Happy New Year! It’s Backdoor Roth IRA season, so let’s talk about the issue that refuses to go away . . . the timing of the two steps of the Backdoor Roth IRA.

Recall that the Backdoor Roth IRA is a two-step transaction. First, there is a nondeductible contribution to a traditional IRA. The second step is a relatively close-in-time conversion of the nondeductible traditional IRA contribution and any minor growth to a Roth IRA. Assuming the correct profile, this can move money into a Roth IRA for a year the person exceeds the Roth IRA contribution MAGI limits.

If there are two steps of the Backdoor Roth IRA, that begs a question: Just how long do I have to wait between the two steps, i.e., how long does the nondeductible traditional IRA contribution have to sit in the traditional IRA prior to the Roth conversion step? A minute? A day? A month? A year?

In some, but not all, cases there may have to be a few days or even a few weeks between the two steps of the Backdoor Roth IRA. Dr. Jim Dahle discussed this on a recent episode of The White Coat Investor podcast.

The Backdoor Roth IRA and the Step Transaction Doctrine

There has been a concern with the Backdoor Roth IRA: the step transaction doctrine, which can collapse steps into a single step. In theory, the two steps of the Backdoor Roth IRA can be viewed as a single step (a direct contribution to a Roth IRA), which creates an excess contribution (subject to a potential 6 percent penalty). Michael Kitces has written that he is concerned that, because the Roth conversion step might occur so soon after the nondeductible traditional IRA contribution, the step transaction doctrine can apply to the Backdoor Roth IRA. Kitces generally advocates waiting a year between the steps based on his step transaction doctrine concern. To my knowledge he has never changed his view on the issue.

I believe Mr. Kitces is a bit of a lone voice on the issue these days. In fact, Kitces’ own colleague Jeffrey Levine disagrees with him on the issue.

Two late 2010’s developments moved the needle in the practitioner community towards Mr. Levine’s view. First, the IRS, in informal comments, indicated they were not too concerned with the Backdoor Roth IRA. Second, the legislative history to 2017’s Tax Cuts and Jobs Act indicated that Congressional staffers believed the Backdoor Roth IRA was valid. I believe this second development was overblown, as legislative history, to the extent relevant, is relevant to the legislation then being passed. It is not relevant, to my mind, to prior legislation (the Backdoor Roth IRA enabling legislation passed in 2006 – see Section 512). That said, both developments were informative, though certainly not binding.

Sean’s Take

I have never been too concerned with the Step Transaction Doctrine and the Backdoor Roth IRA. In 2019, I co-wrote a Tax Notes article (available behind a paywall) about the issue with Ben Willis, my former PwC colleague. We concluded that it is not appropriate to apply the step transaction doctrine to a taxpayer’s use of the explicit, taxpayer favorable IRA rules. I believe we made a good case that the step transaction should not apply to the Backdoor Roth IRA based on the contours of the doctrine.

The Backdoor Roth IRA and Section 408(d)(2)(B)

Since 2019, I have further developed my thinking. I now believe a little commented-on rule in the IRA statute is very instructive: Section 408(d)(2)(B).

Section 408(d)(2)(B) provides that all IRA distributions during the year are treated as a single distribution. As a result, the timing of IRA distributions is irrelevant. A January 1st distribution is treated the same as a March 29th distribution, which is treated the same as a December 31st distribution. Roth conversions are distributions from an IRA.

By grouping all IRA distributions into a single distribution, the Internal Revenue Code tells us the timing of IRA distributions, including Roth conversions, during the year is irrelevant.

It would be exceedingly odd to apply a judicial doctrine (the step transaction doctrine) to give that timing relevance when the Code strips away that relevance. Anyone arguing the step transaction doctrine applies to a Backdoor Roth IRA is saying that the step transaction doctrine should override the specific rule of Section 408(d)(2)(B) in determining the degree of relevance afforded to the timing of the Roth conversion step.

I strongly believe it is not appropriate to apply the step transaction doctrine when the Internal Revenue Code itself gives us a rule telling us the timing of the Roth conversion is irrelevant.

Backdoor Roth IRA Favored Timing

I have two beliefs. First, timing is irrelevant when doing the Backdoor Roth IRA. Second, my views are not guaranteed to yield a 9-0 Supreme Court decision 😉

Based on those two beliefs, I have a third. The most desirable Backdoor Roth IRA path is to wait until the end of a month passes and then do the Roth conversion step of the Backdoor Roth IRA. This is the old Ed Slott tactic and locks in an end-of-month statement showing some interest or dividends in the traditional IRA.

