New Year’s Eve is an important day if you do a Backdoor Roth IRA. Read below to find out why.

The Backdoor Roth IRA

I’ve written before about the Backdoor Roth IRA. It is a two step process whereby those not qualifying for a regular Roth IRA contribution can qualify to get money into a Roth IRA. Done over several years, it can help taxpayers grow significant amounts of tax free wealth.

One of the best aspects of the Backdoor Roth IRA is that it does not forego a tax deduction. Most taxpayers ineligible to make a regular Roth IRA contribution are also ineligible to make a deductible traditional IRA contribution. In the vast majority of cases, the choice is between investing money in a taxable account versus investing in a Roth account. For most, a Roth is preferable, since Roths do not attract income taxes on the interest, dividends, and capital gains investments generate.

The Basic Backdoor Roth IRA and the Form 8606

Let’s start with a fairly basic example.

Example 1

Betsy, age 40, earns $300,000 from her W-2 job in 2021, is covered by a workplace 401(k) plan, and has some investment income. Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

At this level of income, Betsy does not qualify for a regular Roth IRA contribution, and she does not qualify to deduct a traditional IRA contribution.

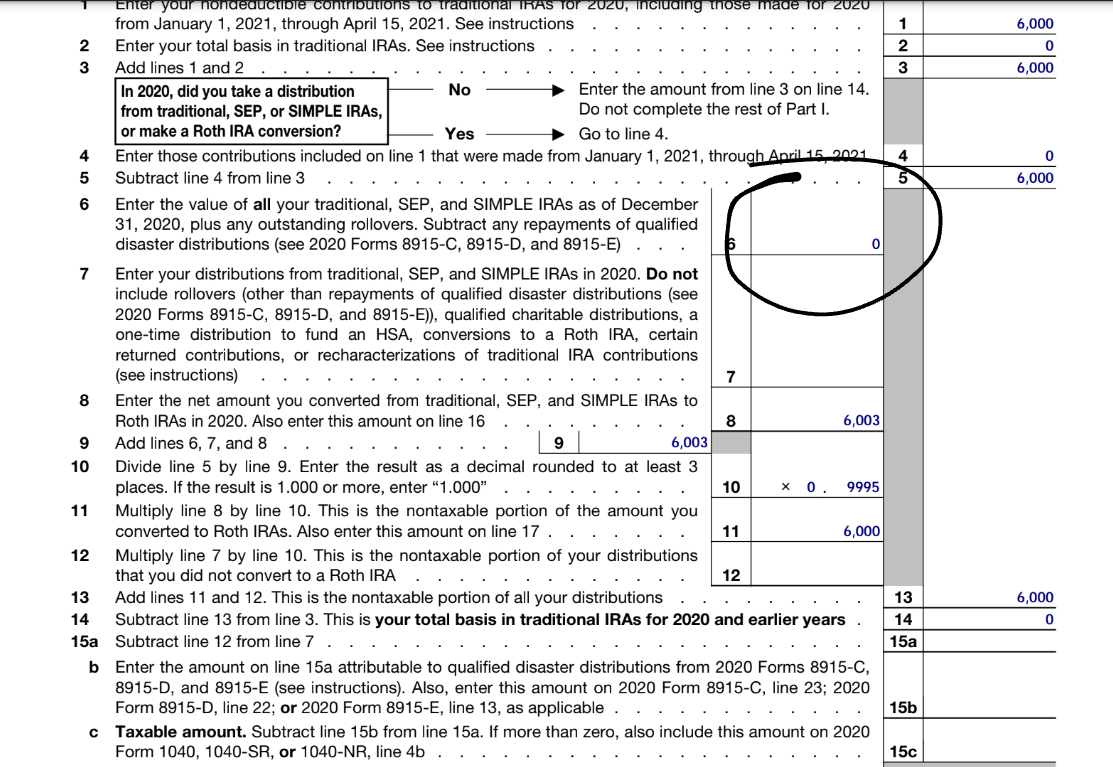

Betsy contributes $6,000 to a traditional IRA on May 20, 2021. The contribution is nondeductible. Because the contribution is nondeductible, Betsy gets a $6,000 basis in her traditional IRA. Betsy must file a Form 8606 with her 2021 tax return to report the nondeductible contribution.

On June 5, 2021, Betsy converts the entire balance in the traditional IRA, $6,003, to a Roth IRA. As of December 31, 2021, Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

Betsy has successfully executed a Backdoor Roth IRA. Here is what page 1 of the Form 8606 Betsy should file with her 2021 income tax return should look like.

Notice here that I am using the 2020 version of the Form 8606 for this and all examples. The 2021 Form 8606 is not yet available as of this writing.

