kyrsten Sinema will ultimately support Build Back Better.

If the Build Back Better program were to become popular, the dynamics in the U.S. Senate would likely change. But one must ask: is there something that could occur in early 2022 that would make the legislation popular then when it was not popular in late 2021?

Another issue the legislation has is the unlikelihood of any potential tax increase passing during an election year. New tax laws have proponents and opponents: in recent years Congress has hesitated to create opponents during election years by enacting significant tax legislation.

What If?

What if the legislation is enacted in early 2022? What happens to Backdoor Roth IRAs? That is highly, highly speculative. My guess is that if the legislation (at that point) bans Backdoor Roth IRAs, either (i) Backdoor Roth IRAs will be prohibited as of January 1, 2023 (instead of January 1, 2022 in the current legislation) or (ii) prohibited as of the enactment of the law.

But all sorts of alternative possibilities exist. A much smaller version of the Build Back Better program could be enacted, and that version could omit the Backdoor Roth IRA repeal. Or there will be no legislation enacted at all.

Why Are We Here?

Is the Backdoor Roth IRA gimmicky? Absolutely it is!

But there is a bigger issue. Why the heck is there any income limitation on the ability to make a $6,000 annual contribution to a Roth IRA? Consider these two examples.

Wealthy Investor controls a large public company and is known for his ability to earn good investment returns. He is worth billions of dollars and is 80 years old. He can direct the large public company to offer a Roth 401(k), and on January 1st of 2022 he can have payroll issued to him, of which he can put $27,000 into his Roth 401(k).

Single Nurse, age 35, is a nurse and earns $170,000 from her W-2 job. Her employer offers a traditional 401(k) but no Roth 401(k). Single Nurse earns too much (due to the Roth IRA modified adjusted gross income limit) to make an annual $6,000 contribution to a Roth IRA. As a result, Single Nurse’s annual Roth contributions are limited to $0.

Wealthy Investor can contribute $27,000 to a Roth 401(k) but Single Nurse can’t contribute $6,000 to a Roth IRA?

To borrow an exasperated quote from Cosmo Kramer, “What’s going on!!!”

The Backdoor Roth IRA solves this problem for Single Nurse and many other Americans. This workaround does not work for all Americans, as I have previously written.

The simplest solution is to eliminate the modified adjusted gross income limit for all Roth IRA contributions. So some very wealthy Americans will get a few thousand dollars into Roth IRAs every year. Is this a horribly worrisome outcome considering many very wealthy Americans already have access to much greater workplace retirement plan contributions with absolutely no income limitation?

Once the income limit on the ability to make a Roth IRA contribution is repealed, there will be no need for Backdoor Roth IRAs.

Conclusion

The only constant in the tax world is change. We shall see what the future holds for the Backdoor Roth IRA, but the coast appears to be clear for the rest of the year. Stay tuned!

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters.Please also refer to the Disclaimer & Warning section found here.

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters.Please also refer to the Disclaimer & Warning section found here.

In recent years, inflation existed but was not significant. Significant inflation was associated with wide lapels and eight-track tapes and thought to be left behind in the late 1970s and early 1980s.

Inflation has a tax angle. How does one use tax planning to minimize the impact of inflation? In this post, I review the issues associated with inflation and tactics to consider if one is concerned about inflation.

Inflation: The Tax Problem

Inflation increases the nominal (i.e., stated) value of assets without a corresponding increase in the real value of the asset. Here is an example:

Larry buys $100,000 worth of XYZ Mutual Fund on January 1, 2022. During the year 2022, there is 10 percent inflation. On January 1, 2023, the XYZ Mutual Fund is worth $110,000. Inflation-adjusted, the position has the same real value as it did when Larry purchased it. However, were Larry to sell the entire position, he would trigger a $10,000 capital gain ($110,000 sales price less $100,000 tax basis), which would be taxable to him.

Hopefully you see the problem: Larry has not experienced a real increase in wealth. Larry’s taxable “gain” is not a gain. Rather, it is simply inflation! Larry will pay tax on inflation if he sells the asset. Ouch!

While inflation increases the nominal value of assets, there is no inflation adjustment to tax basis! Thus, inflation creates artificial gains subject to income tax.

There are other tax problems with inflation. Inflation artificially increases amounts received as wages, self-employment income, interest, dividends, and retirement plan distributions. Those artificial increases are not real increases in income (as they do not represent increases in value) but they are subject to income tax as though they were real increases in income.