It could look something like this:

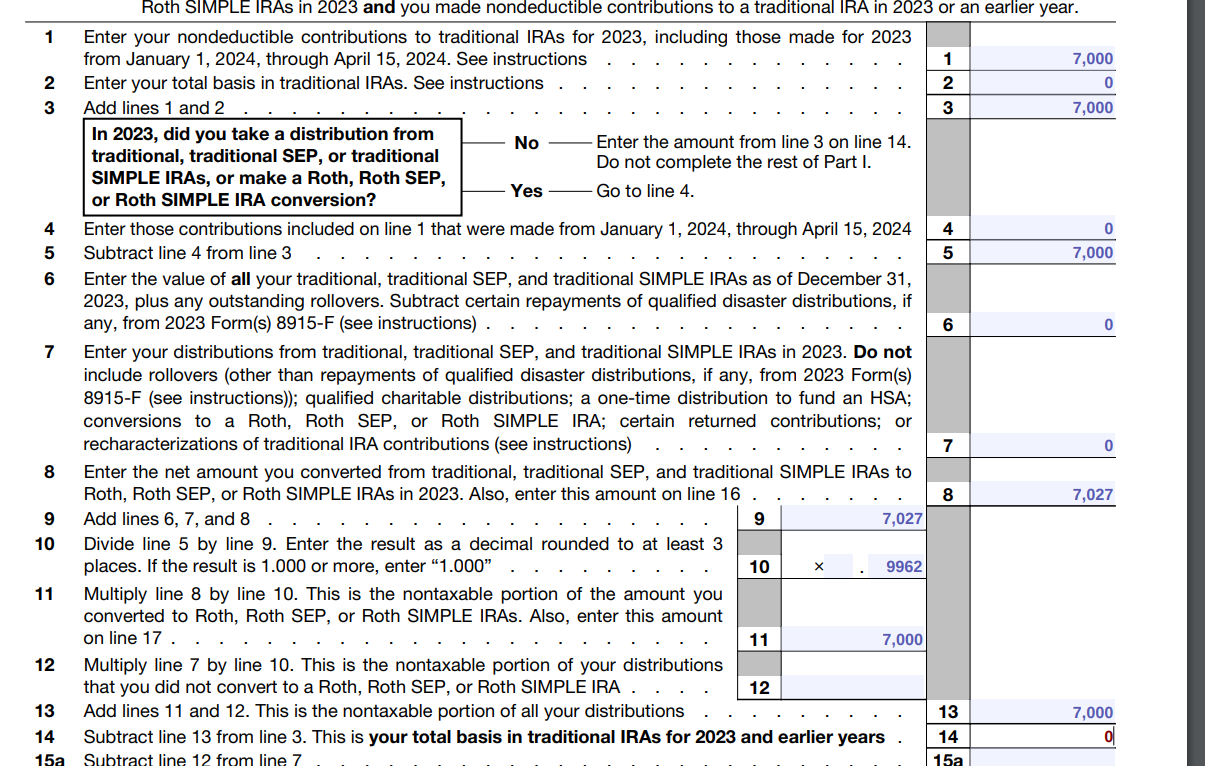

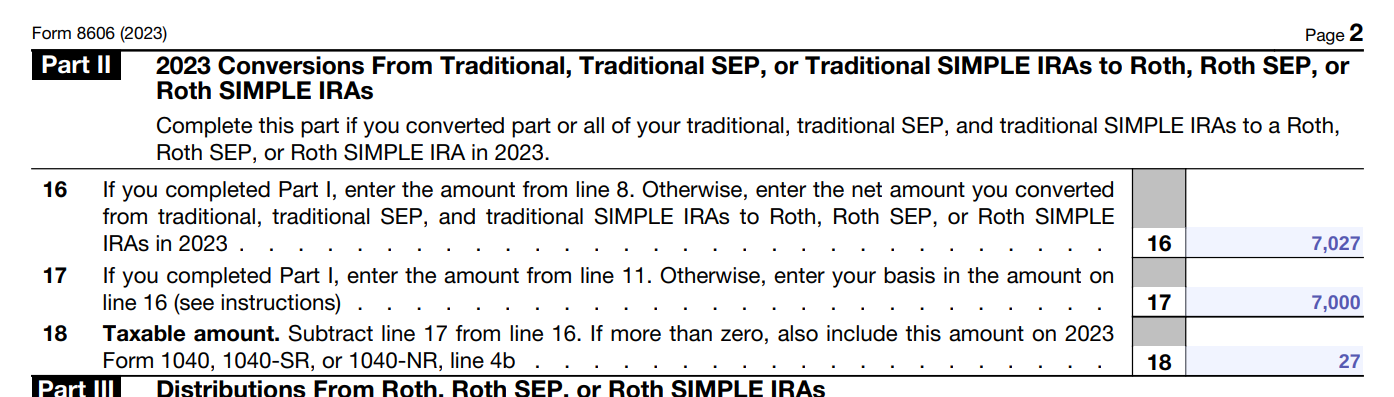

Roger contributes $7,000 to his traditional nondeductible IRA on January 2, 2025 for 2025 and invests it in a money market fund. On February 1, 2025, he converts the entire amount, now $7,027, to a Roth IRA. He has no other IRA transactions during the year and on December 31, 2025 he has $0 balances in any and all traditional IRAs, SEP IRAs, and SIMPLE IRAs.

Oh no, Roger created $27 of taxable income on his Backdoor Roth IRA. We’ve finally found something worse than IRMAA!

All kidding aside, here’s what Roger’s 2025 Form 8606 could look like (pardon the use of the 2023 form, the latest version available as of this writing): 8606 Page 1 8606 Page 2 And, yes, Roger should convert the entire traditional IRA balance, not just the $7,000 originally contributed to the traditional IRA.

{kind=link}

{kind=link}

To my mind, this works as a good Backdoor Roth IRA. So now you say, But Sean, what about your first belief? I thought timing was irrelevant!

I respond, (A) see my second belief and (B) what’s the downside of my desired approach?

$27 of taxable income creates $10 of federal income tax if Roger is in the highest federal tax bracket, and Roger will have $27 more protected from future tax by the Roth IRA.

The Backdoor Roth IRA Should Not Exist

That the Backdoor Roth IRA exists is ridiculous. It is obnoxious that our tax laws are so complicated that one of the most prominent financial planners, Michael Kitces, could plausibly claim the step transaction doctrine adversely impacts the Backdoor Roth IRA.

Let’s end all of this and adopt a rule that notorious tax haven, Canada, has adopted: Eliminate the income limit on the ability to make an annual Roth IRA contribution! Canada’s Tax-Free Savings Account (their version of a Roth IRA) has absolutely no income limit on the ability to make a contribution. America should adopt that rule as a small part of what hopefully will be a dramatic simplification of American income tax laws in 2025.

Conclusion

I do not believe that the step transaction doctrine should apply to the Backdoor Roth IRA. I do not believe that the timing of the two steps is relevant for determining their ultimate federal income taxation. That said, I like waiting until the following month to do the Roth conversion step.

