It’s time to think about year-end tax planning. Year-end is a great time to get tax planning ducks in a row and take advantage of opportunities. This is particularly true for those in the financial independence community. FI principles often increase one’s tax planning opportunities.

Remember, this post is for educational purposes only. None of it is advice directed towards any particular taxpayer.

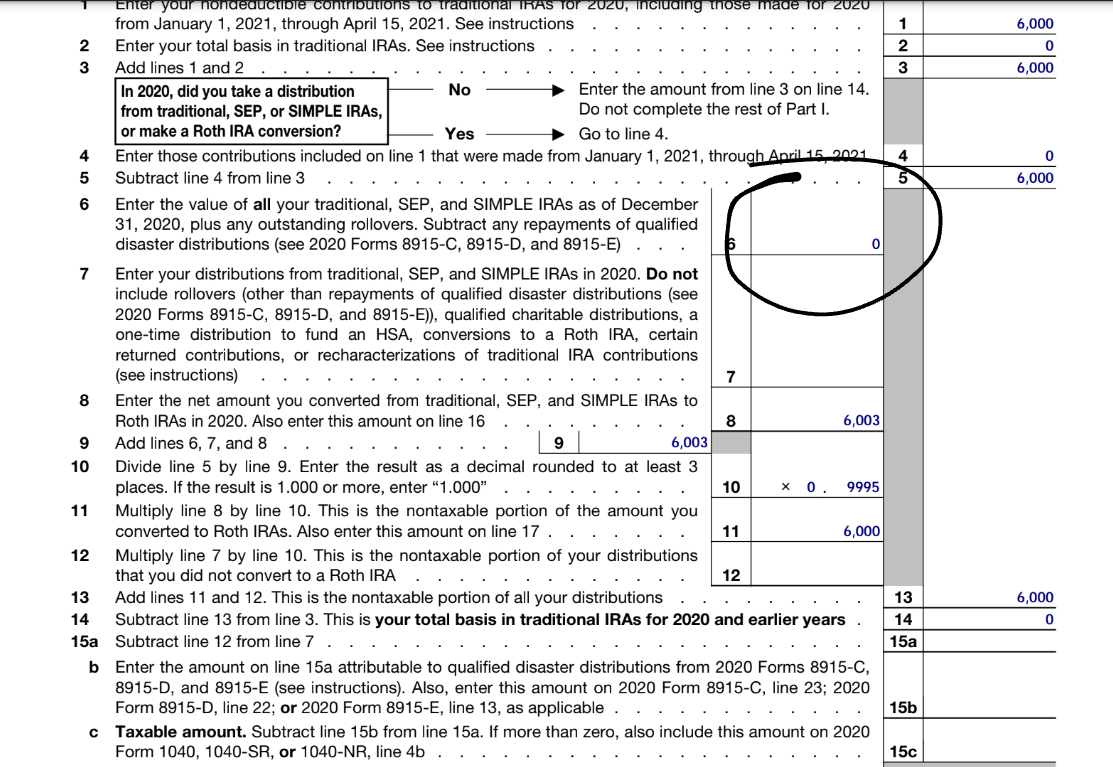

Backdoor Roth IRA Deadline 2021

As of now (December 7, 2021), the legal deadlines around Backdoor Roth IRAs have not changed: the nondeductible 2021 traditional IRA contribution must happen by April 18, 2022 and there is no legal deadline for the second step, the Roth conversion. However, from a planning perspective, the practical deadline to have both steps of a 2021 Backdoor Roth IRA completed is December 31, 2021.

This is because of proposed legislation that eliminates the ability to convert nondeductible amounts in a traditional IRA effective January 1, 2022. As of December 7th, the proposed legislation has passed the House of Representatives but faces a very certain future in the Senate. Considering the risk that the Backdoor Roth elimination proposal is enacted, taxpayers planning on completing a 2021 Backdoor Roth IRA should act to ensure that the second step of the Backdoor Roth IRA (the Roth conversion) is completed before December 31st.

Taxpayers on the Roth IRA MAGI Limit Borderline

In years prior to 2021, taxpayers unsure of whether their income would allow them to make a regular Roth IRA contribution could simply wait until tax return season to make the determination. At that point, they could either make the regular Roth IRA contribution for the prior year (if they qualified) or execute what I call a Split-Year Backdoor Roth IRA.