The most important line of page 1 of the Form 8606 is line 6. Line 6 reports the fair market value of all traditional IRAs, SEP IRAs, and SIMPLE IRAs Betsy owns as of year-end. Because Betsy had no traditional IRAs, SEP IRAs, and SIMPLE IRAs as of December 31, 2021, her Backdoor Roth IRA works and is tax efficient. This important number ($0) on line 6 of the Form 8606 is what ensures Betsy’s Backdoor Roth IRA is tax efficient.

Note that Betsy’s Backdoor Roth IRA creates an innocuous $3 of taxable income, which is reported on the top of part 2 of the Form 8606.

The Pro-Rata Rule and December 31st

But what if Betsy did have a balance inside a traditional IRA, SEP IRA, or SIMPLE IRA on December 31, 2021? Would her Backdoor Roth IRA still be tax efficient? Probably not, due to the Pro-Rata Rule.

The Pro-Rata Rule tells us just how much of the basis in her traditional IRA Betsy can recover when she does the Roth conversion step of the Backdoor Roth IRA. Betsy’s $6,000 nondeductible traditional IRA creates $6,000 of basis. As we saw above, Betsy was able to recover 100 percent of her $6,000 of basis against her Roth conversion.

But the Pro-Rata Rule says “not so fast” if Betsy has another traditional IRA, SEP IRA, or SIMPLE IRA on December 31st of the year of any Roth conversion. The Pro-Rata Rule allocates IRA Basis between converted amounts (in Betsy’s case, $6,003) and amounts in traditional IRAs, SEP IRAs, and SIMPLE IRAs on December 31st. Here’s an example.

Example 2

Betsy, age 40, earns $300,000 from her W-2 job in 2021, is covered by a workplace 401(k) plan, and has some investment income. Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

Betsy contributes $6,000 to a traditional IRA on May 20, 2021. The contribution is nondeductible. Because the contribution is nondeductible, Betsy gets a $6,000 basis in her traditional IRA. Betsy must file a Form 8606 with her 2021 tax return to report the nondeductible contribution.

On June 5, 2021, Betsy converts the entire balance in the traditional IRA, $6,003, to a Roth IRA.

On September 1, 2021, Betsy transfers an old 401(k) from a previous employer 401(k) plan to a traditional IRA. On December 31st, that traditional IRA is worth $100,000. The old 401(k) had no after-tax contributions.

This one 401(k)-to-IRA rollover transaction dramatically changes both the taxation of Betsy’s Backdoor Roth IRA and her 2021 Form 8606. Here’s page 1 of the Form 8606.

Line 6 of the Form 8606 now has $100,000 on it instead of $0. That $100,000 causes Betsy to recover only 5.67 percent of the $6,000 of basis she created by making a nondeductible contribution to the traditional IRA. As a result, $5,663 of the $6,003 transferred to the Roth IRA in the Roth conversion step is taxable to Betsy as ordinary income. At a 35% tax rate, the 401(k) to IRA rollover (a nontaxable transaction) cost Betsy $1,982 in federal income tax on her Backdoor Roth IRA. Ouch!

Quick Lesson: The lesson here is that prior to rolling over a 401(k) or other workplace plan to an IRA, taxpayers should consider the impact on any Backdoor Roth IRA planning already done and/or planned for the future. One possible planning alternative is to transfer old employer 401(k) accounts to current employer 401(k) plans.

There is an antidote to the Pro-Rata Rule when one has amounts in traditional IRAs, SEP IRAs, and SIMPLE IRAs. It is transferring the traditional IRA, SEP IRA, or SIMPLE IRA to a qualified plan (such as a 401(k) plan) before December 31st. Here is what that might look like in Betsy’s example.

Example 3

Betsy, age 40, earns $300,000 from her W-2 job in 2021, is covered by a workplace 401(k) plan, and has some investment income. Betsy has no balance in a traditional IRA, SEP IRA, or SIMPLE IRA.

Betsy contributes $6,000 to a traditional IRA on May 20, 2021. The contribution is nondeductible. Because the contribution is nondeductible, Betsy gets a $6,000 basis in her traditional IRA. Betsy must file a Form 8606 with her 2021 tax return to report the nondeductible contribution.

On June 5, 2021, Betsy converts the entire balance in the traditional IRA, $6,003, to a Roth IRA.

On September 1, 2021, Betsy transfers an old 401(k) from a previous employer to a traditional IRA. The old 401(k) had no after-tax contributions.

On November 16, 2021, Betsy transfers the entire balance in this new traditional IRA to her current employer’s 401(k) plan in a direct trustee-to-trustee transfer.