The tax law does provide some remedy to address the problem of taxing inflation. The IRS provides inflation adjustments to increase the size of progressive tax brackets. In addition, the standard deduction is adjusted annually for inflation. Recently the IRS released the inflation adjustments for 2022.

IRS inflation adjustments are helpful, but they do not excuse inflation from taxation. Rather, they only soften the blow. Thus, they are not a full cure for the tax problems caused by inflation.

Inflation and Traditional Retirement Accounts

Inflation is detrimental to traditional retirement accounts such as pre-tax 401(k)s and IRAs. Holding assets inside a traditional retirement account subjects the taxpayer to income tax on the growth in the assets caused by inflation.

Inflation artificially increases amounts in these accounts that will ultimately be subject to taxation. Inflation can also limit the opportunity to do Roth conversions in early retirement. Greater balances to convert from traditional to Roth accounts and increased dividend, capital gain, and interest income triggered by inflation makes early retiree Roth conversion planning more challenging.

Inflation and Real Estate

There are several tax benefits of rental real estate. One of the main benefits is depreciation. For residential real estate, the depreciable basis is deducted in a straight-line over 27.5 years. For example, if the depreciable basis of a rental condo is $275,000, the annual depreciation tax deduction (for 27.5 years) is $10,000 (computed as $275,000 divided by 27.5). That number rarely changes, as most of the depreciable basis is determined at the time the property is purchased or constructed.

Over time, inflation erodes the value of depreciation deductions. Inflation generally increases rental income, but the depreciation deduction stays flat nominally and decreases in real value. Increasing inflation reduces the tax benefits provided by rental real estate.

Planning Techniques

There are planning techniques that can protect taxpayers against the tax threat posed by inflation.

Roth Contributions and Conversions

Inflation is yet another tax villain the Roth can slay. Tax free growth inside a Roth account avoids the tax on inflation.

Once inside a Roth, concerns about inflation increasing taxes generally vanish. Properly planned, Roths provide tax free growth and tax free withdrawals. Thus, Roths effectively eliminate the concern about paying tax on inflation.

For those thinking of Roth conversions, inflation concerns point to accelerating Roth conversions. The sooner amounts inside traditional retirement accounts are converted to Roth accounts, the less exposure the amounts have to inflation taxes.

Roth contributions and conversions provide tax insurance against the threat of inflation. For those very concerned about inflation, this consideration moves the needle toward the Roth in the ongoing Roth versus traditional debate.

Watch me discuss using Roth accounts to help manage an investor’s exposure to inflation.

Health Savings Accounts

A Health Savings Account, like its Roth IRA cousin, offers tax free growth. HSAs also protect against taxes on inflation. Inflation is another argument to take advantage of an HSA.

Basis Step Up Planning

There is another tax planning opportunity that can wipe away the taxes owed on years of inflation: the basis step up at death. At death, heirs receive a basis in inherited taxable assets which is usually the fair market value of the assets on the date of death. For taxable assets, death provides an opportunity to escape the tax on inflation.

It is important to note that traditional retirement accounts do not receive a basis step up. Inflation inside a traditional retirement account will eventually be subject to tax (either to the original owner or to a beneficiary after the original owner’s death).

During one’s lifetime, there is the tax gain harvesting opportunity to step up basis and reduce inflation taxes. The tactic is to sell and repurchase an investment with a built-in gain at a time when the investor does not pay federal income tax on the capital gain. If one can keep their marginal federal income tax rate in the 12% or lower marginal tax bracket, they can pay a 0% federal income tax rate on the gain and “reset” the basis to the repurchase price of the sold and then repurchased asset.

There is a second flavor of tax gain harvesting: triggering a capital gain (at an advantageous time from a tax perspective) by selling an asset and reinvesting the proceeds in a more desirable asset (essentially, investment reallocation).

One inflation consideration with respect to tax gain harvesting: as inflation increases interest and dividends, there will be less room inside the 12 percent taxable income bracket to create capital gains that are federal income tax free.

Conclusion

Inflation is yet another tax planning consideration. As we are now in a period of significant inflation, taxpayers and advisors will need to weigh inflation’s potential impact on tax strategies.

None of the above is advice for any particular taxpayer. Hopefully it provides some educational background to help assess the tax impact of inflation and consider tactical responses to inflation.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

Listen to me discuss year-end tax planning with Brad and Jonathan on the ChooseFI podcast. The episode is available on all major podcast players, YouTube, and on the ChooseFI website (https://www.choosefi.com/year-end-tax-planning-2021-ep-351/).