With the proposed legislation looming, waiting is not a good option. The good news is that taxpayers executing a Backdoor Roth IRA during a year they actually qualify for a regular annual Roth IRA contribution suffer no material adverse tax consequences. Of course, in order for this to be true there must be zero balance, or at most a very small balance, in all traditional IRAs, SEP IRAs, and SIMPLE IRAs as of December 31, 2021.

December 31st and Backdoor Roth IRAs

December 31st is a crucial date for those doing the Roth conversion step of a Backdoor Roth IRA during the year. It is the deadline to move any balances in traditional IRAs, SEP IRAs, and SIMPLE IRAs to workplace plans in order to ensure that the Roth conversion step of any Backdoor Roth IRA executed during the year is tax-efficient.

This December 31st deadline applies regardless of the proposed legislation discussed above.

IRAs and HSAs

Good news on regular traditional IRA contributions, Roth IRA contributions, and HSA contributions: they don’t have to be part of an end-of-2021 tax two-minute drill. The deadline for funding an HSA, a traditional IRA, and a Roth IRA for 2021 is April 18, 2022.

Solo 401(k)

The self-employed should consider this one. Deadlines vary, but as a general rule, those eligible for a Solo 401(k) usually benefit from establishing one prior to year-end. The big takeaway should be this: if you are self-employed, your deadline to seriously consider a Solo 401(k) for 2021 is ASAP! Usually, such considerations benefit from professional assistance.

Something to look forward to in 2022: my upcoming Solo 401(k) book!

Charitable Contributions

For those itemizing deductions in 2021 and either not itemizing in 2022 or in a lower marginal tax rate in 2022 than in 2021, it can be advantageous to accelerate charitable contributions late in the year. It can be as simple as a direct donation to a qualifying charity by December 31st. Or it could involve contributing to a donor advised fund by December 31st.

A great donor advised fund planning technique is transferring appreciated securities (stocks, bonds, mutual funds, or ETFs) to a donor advised fund. Many donor advised fund providers accept securities. The tax benefits of making such a transfer usually include (a) eliminating the built-in capital gain from federal income taxation and (b) if you itemize, getting to take a current year deduction for the fair market value of the appreciated securities transferred to the donor advised fund.

The elimination of the lurking capital gain makes appreciated securities a better asset to give to a donor advised fund than cash (from a tax perspective). Transfers of appreciated securities to 501(c)(3) charities can also have the same benefits.

The 2021 deadline for this sort of planning is December 31, 2021, though taxpayers may need to act much sooner to ensure the transfer occurs on time. This is particularly true if the securities are transferred from one financial institution to a donor advised fund at another financial institution. In these cases, the transfer may have to occur no later than mid-November, though deadlines will vary.

Early Retirement Tax Planning

For those in early retirement, the fourth quarter of the year is the time to do tax planning. Failing to do so can leave a great opportunity on the table.

Prior to taking Social Security, many early retirees have artificially low taxable income. Their only taxable income usually consists of interest, dividends, and capital gains. In today’s low-yield environment, without additional planning, early retirees’ taxable income can be very low (perhaps even below the standard deduction).

Artificially low income gives early retirees runway to fill up lower tax brackets (think the 10 percent and 12 percent federal income tax brackets) with taxable income. Why pay more tax? The reason is simple: choose to pay tax when it is taxed at a low rate rather than defer it to a future when it might be taxable at a higher rate.

The two main levers in this regard are Roth conversions and tax gain harvesting. Roth conversions move amounts in traditional retirement accounts to Roth accounts via a taxable conversion. The idea is to pay tax at a very low tax rate while taxable income is artificially low, rather than leaving the money in deferred accounts to be taxed later in retirement at a higher rate under the required minimum distribution (“RMD”) rules.

Tax gain harvesting is selling appreciated assets when one is in the 10 percent or 12 percent marginal tax bracket so as to incur a zero percent long term capital gains federal tax rate on the capital gain.

Early retirees can do some of both. In terms of a tiebreaker, if everything else is equal, I prefer Roth conversions to tax gain harvesting, for two primary reasons. First, traditional retirement accounts are subject to ordinary income tax rates in the future, which are likely to be higher than preferred capital gains tax rates. Second, large taxable capital gains in taxable accounts can be washed away through the step-up in basis at death. The step-up in basis at death doesn’t exist for traditional retirement accounts.