Here is Betsy’s 2021 Form 8606 (page 1) after all of these events:

Betsy got clean by December 31st, so her Backdoor Roth IRA now reverts to the optimized result (just $3 of taxable income) she obtained in Example 1.

Pro-Rata Rule Clean Up

Implementation

From a planning perspective, it is best to clean up old traditional IRAs/SEP IRAs/SIMPLE IRAs prior to, not after, executing the Roth conversion step of a Backdoor Roth IRA. I say that because things happen in life. There is absolutely no guarantee that those intending to roll amounts from IRAs to workplace qualified plans will get that accomplished by December 31st.

Further, transfers from one retirement account to another are usually best done through a direct “trustee-to-trustee” transfer to minimize the risk that the money in the retirement account accidentally is distributed to the individual, causing potential tax and penalties.

Before cleaning up old traditional IRAs, SEP IRAs, and SIMPLE IRAs, one should consider the investment choices and fees inside their employer retirement plan (such as a 401(k)). If the investment options are not good, and/or the fees are high, perhaps cleaning up an IRA to move money into less desirable investments is not worth it. This is a subjective judgment that must weigh the potential tax and investment benefits and drawbacks.

Tax Issues

Amazingly enough, the Pro-Rata Rule is concerned with only one day: December 31st. A taxpayer can have a balance in a traditional IRA, SEP IRA, or SIMPLE IRA on any day other than December 31st, and it does not count for purposes of the Pro-Rata Rule. Perhaps December 31st should be called Pro-Rata Rule Day instead of New Year’s Eve. 😉

Betsy’s November 16th distribution from her traditional IRA to the 401(k) plan does not attract any of the basis created by the nondeductible traditional IRA contribution earlier in the year. This document provides a brief technical explanation of why rollovers to qualified plans do not reduce IRA basis.

Extra care should be taken when cleaning up (a) large amounts in any type of IRA and (b) any SIMPLE IRA. While it is fairly obvious that significant sums should be moved only after considering all the relevant investment, tax, and execution issues, the SIMPLE IRA provides its own nuances. Any SIMPLE IRA cannot be rolled to an account other than a SIMPLE IRA within the SIMPLE IRA’s first two years of existence. Thus, SIMPLE IRAs must be appropriately aged before doing any sort of Backdoor Roth IRA clean up planning.

Spouses are entirely separate for Pro-Rata Rule purposes, even in community property states. Cleaning up one spouse, or failing to clean up one spouse, has absolutely no impact on the taxation of the other spouse’s Backdoor Roth IRA.

Lastly, non spousal inherited IRAs do not factor into a taxpayer’s application of the Pro-Rata Rule. Each non spousal inherited IRA has its own separate, hermetically sealed Pro-Rata Rule calculation. The inheriting beneficiary does a Pro-Rata Rule calculation on all IRAs he/she owns as the original owner, separate from any inherited IRAs. In addition, non spousal inherited IRAs cannot be rolled into a 401(k).

Mega Backdoor Roth

Good news: the concerns addressed in this blog post generally do not apply with respect to the Mega Backdoor Roth (sometimes referred to as a Mega Backdoor Roth IRA, though a Roth IRA does not necessarily have to be involved). Qualified plans such as 401(k)s are not subject to the Pro-Rata Rule.

While 401(k)s are not subject to the Pro-Rata Rule, amounts within a particular 401(k) plan’s after-tax 401(k) are subject to the “cream-in-the-coffee” rule I previously wrote about here. Thus, if there is growth on Mega Backdoor Roth contributions before they are moved out of the after-tax 401(k), generally speaking either the taxpayer must pay income tax on the growth (if moved to a Roth account) or the taxpayer can separately roll the growth to a traditional IRA (which could then create a rather small Pro-Rata Rule issue with future Backdoor Roth IRAs). Fortunately, the cream-in-the-coffee rule has a much narrower reach than the Pro-Rata Rule.

Backdoor Roth IRA Tax Return Reporting

Conclusion

Get your IRAs in order so you can enjoy New Year’s Eve!

December 31st is an important date when it comes to Backdoor Roth IRA planning. It is important to plan to have no (or at a minimum, very small) balances in traditional IRAs, SEP IRAs, and SIMPLE IRAs on December 31st when planning Backdoor Roth IRAs.

None of what is discussed in this blog post is advice for any particular taxpayer. Those working through Backdoor Roth IRA planning issues are often well advised to reach out to professional advisors regarding their own tax situation.

Further Reading

I did a blog post about Backdoor Roth IRA tax return reporting here.

I did a deep dive on the taxation of Roth IRA withdrawals here.

I did a deep dive on the Pro-Rata Rule here.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

Follow me on Twitter: @SeanMoneyandTax

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.