During the conversation we referenced this blog post.

As always, the discussion is general and educational in nature and does not constitute tax, investment, legal, or financial advice with respect to any particular individual or taxpayer. Please consult your own advisors regarding your own unique situation. Sean Mullaney and ChooseFI Publishing are currently under contract to publish a book authored by Sean Mullaney.

FI Tax Guy can be your financial advisor! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters.Please also refer to the Disclaimer & Warning section found here.

Many taxpayers ask the question: should I contribute to a Roth 401(k) or contribute to a Roth IRA? While there is no universal answer to this question, for many in the financial independence (FI/FIRE) community, I believe there is a clear answer.

Roth Accounts

What is not to love about Roths? If withdrawn properly, they promise tax free growth and tax free withdrawals. Further, Roths (be them 401(k)s or IRAs) give taxpayers tax insurance: income tax increases in the future are not a problem with respect to money invested in a Roth account. Roths even provide some ancillary benefits during retirement if the United States ever adopts a value added tax (a “VAT”).

Roth IRAs

Roth IRAs are an individual account and can be established at a plethora of financial institutions. Most working taxpayers qualify to make annual contributions to a Roth IRA. However, the ability to make an annual contribution to a Roth IRA phases out at certain income levels and is completely eliminated at $140,000 (single) or $208,000 (married filing joint) of modified adjusted gross income (2021 numbers).

The maximum annual contribution to a Roth IRA is $6,000 (if under age 50) or $7,000 (if age 50 or older) (2021 and 2022 numbers).

I have previously written about my fondness for Roth IRAs. One reason for my fondness is that annual contributions can be withdrawn from the Roth IRA at any time for any reason tax and penalty free. Thus, Roth IRAs can perform double duty as both a retirement savings vehicle and as an emergency fund. This is an advantage of Roth IRAs over Roth 401(k)s.

Of course, considering their tax free growth, it is usually best to keep amounts in a Roth IRA for as long as possible.

Roth 401(k)s

Roth 401(k)s are a workplace retirement plan. Contributions can be made through payroll withholding. Many employers offer a Roth 401(k), though they are far from universally adopted.

The Roth 401(k) does enjoy some advantages when compared to its Roth IRA cousin. First, there is no income limit to worry about. Regardless of income level, an employee can contribute to a Roth 401(k). Second, the contribution limits are much higher than the contribution limits for Roth IRAs. As of 2021, the annual Roth 401(k) contribution limit is $19,500 (under age 50) or $26,000 (age 50 and older).

So which one should members of the FI/FIRE community prioritize? Contributions to a Roth 401(k) or contributions to a Roth IRA?

To help us answer that question, let’s consider a young couple pursuing financial independence:

Stephen and Becky are both age 30, married (to each other), and pursuing financial independence. They both would like to retire at least somewhat early by conventional standards. They each have a W-2 salary of $90,000. They have approximately $2,000 of annual interest and dividend income. They claim the standard deduction. At this level of income, they have a 22 percent marginal federal income tax rate. Stephen and Becky each have access to a traditional 401(k) and a Roth 401(k) at work. They would like to maximize their retirement plan contributions.

How should Stephen and Becky allocate their retirement plan contributions? Should they contribute to a Roth 401(k) and/or to a Roth IRA?

To my mind, the best play here is to contribute to a Roth IRA ($6,000 each) and contribute to a traditional 401(k) ($19,500 each). Stephen and Becky should not contribute to a Roth 401(k).

There is a significant tax opportunity cost to making a Roth 401(k) contribution: the ability to deduct a traditional contribution to a 401(k). Remember, the Roth 401(k) shares the $19,500 annual contribution limit with the traditional 401(k). Every dollar contributed to a Roth 401(k) is a dollar that cannot be contributed to a traditional 401(k).

For Stephen and Becky, the hope is that in early retirement tax laws either stay the same as they are today or at least keep today’s flavor. The idea is to take a deduction while working at a 22 percent marginal tax rate (by contributing to the traditional deductible 401(k)). Then, in early retirement, they convert amounts in the traditional 401(k) to a Roth. At that point, hopefully they have a marginal federal income tax rate of 10 percent or 12 percent. Many early retirees have an artificially low taxable income (and thus, a low marginal income tax rate) prior to collecting Social Security.