One time to favor tax gain harvesting over Roth conversions is when the traditional retirement accounts have the early retiree’s desired investment assets but the taxable brokerage account has positions that the early retiree does not like anymore (for example, a concentrated position in a single stock). Why not take advantage of tax gain harvesting to reallocate into preferred investments in a tax-efficient way?

Long story short: during the fourth quarter, early retirees should consider their taxable income for the year and consider year-end Roth conversions and/or tax gain harvesting. Planning in this regard should be executed no later than December 31st, and likely earlier to ensure proper execution.

Roth Conversions, Tax Gain Harvesting, and Tax Loss Harvesting

Early retired or not, the deadline for 2021 Roth conversions, tax gain harvesting, and tax loss harvesting is December 31, 2021. Taxpayers should always consider timely implementation: these are not tactics best implemented on December 30th!

For some who find their income dipped significantly in 2021 (perhaps due to a job loss), 2021 might be the year to convert some amounts in traditional retirement accounts to Roth retirement accounts. Some who are self-employed might want to consider end-of-year Roth conversions to maximize their qualified business income deduction.

Stimulus and Child Tax Credit Planning

Taxpayers who did not receive their full 2021 stimulus may want to look into ways to reduce their 2021 adjusted gross income so as to qualify for additional stimulus funds. I wrote in detail about one such opportunity in an earlier blog post. Lowering adjusted gross income can also qualify taxpayers for additional child tax credits.

There are many factors you and your advisor should consider in tax planning. This opportunity may be one of them. For example, taxpayers considering a Roth conversion at the end of the 2021 might want to hold off in order to qualify for additional stimulus and/or child tax credits.

Accelerate Payments

The self-employed and other small business owners may want to review business expenses and pay off expenses before January 1st, especially if they anticipate their marginal tax rate will decrease in 2022. Depending on structure and accounting method, doing so may not only reduce income taxes, it could also reduce self-employment taxes.

State Tax Planning

For my fellow Californians, the big one here is property taxes. It may be advantageous to pay billed (but not yet due) property taxes in late 2021. This allows taxpayers to deduct the amount on their 2021 California income tax return. In California, the standard deduction ($4,601 for single taxpayers, $9,202 for married filing joint taxpayers) is much lower than the federal standard deduction, so consideration should be given to accelerating itemized deductions in California, regardless of whether the taxpayer itemizes for federal income tax purposes.

Required Minimum Distributions (“RMDs”)

They’re back!!! RMDs are back for 2021. The deadline to withdraw a required minimum distribution for 2021 is December 31, 2021. Failure to do so can result in a 50 percent penalty.

Required minimum distributions apply to most retirement accounts (Roth IRAs are an exception). They apply once the taxpayer turns 72. Also, many inherited retirement accounts (including Roth IRAs) are subject to RMDs, regardless of the beneficiary’s age.

Planning for Traditional Retirement Accounts Inherited in 2020 and 2021

Those inheriting traditional retirement accounts in 2020 or later often need to do some tax planning. The end of the year is a good time to do that planning. Many traditional retirement account beneficiaries will need to empty the retirement account in 10 years (instead of being on an RMD schedule), and thus will need to plan out distributions over the 10 year time frame to manage taxes rate on the distributions.

2021 Federal Estimated Taxes

For those with small business income, side hustle income, significant investment income, and other income that is not subject to tax withholding, the deadline for 2021 4th quarter estimated tax payments to the IRS is January 18, 2022. Such individuals should also consider making timely estimated tax payments to cover any state income taxes.

Review & Update Beneficiary Designation Forms

Beneficiary designation forms control the disposition of financial assets (such as retirement accounts and brokerage accounts) upon death. Year-end is a great time to make sure the relevant institutions have up-to-date forms on file. While beneficiary designations should be updated anytime there is a significant life event (such as a marriage or a death of a loved one), year-end is a great time to ensure that has happened.

2022 and Beyond Tax Planning

The best tax planning is long term planning that considers the entire financial picture. There’s always the temptation to maximize deductions on the current year tax return. But the best planning considers your current financial situation and your future plans and strives to reduce total lifetime taxes. 2022 is as good a time as any to do long-term planning.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

Follow me on Twitter: @SeanMoneyandTax

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.