Of course, the entirety of this article is simply academic commentary. It is not tax, legal, or investment advice for you or anyone else.

FI Tax Guy can be your financial planner! Find out more by visiting mullaneyfinancial.com

Follow me on X: @SeanMoneyandTax

This post is for entertainment and educational purposes only. It does not constitute accounting, financial, investment, legal, or tax advice. Please consult with your advisor(s) regarding your personal accounting, financial, investment, legal, and tax matters. Please also refer to the Disclaimer & Warning section found here.

Thanks for the post, Sean.

I just did my contribution on the first and then the conversion on the third.

I guess we’ll see. . .😬

At this point millions (tens of millions perhaps?) of backdoor Roth conversions have been done the same week of the contribution, and I’ve yet to hear of a single case of an invalidated backdoor based on timing.

100% this. I do my conversions the day the money to the traditional IRA is settled. Have never had a problem.

I have a somewhat related question: Can one isolate past deductible contributions and growth from bases (for a subsequent Roth conversion) by transferring that part of a Traditional IRA to a solo 401k OR 403(b) and is one ‘allowed’ to have BOTH continue to exist?

Meaning: I have all of a Roth IRA, Traditional IRA, Solo 401k (as well as Solor Roth 401(k) and a 403(b) (and Roth 403(b)) Plan. Can I eliminate the Traditional IRA by moving the basis to the Roth IRA and the tax deferred contribution+growth from the TIRA to EITHER the Solo 401k OR 403(b) but keep both those plans.

I want to isolate the basis and tax deferred funds, so I can actually start doing ‘clean’ Backdoor Roth Conversions as described above in your article the calendar year after I have done the above isolation of investments.

Unfortunately I can’t address any particular individual situation in the blog comments. I wrote an article on what I refer to as the Basis Isolation Backdoor Roth IRA on the blog you may find interesting from an academic perspective. But I can’t comment on whether and/how it applies to the particulars of your situation.

Love hearing you on podcasts. The newsletter subscribe function doesn’t work. Keeps giving an error.