Contrast the significant tax opportunity cost of making a Roth 401(k) contribution to the tax opportunity cost of making a Roth IRA contribution: practically nothing.

Stephen and Becky have no ability to deduct a traditional IRA contribution because of their income level and the fact that they are covered by a workplace retirement plan. Thus, they aren’t losing much, from a tax perspective, by each making a $6,000 annual Roth IRA contribution.

Situations Where the Roth 401(k) Contributions Make Sense

For those in the financial independence community, generally there are four situations where choosing to contribute to a Roth 401(k) makes sense. In three of these situations, the tax rate arbitrage play available to Stephen and Becky isn’t available. In the fourth situation (tax insurance), there is a separate consideration causing the taxpayer to forgo an initial tax deduction to get assurance as to the tax rate they will be subject to.

In the situations below, a Roth 401(k) contribution is likely preferable to a traditional 401(k) contribution. As compared to a Roth IRA contribution, (a) the first contributions should generally be to the Roth 401(k) to secure the employer match, and then after that, (b) generally both the Roth 401(k) and the Roth IRA work well. To my mind, the emergency-type fund feature of the Roth IRA, which I’ve previously discussed, is probably the tiebreaker in favor of making the next contributions to a Roth IRA.

Transition Years

Think about a year one graduates college, graduate school, law school, or medical school. Usually, the person works for only the last half or last quarter of the year. Thus, they have an artificially low taxable income (since they only work for a small portion of the year). Why take a tax deduction for a contribution to a traditional 401(k) in such a year, when one’s marginal federal income tax rate might only be 10 percent or 12 percent?

Transition years are a great time to make Roth 401(k) contributions instead of traditional 401(k) contributions.

Young Earners with Low Incomes

Many careers start with modest salaries early but have the potential to experience significant salary increases over time. My previous career in public accounting is one example. Medicine is another example. Young accountants and doctors, among others, making modest starting salaries should consider Roth 401(k) contributions at the beginning of their careers. As their salaries increase, they should consider shifting their contributions to a traditional 401(k).

As a *very general* rule of thumb, those in the 10 percent or 12 percent marginal federal income tax rate (particularly those not subject to a state income tax) should consider prioritizing Roth 401(k) contributions (regardless of occupation).

No Hope

Picture a charismatic franchise NFL quarterback. He’s got a $40M plus annual NFL contact, endorsement deals, business ventures, and likely a long TV career after his playing days are done. For him, there is no hope ( 😉 ). He will probably be in the top federal income tax bracket the rest of his life. He might be well advised to “lock-in” today’s low (by historical standards) 37% federal income tax marginal tax rate by choosing to contribute to a Roth 401(k) instead of to a traditional 401(k).

Tax Insurance

We really do not know what the future holds. That includes future federal and state income tax rates.

Thus, some workers may want to buy tax insurance. Roth 401(k) contributions are a way to do that. The extra tax paid (because the taxpayer did not deduct traditional 401(k) contributions) is an insurance premium. That insurance premium ensures that the taxpayer won’t be subject to future income tax (including potential tax rate increases) on amounts inside the Roth 401(k) and the growth thereon.

Remember, none of this is “all or nothing” planning. Some may want to allocate a piece of their workplace retirement plan contributions to the Roth 401(k) to get some insurance coverage against future tax rate increases.

Conclusion

In the FI community, a maxed out traditional 401(k) and a maxed out Roth IRA (whether through a regular annual contribution or through a Backdoor Roth IRA) can be the dynamic duo of retirement savings. This combination can provide tax flexibility while maximizing current tax deductions. Roth 401(k) contributions often have a significantly greater tax opportunity cost as compared to the tax opportunity cost of Roth IRA contributions. In such situations, the Roth IRA is preferable to my mind.

Of course, each individual is unique and has different financial and tax goals and priorities. The above isn’t advice for any particular individual, but hopefully provides some educational insight regarding the issues to consider when allocating employee retirement account contributions.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters.Please also refer to the Disclaimer & Warning section found here.

New Year’s Eve is an important day if you do a Backdoor Roth IRA. Read below to find out why.

The Backdoor Roth IRA

I’ve written before about the Backdoor Roth IRA. It is a two step process whereby those not qualifying for a regular Roth IRA contribution can qualify to get money into a Roth IRA. Done over several years, it can help taxpayers grow significant amounts of tax free wealth.

One of the best aspects of the Backdoor Roth IRA is that it does not forego a tax deduction. Most taxpayers ineligible to make a regular Roth IRA contribution are also ineligible to make a deductible traditional IRA contribution. In the vast majority of cases, the choice is between investing money in a taxable account versus investing in a Roth account. For most, a Roth is preferable, since Roths do not attract income taxes on the interest, dividends, and capital gains investments generate.

The Basic Backdoor Roth IRA and the Form 8606

Let’s start with a fairly basic example.

Example 1

Betsy, age 40, earns $300,000 from her W-2 job in 2021, is covered by a workplace 401(k) plan, and has some investment income. Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

At this level of income, Betsy does not qualify for a regular Roth IRA contribution, and she does not qualify to deduct a traditional IRA contribution.

Betsy contributes $6,000 to a traditional IRA on May 20, 2021. The contribution is nondeductible. Because the contribution is nondeductible, Betsy gets a $6,000 basis in her traditional IRA. Betsy must file a Form 8606 with her 2021 tax return to report the nondeductible contribution.

On June 5, 2021, Betsy converts the entire balance in the traditional IRA, $6,003, to a Roth IRA. As of December 31, 2021, Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

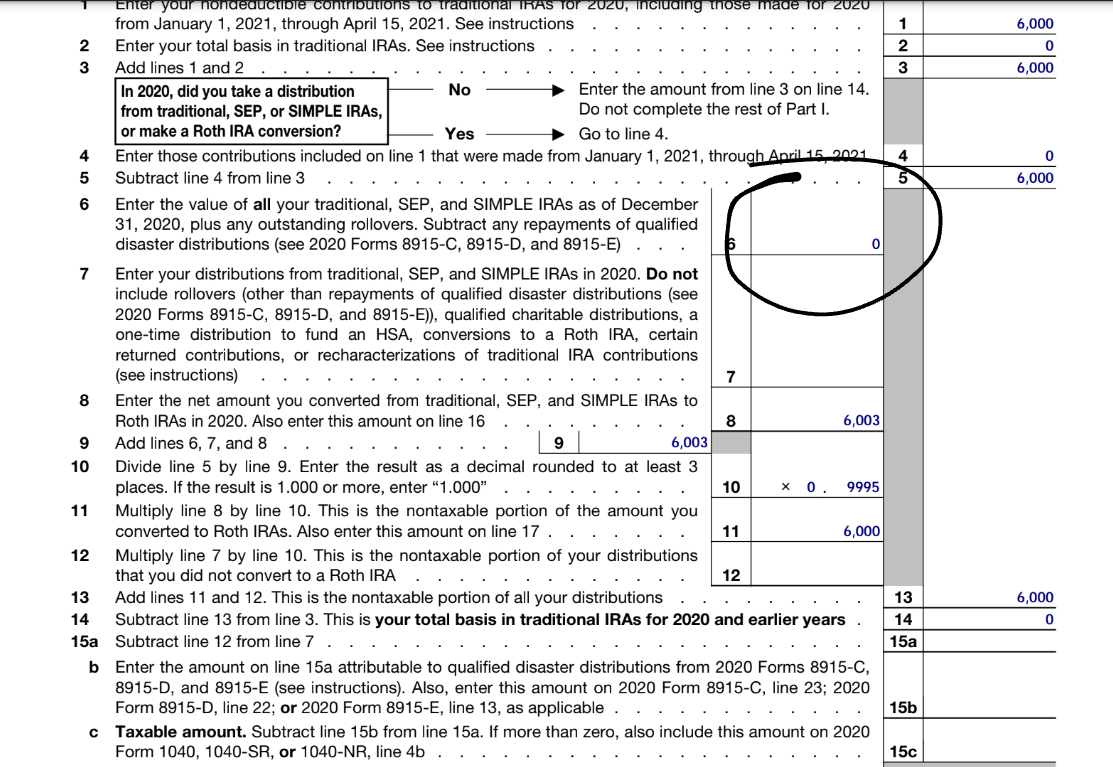

Betsy has successfully executed a Backdoor Roth IRA. Here is what page 1 of the Form 8606 Betsy should file with her 2021 income tax return should look like.

Notice here that I am using the 2020 version of the Form 8606 for this and all examples. The 2021 Form 8606 is not yet available as of this writing.

The most important line of page 1 of the Form 8606 is line 6. Line 6 reports the fair market value of all traditional IRAs, SEP IRAs, and SIMPLE IRAs Betsy owns as of year-end. Because Betsy had no traditional IRAs, SEP IRAs, and SIMPLE IRAs as of December 31, 2021, her Backdoor Roth IRA works and is tax efficient. This important number ($0) on line 6 of the Form 8606 is what ensures Betsy’s Backdoor Roth IRA is tax efficient.

Note that Betsy’s Backdoor Roth IRA creates an innocuous $3 of taxable income, which is reported on the top of part 2 of the Form 8606.

The Pro-Rata Rule and December 31st

But what if Betsy did have a balance inside a traditional IRA, SEP IRA, or SIMPLE IRA on December 31, 2021? Would her Backdoor Roth IRA still be tax efficient? Probably not, due to the Pro-Rata Rule.

The Pro-Rata Rule tells us just how much of the basis in her traditional IRA Betsy can recover when she does the Roth conversion step of the Backdoor Roth IRA. Betsy’s $6,000 nondeductible traditional IRA creates $6,000 of basis. As we saw above, Betsy was able to recover 100 percent of her $6,000 of basis against her Roth conversion.

But the Pro-Rata Rule says “not so fast” if Betsy has another traditional IRA, SEP IRA, or SIMPLE IRA on December 31st of the year of any Roth conversion. The Pro-Rata Rule allocates IRA Basis between converted amounts (in Betsy’s case, $6,003) and amounts in traditional IRAs, SEP IRAs, and SIMPLE IRAs on December 31st. Here’s an example.

Example 2

Betsy, age 40, earns $300,000 from her W-2 job in 2021, is covered by a workplace 401(k) plan, and has some investment income. Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

Betsy contributes $6,000 to a traditional IRA on May 20, 2021. The contribution is nondeductible. Because the contribution is nondeductible, Betsy gets a $6,000 basis in her traditional IRA. Betsy must file a Form 8606 with her 2021 tax return to report the nondeductible contribution.

On June 5, 2021, Betsy converts the entire balance in the traditional IRA, $6,003, to a Roth IRA.

On September 1, 2021, Betsy transfers an old 401(k) from a previous employer 401(k) plan to a traditional IRA. On December 31st, that traditional IRA is worth $100,000. The old 401(k) had no after-tax contributions.

This one 401(k)-to-IRA rollover transaction dramatically changes both the taxation of Betsy’s Backdoor Roth IRA and her 2021 Form 8606. Here’s page 1 of the Form 8606.

Line 6 of the Form 8606 now has $100,000 on it instead of $0. That $100,000 causes Betsy to recover only 5.67 percent of the $6,000 of basis she created by making a nondeductible contribution to the traditional IRA. As a result, $5,663 of the $6,003 transferred to the Roth IRA in the Roth conversion step is taxable to Betsy as ordinary income. At a 35% tax rate, the 401(k) to IRA rollover (a nontaxable transaction) cost Betsy $1,982 in federal income tax on her Backdoor Roth IRA. Ouch!

Quick Lesson: The lesson here is that prior to rolling over a 401(k) or other workplace plan to an IRA, taxpayers should consider the impact on any Backdoor Roth IRA planning already done and/or planned for the future. One possible planning alternative is to transfer old employer 401(k) accounts to current employer 401(k) plans.

There is an antidote to the Pro-Rata Rule when one has amounts in traditional IRAs, SEP IRAs, and SIMPLE IRAs. It is transferring the traditional IRA, SEP IRA, or SIMPLE IRA to a qualified plan (such as a 401(k) plan) before December 31st. Here is what that might look like in Betsy’s example.

Example 3

Betsy, age 40, earns $300,000 from her W-2 job in 2021, is covered by a workplace 401(k) plan, and has some investment income. Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

Betsy contributes $6,000 to a traditional IRA on May 20, 2021. The contribution is nondeductible. Because the contribution is nondeductible, Betsy gets a $6,000 basis in her traditional IRA. Betsy must file a Form 8606 with her 2021 tax return to report the nondeductible contribution.

On June 5, 2021, Betsy converts the entire balance in the traditional IRA, $6,003, to a Roth IRA.

On September 1, 2021, Betsy transfers an old 401(k) from a previous employer to a traditional IRA. The old 401(k) had no after-tax contributions.

On November 16, 2021, Betsy transfers the entire balance in this new traditional IRA to her current employer’s 401(k) plan in a direct trustee-to-trustee transfer.

Here is Betsy’s 2021 Form 8606 (page 1) after all of these events:

Betsy got clean by December 31st, so her Backdoor Roth IRA now reverts to the optimized result (just $3 of taxable income) she obtained in Example 1.

Pro-Rata Rule Clean Up

Implementation

From a planning perspective, it is best to clean up old traditional IRAs/SEP IRAs/SIMPLE IRAs prior to, not after, executing the Roth conversion step of a Backdoor Roth IRA. I say that because things happen in life. There is absolutely no guarantee that those intending to roll amounts from IRAs to workplace qualified plans will get that accomplished by December 31st.

Further, transfers from one retirement account to another are usually best done through a direct “trustee-to-trustee” transfer to minimize the risk that the money in the retirement account accidentally is distributed to the individual, causing potential tax and penalties.

Before cleaning up old traditional IRAs, SEP IRAs, and SIMPLE IRAs, one should consider the investment choices and fees inside their employer retirement plan (such as a 401(k)). If the investment options are not good, and/or the fees are high, perhaps cleaning up an IRA to move money into less desirable investments is not worth it. This is a subjective judgment that must weigh the potential tax and investment benefits and drawbacks.

Tax Issues

Amazingly enough, the Pro-Rata Rule is concerned with only one day: December 31st. A taxpayer can have a balance in a traditional IRA, SEP IRA, or SIMPLE IRA on any day other than December 31st, and it does not count for purposes of the Pro-Rata Rule. Perhaps December 31st should be called Pro-Rata Rule Day instead of New Year’s Eve. 😉

Extra care should be taken when cleaning up (a) large amounts in any type of IRA and (b) any SIMPLE IRA. While it is fairly obvious that significant sums should be moved only after considering all the relevant investment, tax, and execution issues, the SIMPLE IRA provides its own nuances. Any SIMPLE IRA cannot be rolled to an account other than a SIMPLE IRA within the SIMPLE IRA’s first two years of existence. Thus, SIMPLE IRAs must be appropriately aged before doing any sort of Backdoor Roth IRA clean up planning.

Spouses are entirely separate for Pro-Rata Rule purposes, even in community property states. Cleaning up one spouse, or failing to clean up one spouse, has absolutely no impact on the taxation of the other spouse’s Backdoor Roth IRA.

Lastly, non spousal inherited IRAs do not factor into a taxpayer’s application of the Pro-Rata Rule. Each non spousal inherited IRA has its own separate, hermetically sealed Pro-Rata Rule calculation. The inheriting beneficiary does a Pro-Rata Rule calculation on all IRAs he/she owns as the original owner, separate from any inherited IRAs. In addition, non spousal inherited IRAs cannot be rolled into a 401(k).

Mega Backdoor Roth

Good news: the concerns addressed in this blog post generally do not apply with respect to the Mega Backdoor Roth (sometimes referred to as a Mega Backdoor Roth IRA, though a Roth IRA does not necessarily have to be involved). Qualified plans such as 401(k)s are not subject to the Pro-Rata Rule.

While 401(k)s are not subject to the Pro-Rata Rule, amounts within a particular 401(k) plan’s after-tax 401(k) are subject to the “cream-in-the-coffee” rule I previously wrote about here. Thus, if there is growth on Mega Backdoor Roth contributions before they are moved out of the after-tax 401(k), generally speaking either the taxpayer must pay income tax on the growth (if moved to a Roth account) or the taxpayer can separately roll the growth to a traditional IRA (which could then create a rather small Pro-Rata Rule issue with future Backdoor Roth IRAs). Fortunately, the cream-in-the-coffee rule has a much narrower reach than the Pro-Rata Rule.

Backdoor Roth IRA Tax Return Reporting

Watch me discuss Backdoor Roth IRA tax return reporting.

Conclusion

Get your IRAs in order so you can enjoy New Year’s Eve!

December 31st is an important date when it comes to Backdoor Roth IRA planning. It is important to plan to have no (or at a minimum, very small) balances in traditional IRAs, SEP IRAs, and SIMPLE IRAs on December 31st when planning Backdoor Roth IRAs.

None of what is discussed in this blog post is advice for any particular taxpayer. Those working through Backdoor Roth IRA planning issues are often well advised to reach out to professional advisors regarding their own tax situation.

Further Reading

I did a blog post about Backdoor Roth IRA tax return reporting here.

I did a deep dive on the taxation of Roth IRA withdrawals here.

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.